End-of-quarter synthesis. Q1 2026.

On February 19, Guillaume Faury called 2025 “a landmark year.” Revenue hit €73.4 billion. EBIT Adjusted rose 33% to €7,128 million. The backlog grew to 8,754 aircraft. The stock fell 8%.

Thirty-seven days later, Iranian drones struck four Gulf airports. Three maritime chokepoints closed simultaneously. The aluminium smelter that feeds Airbus’s fuselage supply entered shutdown. Oil hit $119. Jet fuel crack spreads exceeded the levels that preceded the 2005 airline bankruptcies. The 2026 guidance, published nine days before the strikes, assumed “no additional disruptions to global trade or the world economy, air traffic, the supply chain.”

Between the earnings release and the first drone impact, a structure became visible. This is what the quarter revealed.

I. The headline and what it contains

The +33% in EBIT came from one place. Defence & Space swung from a €566 million loss to €798 million in profit, a €1,364 million improvement accounting for 77% of the group’s gains. The swing was a base effect: €1.3 billion in space-systems charges in 2024 had turned a normally profitable division into a loss-maker. Remove D&S, and group EBIT grew 7%.

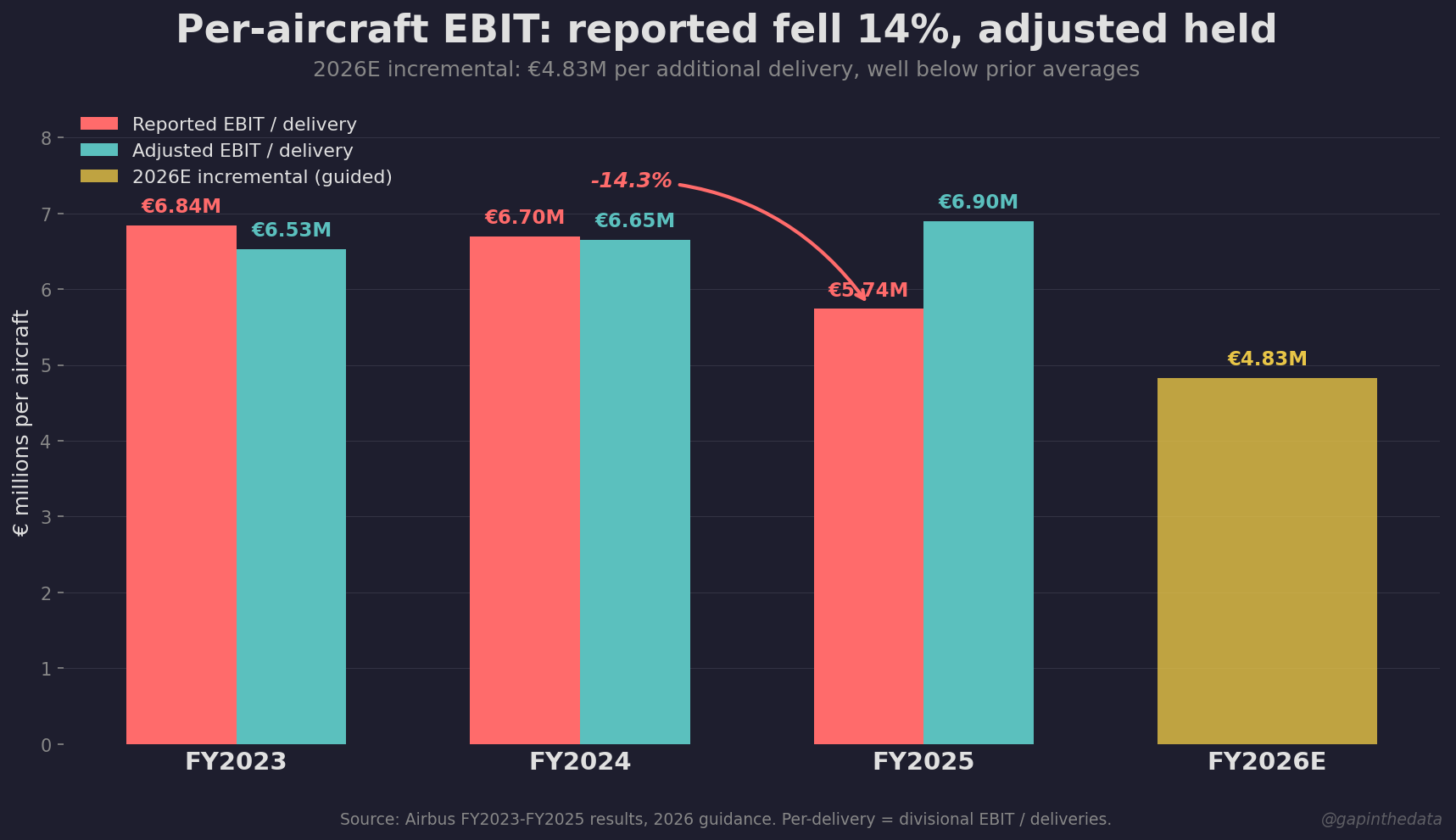

The commercial aircraft business that generates 72% of revenue earned less than it did a year ago on a reported basis. EBIT Reported fell 11.3%, from €5,133 million to €4,555 million, despite 27 more deliveries. Per-aircraft reported earnings dropped 14%, from €6.70 million to €5.74 million. The adjusted number held. The reported number did not. Both are in the same filing.

At €7.5 billion in guided EBIT on 870 deliveries for 2026, each incremental aircraft contributes €4.83 million, well below the prior year’s average. On a commercial-aircraft basis, EBIT declines €219 million despite 77 more deliveries, as headwinds compound: FX drag of €300 million, rising R&D, Spirit integration costs, tariffs, and an engine constraint limiting the one segment at mature margins.

Free cash flow before customer financing has been essentially flat at €4.4 to €4.6 billion for four consecutive years on 12% revenue growth. The 2026 guide of approximately €4.5 billion would make a fifth. Revenue climbs. Cash flow does not.

II. Three ramps, one paradox

Airbus is ramping three loss-making programmes simultaneously, and the paradox is that success makes the problem worse. Every additional delivery of an A220, A350, or A321XLR dilutes the average margin because none has reached the production rate at which it becomes accretive.

The A350 delivered 57 aircraft in FY2025, an average of 4.75 per month against a target of 8 and a long-term goal of 12. Forecast International described the performance as showing “no signs of stabilizing, even at the six-per-month rate.” Spirit AeroSystems, whose A350 fuselage operations Airbus absorbed at a nine-figure annual loss, constrains the primary bottleneck. United Airlines removed 45 A350-900s from its fleet plans over a Rolls-Royce dispute, and five airworthiness directives in eight months compound the ramp challenge. The programme that needs every delivery slot to amortise costs has fewer buyers at exactly the wrong moment.

The A220 has been under Airbus ownership for seven years and still loses money on every airframe. Faury declined to say when that changes. The programme took a €500 million impairment in FY2025; Quebec wrote off C$400 million of its own. The breakeven target has slipped from rate 14 to rate 12 for 2026, with a partial recovery to 13 by 2028. The A220 had zero new orders in all of 2025, the worst year in the programme’s history, while Embraer took 154 E-Jet E2 orders and built its backlog to a record $31 billion. Nordic carriers needed narrowbodies before 2032; Airbus had no slots; Finnair bought Embraers.

The A321XLR has no competition and a delivery problem that zero competition cannot solve. Frontier cancelled all 18 orders. Wizz Air slashed from 47 to 11. JetBlue deferred all 13. Aegean bought two ex-JetBlue aircraft, then cancelled both over seat certification delays that pushed delivery past the summer revenue window. Replacement buyers, airlines retiring 757s and downgauging widebody routes, will wait because they must. Expansion buyers, airlines opening routes that have never existed, walk away because the route simply does not happen.

The A350 and A220 share a root cause: Spirit constrains the A350 rate, Spirit’s integration delays the A220 breakeven, and both programmes dilute the delivery mix that determines group margins. The XLR’s problems are different in kind, demand-side and regulatory rather than production-driven, but identical in effect: fewer deliveries of higher-margin aircraft at the moment the mix needs them most.

III. The constraint stack

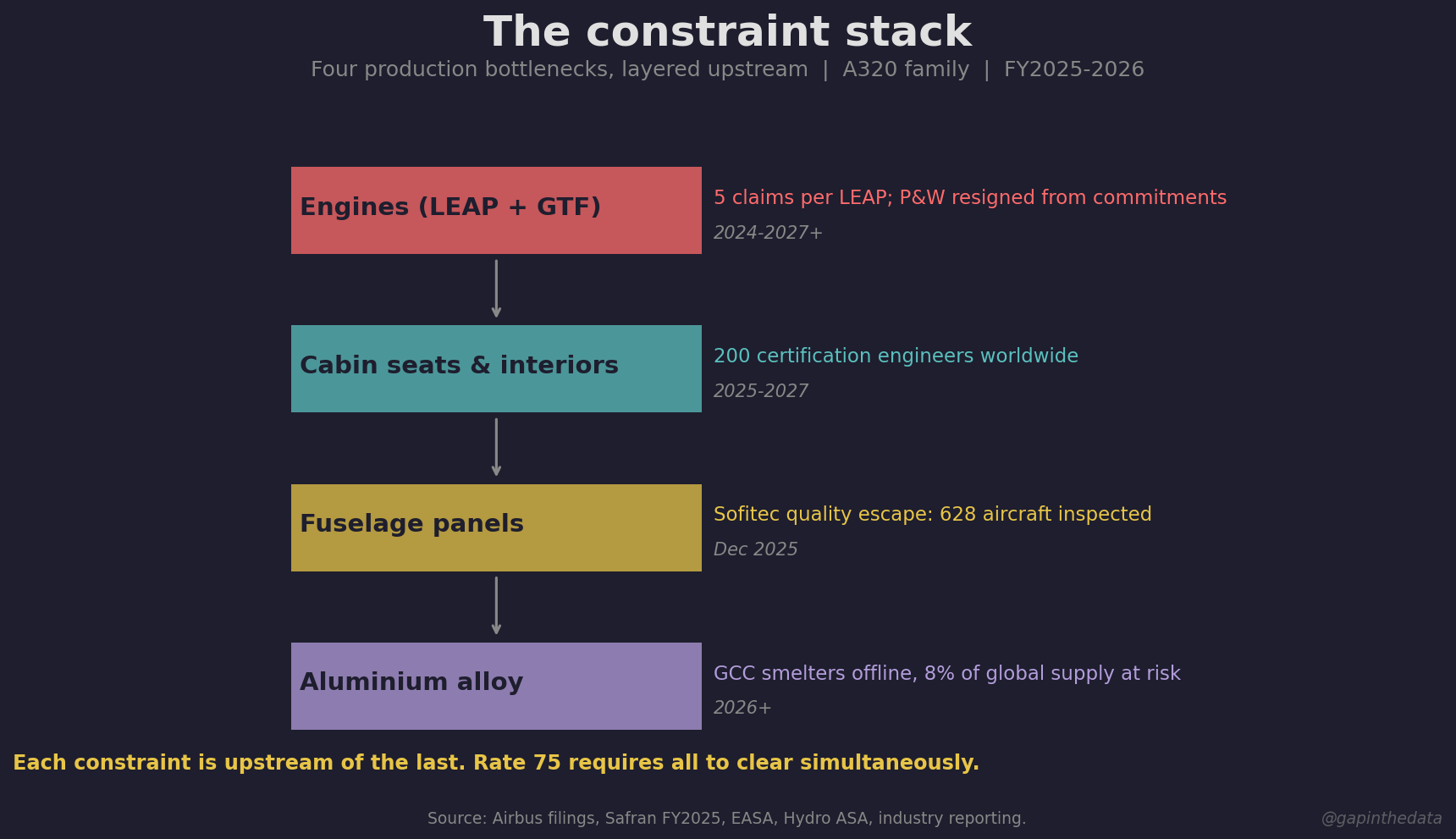

The A320 family, the one programme at mature margins, is itself constrained at every major stage of production.

Five competing claims fight over every LEAP engine Safran builds: Boeing’s 737 MAX programme (roughly 890 engines in 2025), COMAC’s C919 (30), spare engine pools, a tripling aftermarket, and what remains for Airbus. Safran’s 1,802 engines cannot simultaneously justify Safran’s aftermarket growth and Airbus’s delivery acceleration. One of those stories is wrong.

Pratt & Whitney, which supplies engines for approximately 40% of A320neo production, has not finalised volumes for 2026 or 2027. Faury’s language at the annual press conference was unusually direct: “Pratt & Whitney has resigned from the orders we had placed and they had accepted.” “They are not respecting their contractual obligations.” “Indeed we have initiated a process according to contractual requirements of disputes.” Rate 75, the production target that underpins the delivery guidance, has slipped from 2025 to 2026 to “70 to 75 by the end of 2027.”

But engines are only the first constraint in a stack that runs deeper. They bound production for ten months of 2025. Then, in December, a supplier quality issue on fuselage panels from Sofitec in Seville required inspection of 628 aircraft and cut guidance by 30 deliveries. Solving one surfaced the next. Below the panels sit premium cabin seats, with only 200 certification engineers worldwide and bespoke designs requiring 3,000 parts from 50 suppliers. Below the seats sits aluminium, the raw material making up 75 to 80% of every A320 airframe, now itself at risk. Each layer is upstream of the last. Rate 75 requires all of them to clear simultaneously.

Even the delivery figures that do emerge carry an asterisk. Airbus delivered 136 aircraft on December 31, 17.2% of the annual total, then 19 in January, the lowest since COVID. The pattern has held for three years, with December’s share climbing from 15.2% to 16.1% to 17.2%, each time followed by a January collapse. Aircraft contractually delivered on the final day of the year were physically ferried to operators throughout the following month. The 136 and the 19 are one event split across a calendar boundary.

IV. The dependency Airbus built

Twenty percent of Airbus’s single-aisle production physically depends on infrastructure in China, co-owned with AVIC, a state enterprise whose subsidiaries build the C919, whose subsidiary sells aircraft to the IRGC, and which the Trump administration designated as a PLA-linked entity. AVIC is simultaneously Airbus’s largest non-engine supplier globally, COMAC’s founding shareholder, and the supermajority owner of the Harbin facility that is the sole worldwide source for four critical A350 composite structures.

The technology transfer is structural rather than incidental. Engineers working on Airbus programmes at AVIC subsidiaries accumulate composite manufacturing expertise directly applicable to COMAC programmes. The same workforce, facilities, and institutional knowledge serve both customers. In July 2025, while the analysis community debated whether COMAC posed a long-term threat, Airbus expanded the AVIC partnership to A321 fuselage equipping.

COMAC delivered 15 C919s in 2025 against a target that shifted from 30 to 75 to 25. The programme runs behind schedule. It is on strategy. Beijing’s response, published in the 15th Five-Year Plan, was to accelerate the CJ-1000A, the domestic engine that eliminates the C919’s dependence on Western suppliers. Near-term, every CJ-1000A that replaces a LEAP-1C frees an engine for CFM’s other customers. Long-term, a COMAC that no longer needs US export licences is a COMAC whose production ceiling is set by Chinese industrial capacity, not American trade policy. The engine pool loosens. The competitor unshackles.

COMAC has built a three-variant narrowbody family in two years, covering 138 to 240 seats. IBA forecasts 90 C919 deliveries per year by 2030. The domestic market alone, 9,500 new aircraft over twenty years by Faury’s own estimate, sustains the programme without a single export. Airbus does not disclose China-specific revenue. At roughly 20% of deliveries, the exposure is an estimated €10 to €14 billion annually.

When China built its high-speed rail network, it invited Kawasaki, Siemens, Alstom, and Bombardier to compete for contracts, conditioned every one on technology transfer, and within fifteen years CRRC held 56% of the global HSR market. Airbus opened its first Tianjin assembly line in 2008. Every decision was rational in isolation. The pattern they form is not.

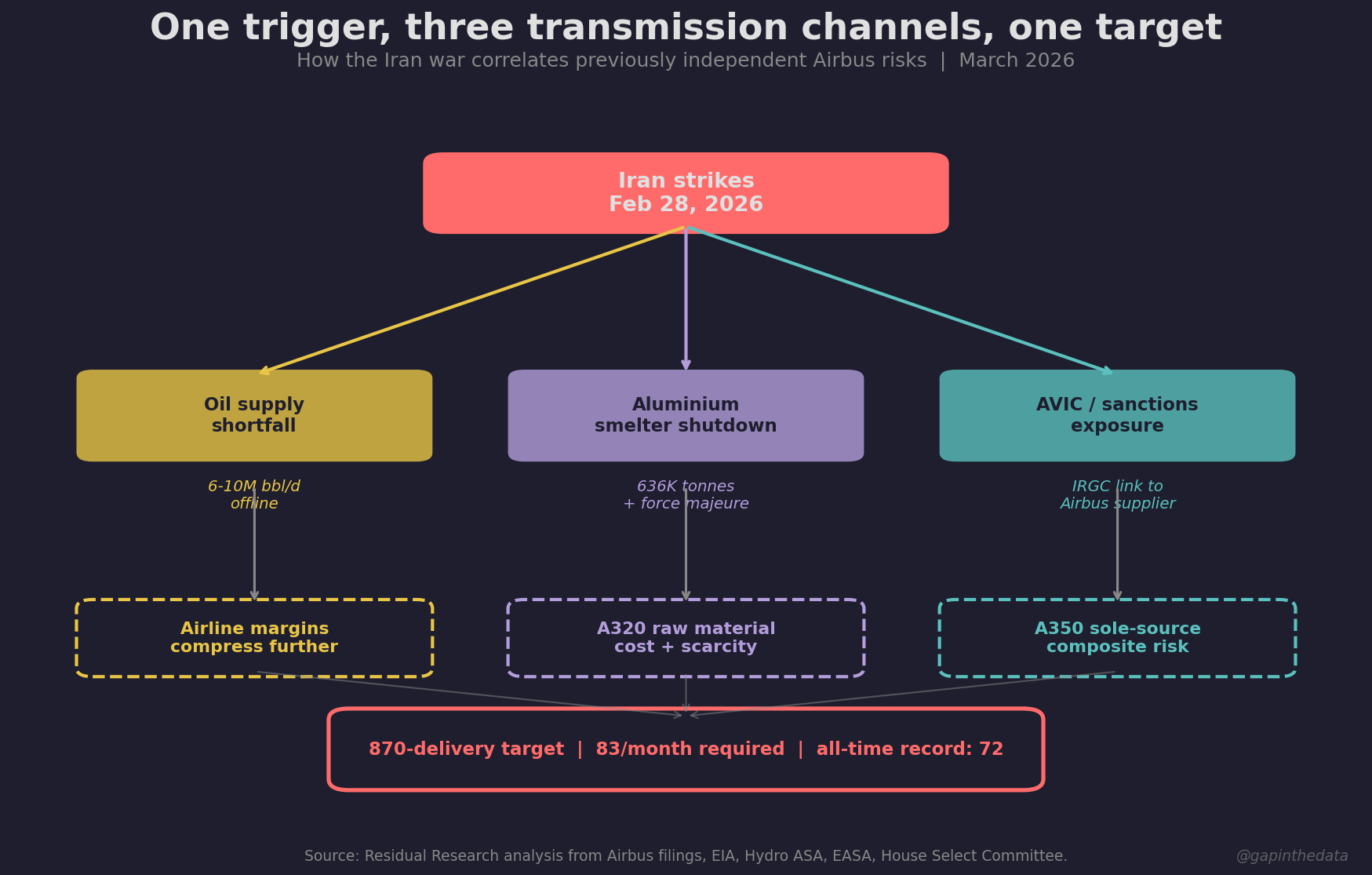

V. The correlation event

Before February 28, each of the risks documented in Sections I through IV was independent. The engine constraint had nothing to do with Gulf carrier financial health. The AVIC supply chain was unrelated to oil prices. The three loss-making ramps were unrelated to the Strait of Hormuz. Each was priced independently.

The transmission runs through three channels simultaneously. The first is airline economics. Margins were already compressing before the first drone launched: SWISS from 13.5% to 9.1% in two years, Ryanair from 15.3% to 11.2%, American from 4.8% to 2.7%, every carrier in the sample now operating below its 2019 level even as passenger volumes grew. The cost ratchet, post-pandemic labour contracts adding 35 to 54% at US carriers, infrastructure fees, engine maintenance mandates, was already tightening the range between revenue and expense. An oil shock lands on airlines that have no margin left to absorb it. They defer deliveries, negotiate harder on pricing, and conserve cash. The backlog number stays constant; the cash conversion timeline extends. The weakest tail, roughly 1,000 to 1,100 European LCC aircraft at 12% of the total, concentrates carriers with junk credit, grounded fleets, and ancillary revenue ratios above 40% now threatened by regulation.

Three maritime chokepoints closed simultaneously. The Strait of Hormuz handles 20% of global oil consumption. The Red Sea rerouting adds 10 to 14 days and $1 million per voyage. The Bosphorus was already constrained. The net oil shortfall runs conservatively 6 to 10 million barrels per day. The G7 declined to release strategic reserves; combined maximum release capacity covers 15 to 33% of the shortfall, and the buffer has not been deployed.

Qatalum’s 636,000-tonne aluminium smelter entered controlled shutdown after the strikes destroyed its gas supply infrastructure. Alba declared force majeure. The global aluminium market entered the crisis with 13 days of inventory, zero in US warehouses, and a structural deficit of 400,000 to 600,000 tonnes before the first smelter shut down. An A320 requires 31 tonnes of aluminium. The ramp from rate 50 to rate 75 requires 50% more metal each month, from a market that just lost 8% of supply.

Jet fuel crack spreads blew out to $85 to $95 per barrel, wider than the levels that preceded the 2005 airline bankruptcies. US Gulf Coast jet fuel hit $4.30 per gallon against a $4.36 peak in 2008 that triggered 25 US carrier bankruptcies. Deutsche Bank called it an “existential threat.” Four of the eight major carriers entered the crisis unhedged. Emirates, the A350’s largest single customer, does not hedge fuel and never has.

Airbus needs roughly 83 deliveries per month for the rest of 2026 to reach 870. The all-time monthly average is 72. The customers who are supposed to accept those aircraft are the airlines whose fuel bills rose by billions, whose airports were struck, whose margins were already falling. In 2008, comparable conditions reduced Airbus new orders by 79%.

VI. The competitor recovers

For four years, Airbus’s constraints were offset by the absence of a functioning competitor. That offset is ending.

Boeing outdelivered Airbus nearly two to one through the first two months of 2026: an estimated 98 to 52. Boeing led net orders in January for the first time since at least 2019. The financial press framed this as a competition story. The structure says something different.

The two companies share a supply chain, and Boeing’s acceleration tightens the constraints already binding on Airbus. Boeing exited 2025 at rate 42 and targets rate 47 by mid-2026. Every additional 737 MAX absorbs two LEAP-1Bs from the same upstream supply base that feeds the LEAP-1A. When Boeing was grounded, CFM’s upstream allocation was effectively Airbus-first by default. The FAA lifted the production cap in September 2025.

The 737 MAX 10 has more than 1,400 firm orders and zero deliveries. The FAA cleared Boeing for Phase 2 flight testing in December 2025, with a nacelle redesign and congressionally mandated safety enhancements remaining, the latter a direct consequence of the MCAS concealment that killed 346 people. If certified in late 2026 or early 2027, Airbus’s uncontested pricing power in the 200-plus seat segment faces competitive pressure for the first time since 2022.

Boeing’s balance sheet qualifies every comparison: $54 billion in total debt against Airbus’s €12.2 billion in net cash. But the trajectory is the shift. Boeing’s free cash flow moved from negative $14.3 billion to negative $1.9 billion to a positive guide, while Airbus’s has been flat for four years. The $10 billion FCF target Ortberg has stated is years away, but the direction of travel changes supplier leverage at the margin, and that margin is where the engine allocation is decided.

VII. What the backlog contains

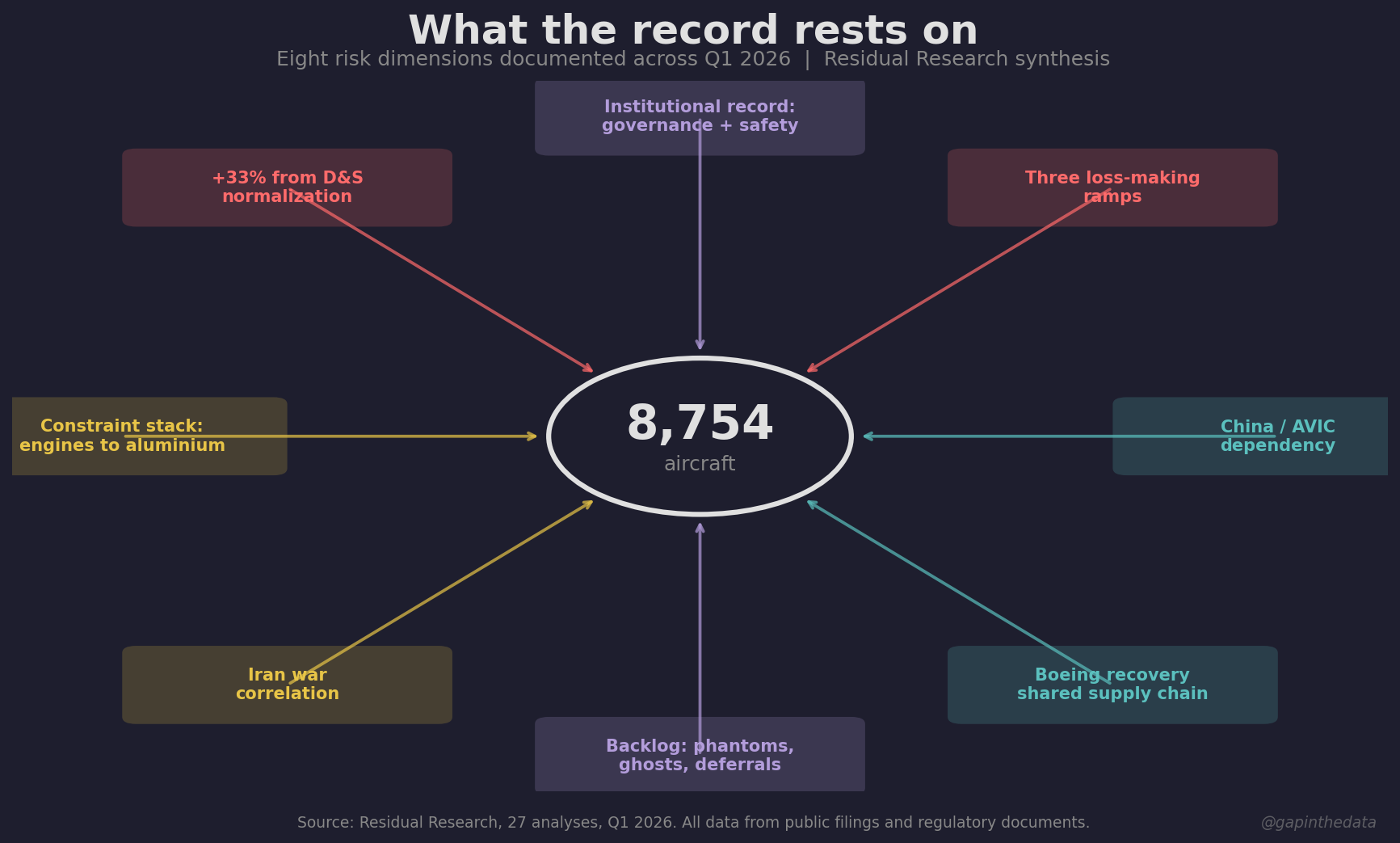

The number 8,754 has never been audited against the orders that compose it.

Documented cancellations and conversions include 66 A321XLRs cancelled or converted, 108 A350/A350F aircraft cancelled or removed from delivery plans, 89 A330neos cancelled with 15 more pending, and 31 A220s removed. Deferrals push another 283 or more aircraft into 2029 through 2033 by airlines in bankruptcy, exiting types, or cutting capacity. Iran Air’s 97 orders sat at zero delivery probability for five years before removal in 2023. United’s 45 A350-900s have occupied the backlog for seventeen years with zero deliveries and no date.

Airbus reports under IFRS 15, which imposes no requirement to estimate probable cancellations. Boeing, under ASC 606, removed approximately 550 orders through adjustments in 2020 alone. Same pandemic, same demand shock. Airbus removed 66. The gap between the analysts’ number and the company’s number is the gap between two accounting standards, one of which requires disclosure and one of which does not.

The headline serves the diplomatic moment. In January 2018, President Macron announced 184 aircraft from China; the order was never fulfilled as announced. In September 2023, Macron announced 10 A350s for Biman Bangladesh; Biman chose Boeing. In February 2026, Chancellor Merz stood in Beijing and announced “up to 120 additional aircraft.” Three weeks later, Airbus has not confirmed the order.

VIII. The institutional record

Bribery was endemic within Airbus in core business areas. That phrase is a British judge’s, used in approving the €3.6 billion settlement in 2020. French prosecutors estimated the corruption increased Airbus’s profits by €1 billion, channelled through a 150-person strategy unit with a $300 million annual budget whose internal sub-unit was described by a former executive as “like our secret service.”

The consequences distributed asymmetrically. In Indonesia, Emirsyah Satar received 8 years, then 5 more; Hadinoto Soedigno received 12 and died in custody. In Sri Lanka, Kapila Chandrasena was arrested on March 12, 2026. In Nepal, 32 charged, 11 convicted.

At Airbus, over 100 employees were terminated. Zero were criminally prosecuted. The CEO of Airbus signed commission declarations stating “none” on a €1 billion Kuwait helicopter contract where an ICC tribunal later awarded the intermediary €12 million. The Kuwaiti parliament found Airbus had engaged in “fraud and deception.” The Emir dissolved parliament. The investigation is frozen.

On March 23, four days after the UK High Court heard a whistleblower case about subsidiary bribery on MOD contracts, Airbus acquired the sovereign encryption hardware for the UK’s SKYNET military satellite network. In March 2025, Ethisphere named Airbus one of the “World’s Most Ethical Companies.”

The safety record follows the same institutional pattern. The A320 family is one-fifth of the American narrowbody fleet and generates four-fifths of reported cabin fume events, at seven to 36 times the 737’s rate depending on methodology. Airbus’s own Project Fresh programme traced 88% of APU fume events to external contaminants ingested through a belly-mounted inlet, identified a fix projected to reduce events by 85%, and applied it only to aircraft not yet built. The approximately 10,000 aircraft currently in service will fly unchanged until retirement. A Swiss A340 landed flapless twice in four days after maintenance failed to resolve the failure, a pattern that had appeared across six operators and three EASA airworthiness directives. The A350 accumulated five regulatory actions in eight months, including a factory-origin defect that the FAA said could lead to “loss of control of the airplane.” In each case, the manufacturer identified the problem, and the fleet that carries passengers today continues to fly with it.

IX. What the record rests on

Find the structure underneath the surface. Ignore the presentation. Check whether the structure supports what is built on top of it.

The presentation is record revenue, record EBIT, record backlog. The structure is a commercial aircraft business whose reported earnings declined on more deliveries, three loss-making ramps that dilute margins as they accelerate, an engine duopoly where one supplier has resigned from its commitments and the other’s output is claimed five times over, a 20% production dependency on a state enterprise simultaneously building the competitor, a demand base of airlines whose margins have compressed below pre-pandemic levels, a geopolitical event that correlates every previously independent risk through a single transmission mechanism, a competitor recovering from crisis and pulling harder on the shared supply chain, a backlog whose composition has never been reconciled against the orders inside it, and an institutional record that the filings contain and the presentations do not mention.

The record also rests on €12.2 billion in net cash against a competitor carrying $54 billion in debt, an A321neo with no certified rival in the 200-plus seat segment and no prospect of one until Boeing resolves a certification process redesigned in response to 346 deaths, airline switching costs measured in billions that lock the narrowbody backlog in place regardless of delivery timing, an A320 family that generates the majority of commercial aircraft profit at mature margins, a Defence & Space division that posted record order intake of €17.7 billion in a Europe accelerating military spending, and a production constraint that functions as a moat: every aircraft Airbus delivers sells into a market where demand exceeds supply by a decade.

Both are in the record.

The 2026 guidance was published nine days before Iranian drones struck four airports. It assumes no disruptions. The disruptions are here.

Eight thousand seven hundred and fifty-four aircraft. What it rests on is what this quarter was about.

Disclosure

This article is a synthesis of analytical commentary previously published on this site, based on publicly available sources cited in the individual analyses linked above. It does not constitute a personal recommendation, investment advice, or an inducement to buy or sell any financial instrument. Forward-looking assessments, including delivery projections, margin estimates, and conditional scenarios, represent the author’s arithmetic from disclosed data and third-party estimates and should not be construed as forecasts or price targets. Key assumptions are stated in the individual analyses.

Residual Research and its contributors hold no positions in the securities, commodities, or derivatives discussed in this article at the time of publication. No compensation has been received from any entity discussed. No article has been reviewed or approved by any issuer prior to publication.

Produced in compliance with Regulation (EU) No 596/2014 (Market Abuse Regulation) and Commission Delegated Regulation (EU) 2016/958. See the full Disclaimer for further regulatory information.