The war doesn’t create new risks. It correlates existing ones.

Airbus set its 2026 guidance on February 19: roughly 870 deliveries, €7.5 billion in EBIT Adjusted, €4.5 billion in free cash flow.1 The guidance assumed “no additional disruptions to global trade or the world economy, air traffic, the supply chain."2

Nine days later, Iranian drones struck Dubai International Airport, Abu Dhabi’s Zayed International, Kuwait International, and Bahrain International.3 Emirates grounded all 260 aircraft,4 eight countries closed their airspace, and 868 flights were cancelled on the first day.5 Supreme Leader Khamenei was confirmed killed on March 1.68

I. What the war changed

Before February 28, each of the risks in this series was independent.

The engine duopoly constraint had nothing to do with Gulf carrier financial health. The AVIC supply chain dependency was unrelated to oil prices. The three loss-making ramps were unrelated to the Strait of Hormuz. Each was priced independently.

The war is the transmission mechanism.

An oil shock hits airline economics, airlines under financial pressure defer deliveries, and deferred deliveries reduce Airbus’s output against a target already constrained by engines and diluted by loss-making ramps.

The diplomatic fallout touches the supply chain directly. AVIC, Airbus’s largest non-engine supplier, has a subsidiary that sells aircraft to the IRGC Aerospace Force, the same organisation that declared the Strait of Hormuz closed.49

Defence & Space, at 6% margins and 11% of group EBIT, cannot compensate for a division that generates 72% of revenue.6

The risks did not change in kind. They changed in correlation. Independent risks sum. Correlated risks compound.

II. The delivery arithmetic

Airbus delivered 43 aircraft to Gulf carriers in the first eleven months of 2025, more than double the 21 delivered in all of 2024.7 Emirates alone received 13 A350-900s, nearly a quarter of global A350 output.8 The region generates roughly 17% of global airline profits.9

For 2026, an estimated 95–100 Airbus deliveries were scheduled for Middle Eastern carriers, 11–12% of the 870-unit target.10

Emirates has 60 A350-900s remaining from a 73-aircraft order.11 Qatar Airways has 50 A321neos beginning delivery in 2026.12 Etihad ordered 27 A350-1000s, 15 A330-900s, and 10 A350Fs at the November 2025 Dubai Airshow.13

Turkish Airlines, the largest A350 customer worldwide with 504 Airbus aircraft on order, operates from an Istanbul hub outside the conflict zone; its exposure is limited to airspace rerouting rather than infrastructure damage.14

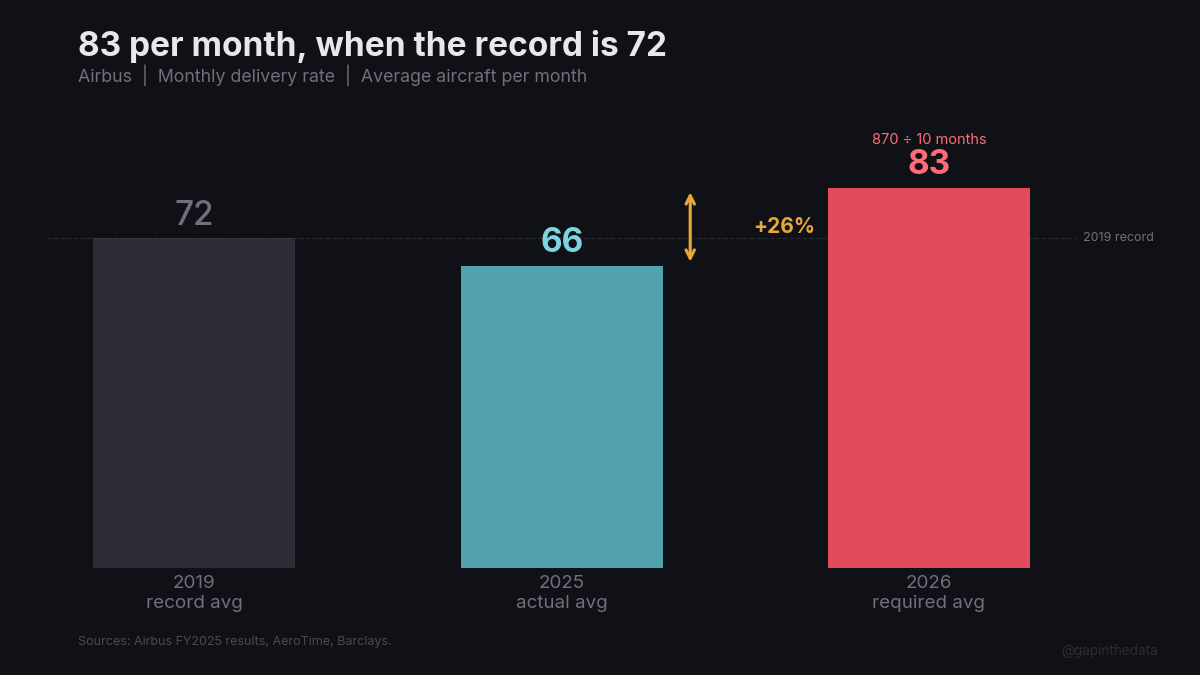

January 2026 deliveries were 19 units, the lowest since April 2020.15 To reach 870, Airbus needs 83 deliveries per month from March through December.16 In 2019, its record year, the monthly average was 72.17 Airbus delivered 136 aircraft in December 2025, or 17.2% of its annual total, though the December sprint has been a recurring pattern rather than evidence of a sustained production rate.69

Each delivered aircraft contributes roughly €6.90 million in EBIT Adjusted.70 The 95–100 estimated Middle Eastern deliveries therefore represent €655–690 million in annual EBIT contribution, or 8.7–9.2% of the 2026 guided total.

Historical precedent suggests the demand environment can shift rapidly. In the 1990 Gulf War, Airbus new orders fell 75% in a single year, from 404 to 101; in the 2008 oil spike, Boeing new orders fell 90%, from 1,413 to 142.71 New orders are not deliveries, but they shape the commercial leverage under which delivery schedules are renegotiated.

III. Three chokepoints

Three major maritime energy chokepoints are simultaneously disrupted.

The Strait of Hormuz. The IRGC issued a VHF radio warning on February 28: “No ship is allowed to pass."18 The strait handles 20 million barrels per day of crude, condensate, and petroleum products, roughly 20% of global consumption, along with 20% of global LNG trade.19

Jet fuel transits Hormuz at 400,000 barrels per day, mostly to Europe, alongside 400,000 barrels per day of diesel.20 At least 150 tankers were anchored in open Gulf waters. 170 containerships, representing 450,000 TEU, were trapped inside.21

Two bypass pipelines, one Saudi and one Emirati, together provide 3.5–4.2 million barrels per day of spare capacity, covering less than 20% of Hormuz flows.22 Neither handles refined products, and no bypass exists for LNG.23

The Strait has never been fully closed. In the 1984–1988 Tanker War, 411 ships were attacked and 239 petroleum tankers hit, yet oil continued to flow.24 Iran itself exports 1.5 million barrels per day through Hormuz, 90% to China.67 A sustained full closure would devastate Iran’s own revenue.

The operative distinction is between physical blockade and economic closure. Marine insurers have cancelled existing policies for Persian Gulf vessels outright, rather than repricing them.25 Aviation war risk insurance carries a standard 7-day cancellation clause, which means that repricing raises costs but cancellation halts operations entirely.26

After Russia’s 2022 invasion of Ukraine, roughly 500 foreign-owned aircraft valued at $10 billion were effectively seized.^72^ DAE Capital, the largest Middle East-based lessor with a $22 billion fleet, is headquartered in Dubai.58

The Red Sea. Houthi attacks, subject to a fragile ceasefire with the Trump administration, resumed following the strikes.27 The Cape of Good Hope alternative adds 10–14 days and $1 million per voyage, reducing effective global shipping capacity by up to 15%.28

The Bosphorus. Transit has been constrained since Russia’s 2022 invasion of Ukraine under Montreux Convention restrictions.29 The Bosphorus is not an active flashpoint, but its ongoing constraint means that the third major energy corridor into Europe was already degraded before the first two came under pressure.

The consequence is cumulative. EU gas storage stands at 30% of capacity, down from 52% a year ago and 72% two years ago, the lowest at this point in the heating season in at least three years.30

Qatar supplies 45% of Italy’s LNG, 38% of Belgium’s, 38% of Poland’s.31 ICIS modelling indicates a 102-day halt of Qatari LNG would push TTF gas prices to €86–92 per megawatt-hour, a threefold increase.32

Container rates from Shanghai to Jebel Ali have risen 55% month-over-month to $4,200 per forty-foot equivalent unit.33 VLCC tanker spot rates on Middle East-to-China routes surged 154% week-over-week.34

IV. What Gulf carriers have, and what they don’t

The three major Gulf carriers enter this crisis in the strongest financial positions in their histories.

Emirates reported $5.2 billion in profit for FY2024/25 and holds $15.2 billion in cash.35 Qatar Airways earned $2.15 billion, backed by the Qatar Investment Authority's $557 billion in sovereign assets.36 Etihad, which was upgraded to AA- by Fitch in December after reducing net leverage from 5.0x to 1.1x over three years, posted $698 million in profit.37

None are publicly traded; all are wholly owned by sovereign entities.38

At $78--80 million per day in operating costs, Emirates can sustain roughly 190 days of zero revenue on its $15.2 billion cash balance without state support.39 The relevant question is not whether these carriers survive but whether carriers entering cash-preservation mode defer aircraft they cannot profitably deploy. Emirates does not hedge fuel costs.73

The COVID precedent is imperfect. Emirates lost $6 billion in FY2020/21, received $8.9 billion in state support, cut nearly 30,000 staff, and recovered to record profits by FY2023/24.40 COVID-era cash reserves were roughly one-quarter of current levels.41

But COVID did not damage airports, and operations resumed the moment policy allowed. Terminal damage requires physical repair; the Sanaa Airport, struck in 2025, sustained an estimated $500 million in damage.42

During COVID, Emirates deferred 777X orders, Qatar demanded deferrals, and Etihad cancelled 16 Boeing widebodies.43 All three subsequently returned to record ordering, because the deferrals were temporary and so was the disruption. A war that damages airports changes the calculus of when and whether operations restart.

Dubai’s economy is 27% dependent on aviation.44 Petroleum contributes less than 6% of GDP.45 The city’s $135 billion debt load represents 125% of GDP, serviced by an economy built around connectivity.46

In 2009, when Dubai World requested a standstill on $59 billion in debt, Abu Dhabi provided $10 billion and stated: “It does not mean that Abu Dhabi will underwrite all of their debts."47

V. The supply chain through the conflict

The war intersects with a supply chain dependency detailed in The Tianjin Trap. AVIC, Airbus’s largest non-engine supplier, is already under formal Congressional scrutiny.

All eleven Republican members of the House Select Committee on China have requested the Treasury Department investigate AVIC.48 The basis: AVIC subsidiary Harbin Aircraft Industry Co. sells aircraft to the IRGC Aerospace Force.49 CAATSA and IFCA provide the legal framework for mandatory secondary sanctions against entities doing significant business with Iran’s defence sector.50

The diplomatic context sharpened on February 28. China’s Foreign Ministry called the strikes a “flagrant violation” of the UN Charter.51 China, Russia, and Iran conducted joint naval exercises in the Strait of Hormuz earlier in February.52

AVIC’s Harbin facility is the exclusive worldwide supplier of four critical A350 composite structures: the rudder, elevator, belly fairing, and S19 maintenance door.53 No alternative supplier exists, and qualifying one would take 18 to 36 months. China controls 75% of global titanium metals production.54 Airbus still sources roughly 20% of its titanium from Russia.55

The 500-aircraft mega-order, reportedly completed in June 2025 but held for “the right timing,” has been announced in stages linked to diplomatic visits.56 On February 25, three days before the strikes, German Chancellor Merz secured 120 aircraft during a Beijing visit.57 The remaining 380 have not been formally announced.

Airbus’s 8,754-aircraft backlog provides a theoretical demand buffer, and delivery slots deferred by Gulf carriers can in principle be reallocated.64 Within the narrowbody backlog, the waitlist stretches years and reallocation is straightforward. Widebodies are different. Airbus delivered 57 A350s in 2025, of which Emirates took 13, or 22.8% of total output.8 Other A350 customers, including Turkish Airlines, Cathay Pacific, and Japan Airlines, have publicly sought earlier delivery positions, and some slots could shift to willing buyers.74 But airline-specific configurations, completion timelines, and engine selections constrain the speed of reallocation, and any slot that slips from the 2026 calendar year reduces output against the 870 target regardless of whether it finds another customer.

Airbus Defence & Space generated €798 million in EBIT on €13.4 billion in revenue in FY2025, a 6.0% margin, on record order intake of €17.7 billion.6 65 European defence spending is accelerating, with the EU SAFE facility providing €150 billion in dedicated financing, and D&S margins are expanding from a base that was negative as recently as FY2024.66 The division’s entire FY2025 profit is comparable in scale to the EBIT contribution of the Gulf delivery schedule, and defence spending is growing; whether that growth translates to margins remains a function of execution on historically challenging programmes.

The engine constraint, the supply chain dependency, the margin dilution, and the delivery shortfall were four analyses of four separate problems. They now share a trigger.

The 2026 guidance was published nine days before the strikes. It assumes “no additional disruptions to global trade or the world economy, air traffic, the supply chain."2

Footnotes

1 Airbus SE, “Airbus Reports Full-Year (FY) 2025 Results,” February 19, 2026. Guidance: ~870 deliveries, ~€7.5B EBIT Adjusted, ~€4.5B FCF before customer financing.

2 Airbus SE, FY2025 press release, guidance assumptions section: “no additional disruptions to global trade or the world economy, air traffic, the supply chain.”

3 Bloomberg, “Busiest Global Airports Shut Down as Iran Strikes US Gulf Bases,” February 28, 2026 (Abu Dhabi: 1 killed, 7 injured). Al Jazeera, “Airspace Closed, Airlines Halt Flights as US-Israel Attack Iran,” February 28, 2026 (Bahrain damage confirmed). AirLive, “Kuwait International Airport Struck by Iranian Suicide Drone,” February 28, 2026 (Terminal 1, 12 injured). Aviation A2Z, “Dubai Airport Hit Amid Regional Strikes,” March 1, 2026 (Terminal 3, 4 staff injured).

4 DJ’s Aviation, “All Emirates Aircraft Are Grounded,” February 28, 2026.

5 Cirium data, reported via Al Jazeera, February 28, 2026. Eight countries closed airspace: Bahrain, Kuwait, Qatar, UAE, Iraq, Israel, Iran, and Jordan.

6 Airbus FY2025 results. Commercial Aircraft: 72% of revenue, 76.7% of EBIT Adjusted. D&S: 18% of revenue, 11.2% of EBIT Adjusted at 6.0% margin. See Thirty-Three Percent.

7 Leeham News, January 12, 2026. 43 aircraft to Gulf carriers Jan–Nov 2025 versus 21 in all of 2024.

8 Leeham News, January 12, 2026. Emirates: 13 A350-900 deliveries in 2025. Total A350 deliveries (all variants): 57. Emirates share: 13/57 = 22.8%.

9 IATA, “Airline Industry Economic Performance,” December 2025. Middle East carriers: roughly 17% of global airline net profits.

10 Author’s estimate based on 2025 delivery run rate, carrier order timelines, and production schedules. Total Middle East deliveries (both OEMs) estimated at 180–220 (Linus Bauer aviation consultancy); Airbus share roughly 60%.

11 Emirates, “Emirates Orders 8 Additional Airbus A350-900 Aircraft,” Dubai Airshow, November 2025. Total order: 73 A350-900s; 60 remaining.

12 One Mile at a Time, “Qatar Airways A350/A321 Order Reinstated,” 2025. 50 A321neos (40 A321neo + 10 A321LR).

13 Etihad, “Etihad Expands Widebody Fleet with 32 New Airbus Aircraft Arriving from 2027,” Dubai Airshow, November 2025. 27 A350-1000 + 15 A330-900 + 10 A350F.

14 Turkish Airlines, December 2023 order: 220 aircraft (150 A321s + 70 A350s). Total Airbus order book: 504 aircraft including 110 A350s, the largest A350 customer worldwide.

15 Airbus January 2026 deliveries: 19 aircraft, 15 customers. AeroTime, February 7, 2026.

16 Calculation: 870 target minus 19 (January) minus estimated February = roughly 830 remaining over 10 months = 83/month. See also Barclays: “expected 2026 delivery profile is likely to be back-end-loaded again.”

17 2019: 863 aircraft / 12 months = 71.9 per month. Airbus historical delivery data.

18 Bloomberg, “IRGC Declares Hormuz Closed,” February 28, 2026. VHF radio warning also reported by Al Jazeera and maritime tracking services.

19 EIA, “The Strait of Hormuz Is the World’s Most Important Oil Transit Chokepoint,” updated 2024. Roughly 20M b/d total throughput; 20% of global petroleum consumption; 20% of global LNG.

20 EIA; Kpler trade flow data. Jet fuel roughly 400K b/d, diesel roughly 400K b/d transiting Hormuz, primarily to European destinations.

21 Lloyd’s List, February 28, 2026 (170 containerships, 450,000 TEU trapped inside the Gulf). Tanker Trackers / maritime AIS data (150+ tankers anchored in open Gulf waters).

22 EIA; Saudi Aramco East-West Pipeline disclosures; ADNOC Habshan-Fujairah Pipeline data. Combined spare capacity: 3.5–4.2M b/d.

23 EIA. All Qatari and UAE LNG exports transit Hormuz. No pipeline bypass exists for liquefied natural gas.

24 Lloyd’s War Risks data, 1984–1988. 411 ships attacked; 239 petroleum tankers hit; roughly 430 civilian sailors killed.

25 RegTechTimes, “Shipping Shock: Insurers Cancel Gulf Policies,” March 2026. Policies cancelled outright, not repriced.

26 AVN48B war exclusion clause; standard 7-day cancellation notice provision. The National, “Airlines and War Risk Insurance,” February 21, 2026.

27 Al Jazeera, “Houthi Attacks Resume Following US-Israel Strikes on Iran,” February 28, 2026.

28 Drewry, “Red Sea Rerouting Impact Assessment,” 2025. Cape of Good Hope alternative: +10–14 days, roughly +$1M per voyage. Effective global shipping capacity reduction up to 15%.

29 Lloyd’s List, “Black Sea Shipping Constraints,” 2026. Bosphorus transit restrictions under the Montreux Convention during the Russia-Ukraine conflict.

30 Gas Infrastructure Europe (GIE) data. EU storage at February 27, 2026: 30.09%. February 2025: roughly 52%. February 2024: roughly 72%.

31 Eurostat LNG import data. Qatar share: Italy 45%, Belgium 38%, Poland 38%.

32 ICIS, European energy modelling. 102-day Qatari LNG halt: TTF to €86–92/MWh from roughly €31–32. For reference, the 2022 crisis peak was roughly €340/MWh.

33 Freightos/Drewry container rate indices. Shanghai–Jebel Ali: +55% MoM to roughly $4,200/FEU.

34 Baltic Exchange. VLCC Middle East–China spot rates: +154% week-over-week.

35 Emirates Group, FY2024/25 results (year ended March 31, 2025). Revenue AED 145.4B ($39.6B); profit after tax AED 19.1B ($5.2B); cash AED 56.0B ($15.2B, as of September 2025 half-year).

36 Qatar Airways, FY2024/25 results. Revenue QAR 86B ($23.6B); net profit QAR 7.85B ($2.15B). QIA AUM per Sovereign Wealth Fund Institute.

37 Etihad Airways, FY2025 results (calendar year). Revenue AED 30.7B ($8.4B); profit AED 2.6B ($698M). Fitch upgrade to AA- December 2025. Net leverage: 5.0x (2022) to 1.1x (Q1 2025).

38 Emirates: Investment Corporation of Dubai. Qatar Airways: Qatar Investment Authority. Etihad: ADQ / L’imad Holding Company.

39 Author’s calculation: Emirates FY2024/25 operating costs roughly $28.7B / 365 = roughly $78–80M/day. Cash of $15.2B / $80M = 190 days.

40 Emirates FY2020/21: loss AED 22.1B ($6.0B); received $4.1B initial bailout, expanded to $8.9B total. Workforce cut from 105,000 to 75,000.

41 Emirates cash at COVID onset: roughly $4.1B. Current: $15.2B. Ratio: 3.7x.

42 Al Jazeera, “Sanaa Airport Damage Assessment,” 2025. Estimated $500M in damage; Yemeni officials cited “considerable time to restore full functionality.”

43 Emirates: deferred 777X orders, converted some to 787s; subsequently reversed. Qatar Airways: demanded deferrals until 2022. Etihad: cancelled 16 Boeing widebodies. All three returned to record ordering by 2024–2025.

44 Dubai Aviation Corporation; Oxford Economics, “Dubai Aviation Impact Study,” 2023. Aviation: 27% of GDP; 631,000 jobs.

45 UAE Federal Competitiveness and Statistics Centre. Petroleum: less than 6% of Dubai GDP.

46 IMF Article IV data; Dubai government disclosures. Total debt: roughly $135B, roughly 125% of GDP.

47 Reuters, December 2009. Abu Dhabi provided $10B for Dubai World's $59B debt. Quote per Financial Times and Wall Street Journal reporting.

48 House Select Committee on the Chinese Communist Party, press release, 2025. All 11 Republican members requested Treasury investigate AVIC.

49 House Select Committee. AVIC subsidiary Harbin Aircraft Industry Co. supplies aircraft to IRGC Aerospace Force.

50 CAATSA (Countering America’s Adversaries Through Sanctions Act) and IFCA (Iran Freedom and Counter-Proliferation Act). Framework for mandatory secondary sanctions against entities doing significant business with Iran’s defence sector.

51 Chinese Foreign Ministry statement, February 28, 2026. “Highly concerned”; “immediate stop of military actions”; “flagrant violation” of the UN Charter.

52 Reuters, “Maritime Security Belt 2026: China, Russia, Iran Conduct Joint Naval Exercises in Strait of Hormuz,” February 2026.

53 Xinhua, June 10, 2019. Harbin Hafei Airbus Composite Manufacturing Centre: sole worldwide composite structure supplier for A350 rudder, elevator, belly fairing, and S19 maintenance door. AVIC subsidiaries hold roughly 70% ownership; Airbus 29%. See The Tianjin Trap footnotes 12–14.

54 AeroTime, “Global Titanium Market at Risk of Tightening as China-Russia Grip Persists,” 2025. China: 75% of global titanium metals production, up from 40% in 2019.

55 Airbus supply chain disclosures; industry reporting. VSMPO-AVISMA: roughly 20% of Airbus titanium (down from 60%).

56 Bloomberg, August 22, 2025. Deal for roughly 500 aircraft completed June 2025; not officially announced.

57 Reuters, “Germany’s Merz Secures 120 Airbus Aircraft in Beijing Visit,” February 25, 2026.

58 DAE Capital: roughly 750 aircraft, $22B fleet value. Owned by Investment Corporation of Dubai. Headquarters: Dubai.

64 Airbus SE, FY2025 press release. Consolidated order book: 8,754 aircraft at December 31, 2025.

65 Airbus SE, FY2025 press release. D&S order intake: €17.7 billion (record). D&S contributed 76.9% of group EBIT Adjusted year-over-year improvement. See Thirty-Three Percent.

66 European Commission, “SAFE: Supporting the Acceleration of European Defence Equipment,” 2026. €150 billion loan facility with “Buy European” procurement rules.

67 EIA. Iran crude oil exports roughly 1.5 million barrels per day, roughly 90% to China. All transit the Strait of Hormuz.

68 Iranian state media, March 1, 2026. Supreme Leader Khamenei confirmed killed. Critical Threats (AEI/ISW), “Iran Update,” February 28, 2026: Chief of Staff Mousavi killed; Defence Minister Nasirzadeh likely killed; IRGC Commander Pakpour likely killed. Provisional Leadership Council formed (Arafi, Pezeshkian, Mohseni-Eje’i); ceasefire authority unclear.

69 Airbus FY2025 monthly delivery data. December 2025: 136 aircraft delivered, or 17.2% of the 793-aircraft annual total (136/793 = 17.2%). See What Safran Can’t Fix.

70 Computation: FY2025 Commercial Aircraft EBIT Adjusted (€5,470M) / FY2025 deliveries (793) = €6.90M per aircraft. Applied to 95–100 estimated Middle Eastern deliveries: 95 × €6.90M = €655M; 100 × €6.90M = €690M. As percentage of 2026 EBIT Adjusted guidance (€7,500M): €655M/€7,500M = 8.7%; €690M/€7,500M = 9.2%. See Thirty-Three Percent and footnote 10.

71 IATA World Air Transport Statistics; Airbus/Boeing historical orders & deliveries data. 1990: Airbus orders fell from 404 (1989) to 101 (1991). 2008: Boeing orders fell from 1,413 (2007) to 142 (2009).

72 AerCap, “Russia-Ukraine Conflict: Aircraft Update,” 2022–2024. Approximately 500 foreign-owned aircraft (AerCap: 152 aircraft, roughly $2.1B) trapped by Russian legislation prohibiting aircraft export (enacted March 10, 2022). Total industry losses estimated at $10B+.

73 Emirates Group Annual Reports. Emirates maintains a stated policy of not using fuel hedging instruments, relying instead on operational efficiency and fare adjustments.

74 Turkish Airlines, Cathay Pacific, Japan Airlines, and Singapore Airlines have all publicly expressed interest in accelerating A350 delivery positions. See industry reporting from Leeham News and FlightGlobal, 2025–2026.