Three loss-making ramps, one structural paradox.

Part II of III, following The Tianjin Trap

On February 19, 2026, Airbus reported record results, with revenue rising 6% to €73.4 billion and EBIT Adjusted reaching €7,128 million, up 33%.1

The market saw what the headline obscured. As detailed previously, seventy-seven percent of the group’s EBIT improvement came from Defence & Space normalising from its 2024 loss rather than from commercial aircraft expanding margins.1 On a reported basis, commercial aircraft EBIT declined 11.3%, from €5,133 million to €4,555 million, even as the company delivered 27 more aircraft.1

The record headline is a normalisation story, and underneath it the commercial aircraft business is fighting margin compression that gets worse as deliveries increase.

The three ramps

Airbus is ramping three loss-making programmes simultaneously. None has reached the production rate at which it becomes margin-accretive. Every additional delivery dilutes the average.

The A350 was producing approximately ten aircraft per month before the pandemic.2 By 2024, the rate had recovered to roughly six,2 and the target was eight per month in 2025.3 Airbus delivered 57, an average of 4.75 per month.1 Forecast International described the performance as showing “no signs of stabilizing, even at the six-per-month rate."4 The rate 12 target remains officially at 2028, though Forecast International believes 2029 is more realistic.5 In February 2026, Faury told analysts he wants “significantly higher rates,” even as the programme contends with both production shortfalls and a series of airworthiness directives that compound the ramp challenge.6

Every A350 below rate absorbs disproportionate fixed costs. And because A350s are entering the delivery mix in growing numbers relative to mature A320s, every month below target appears in the financial statements as what Airbus itself calls “an unfavourable mix."7 Demand fragility compounds the problem: United Airlines has effectively removed 45 A350-900s from its fleet plans, forty-five fewer airframes over which to amortise ramp costs at exactly the wrong moment.

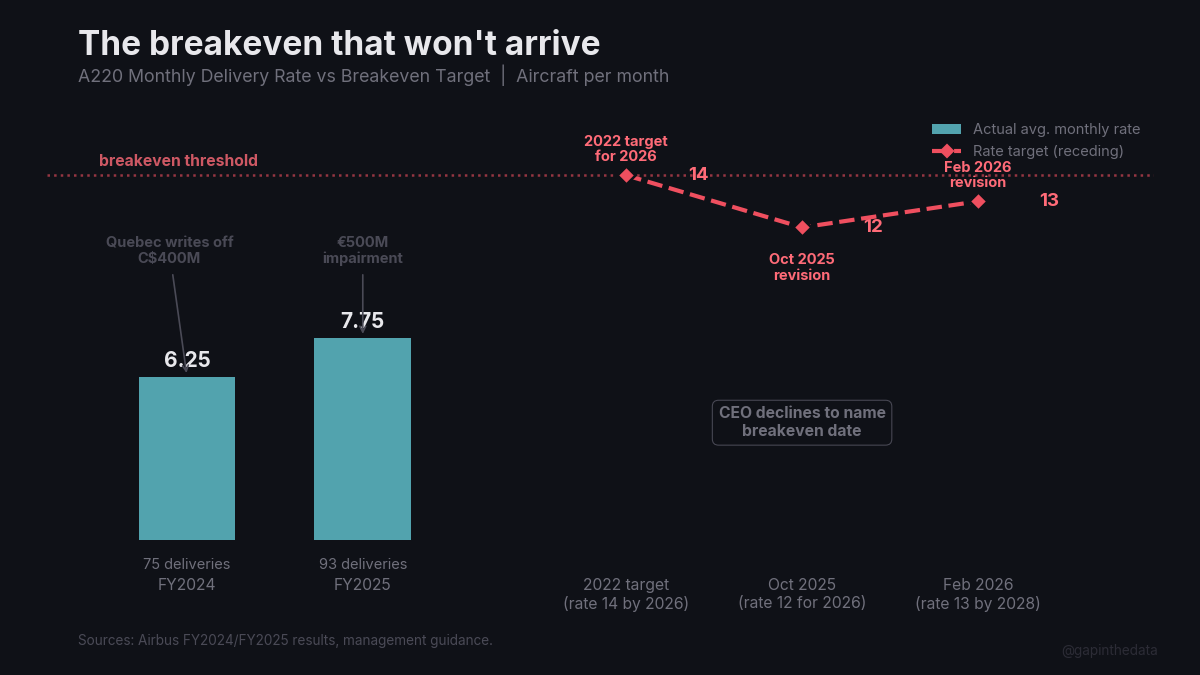

The A220 has been under Airbus ownership for seven years and is still losing money on every airframe delivered.8 In FY2025, Airbus recorded a €500 million impairment of programme assets, triggered by “significant updates to the programme’s long-term business case."9 Quebec wrote off approximately C$400 million from its investment, acknowledging it was unlikely to recover half the funds injected.10

Industry estimates place the breakeven at approximately rate 14, or fourteen aircraft per month.11 That target has moved in the wrong direction: from 14, to 12 for 2026, to 13 by 2028.1 11 The CEO of Airbus publicly declined to provide a breakeven date for a programme the company has operated for seven years.11 The A220’s problems are compounded by the PW1500G engine crisis, which has grounded roughly 22% of the global fleet, with turnaround times stretching to 300 days.12

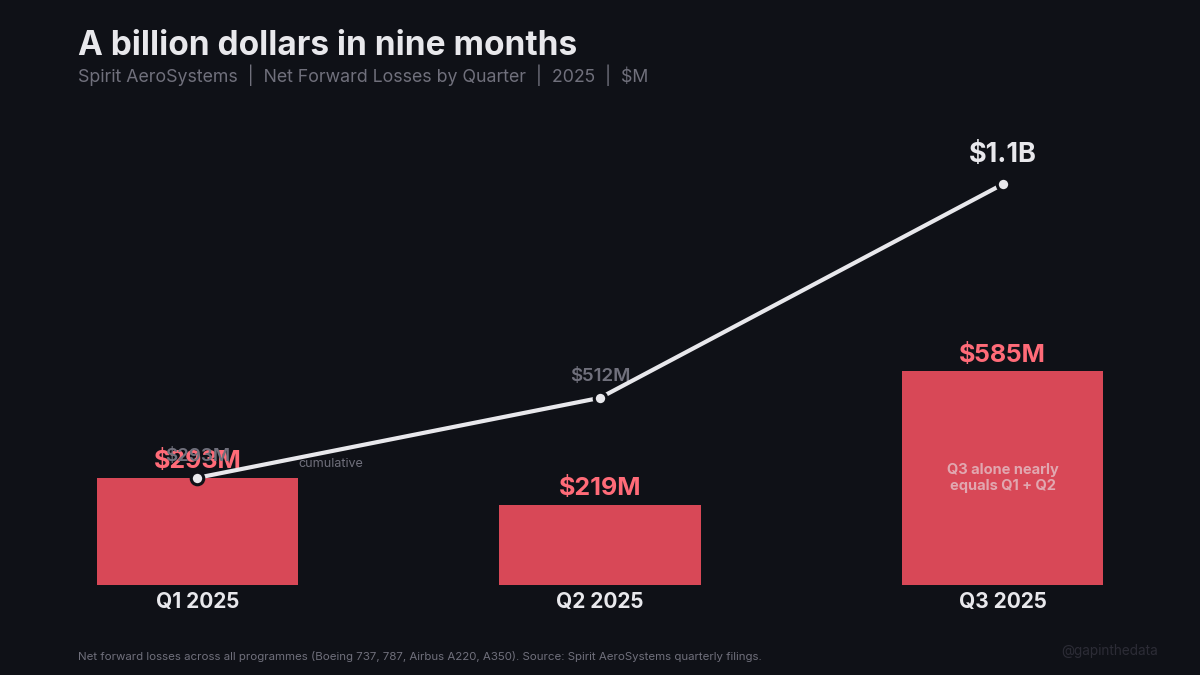

Spirit AeroSystems was a rescue. The company had disclosed going-concern doubt in every quarterly filing throughout 2025 and booked more than $1 billion in forward losses across its contract portfolio, driven by the same Boeing and Airbus programmes it was supplying.13 Airbus acquired Spirit’s work packages for the A220, A320, and A350, bringing five sites and over 4,000 employees.9

The financial impact amounted to a €500 million A220 impairment, €249 million in onerous contract provisions, and €122 million in transaction costs, partially offset by a €738 million accounting gain from settling pre-existing supply contracts.9 CFO Toepfer described the turnaround as requiring “about three years,” with “mid-triple-digit million” negative cash flow in both 2026 and 2027.9

The structural problem is that Spirit’s Airbus work packages were loss-making before Airbus acquired them. Spirit stated publicly that the lack of price increases on Airbus programmes had depressed cash flows.13 Bringing them in-house moves the losses to a different line of Airbus’s financial statements. Spirit’s constraint on A350 fuselage panels is the primary reason the A350 cannot reach rate.5

What appears to be three parallel problems is in substance one problem expressed three ways. Spirit constrains the A350 rate, Spirit’s integration delays the A220 breakeven, and both programmes dilute the delivery mix that determines group margins. The ramps feed each other.

The constraint

The A320 family, the one programme at mature margins and the only one that could dilute the problem, is itself constrained.

Pratt & Whitney supplies engines for approximately 40% of A320neo-family production and has not finalised supply volumes for 2026 or 2027.14 As detailed in “What Safran Can’t Fix,” even CFM’s LEAP acceleration does not translate to Airbus deliveries, because five competing claims share every engine produced. Airbus guided approximately 870 deliveries for 2026, well above the pace implied by its opening months and current constraints.15 The programme that could rescue the mix is constrained by a supplier Airbus cannot control. Meanwhile, the A321XLR, the highest-margin narrowbody variant, keeps losing customers to delays and seat certification problems.

The bridge

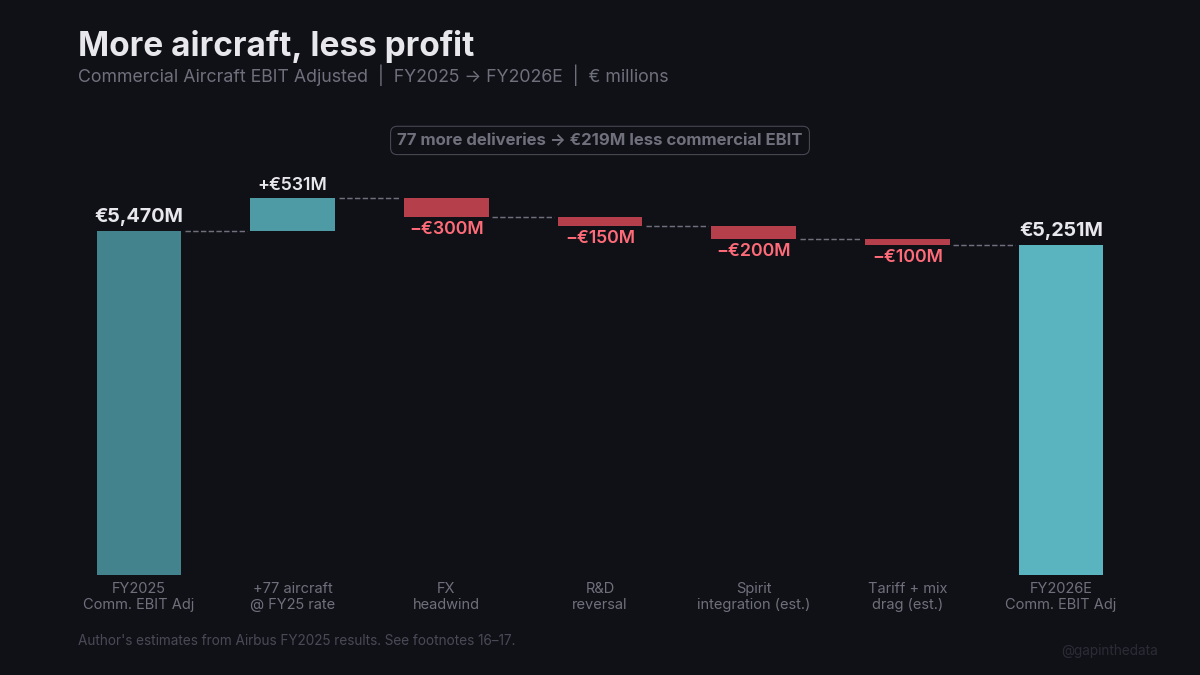

The 2026 guidance math confirms the trajectory. Airbus guided €7.5 billion in group EBIT Adjusted on approximately 870 deliveries, 77 more than FY2025.1 That implies €4.83 million in incremental group EBIT per additional aircraft, well below the FY2025 commercial aircraft average of €6.90 million.16 On a commercial-aircraft-only basis, the bridge is starker: EBIT declines €219 million despite 77 more deliveries.

The headwinds are identified and quantified: FX drag of approximately €300 million; R&D expenses set to increase after a 3% decline in 2025; Spirit integration costs “slightly higher than anticipated”; tariff impacts continuing; the P&W engine constraint limiting the one segment at mature margins.1 9 16

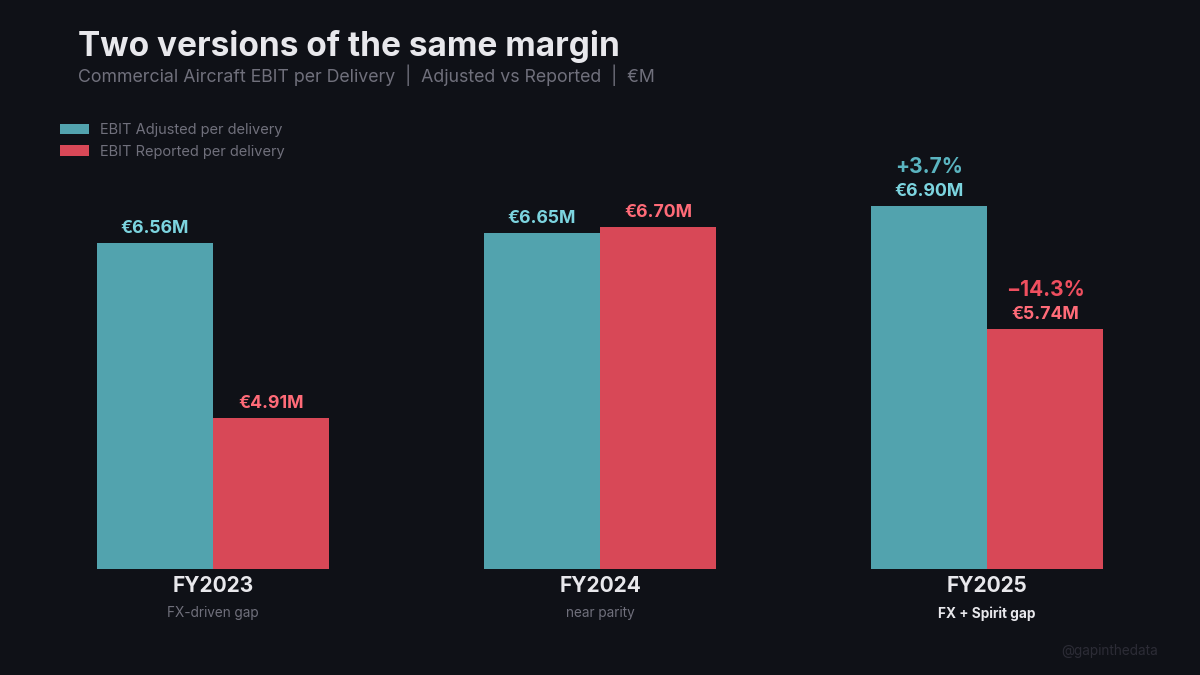

On a per-aircraft basis, reported earnings fell nearly €1 million year-on-year, from €6.70 million in FY2024 to €5.74 million in FY2025, a decline of 14.3%.17 The adjustments that maintain the “stable margin” narrative, in particular the €624 million in FX effects and the €188 million in Spirit charges, are doing enormous work.17 Remove them, and the margin compression is visible on every airframe.

Analyst models adjusted quickly after the guidance update, with UBS cutting its EBIT estimate by approximately €400 million and Oddo BHF expecting broader estimate cuts of roughly 10%.15

Footnotes

1 Airbus, “Airbus Reports Full-Year (FY) 2025 Results,” February 19, 2026. Revenue €73,420M (+6%); EBIT Adjusted €7,128M (+33%); commercial aircraft EBIT Adjusted €5,470M (+7.4%); commercial aircraft EBIT reported €4,555M (−11.3%); 793 deliveries (93 A220s, 607 A320 Family, 36 A330s, 57 A350s); D&S EBIT Adjusted €798M (2024: −€566M). 2026 guidance: ~870 deliveries, ~€7.5B EBIT Adjusted. A320 rate 70–75 by end 2027. A220 rate 13 by 2028.

2 ePlaneAI, “Annual Production Rate of Airbus A350 Aircraft,” August 30, 2025. Pre-pandemic peak of ~10/month in 2019; pandemic low of ~5/month; 2024 output approximately six per month.

3 Aviation Source News, “Airbus Targets 820 Deliveries in 2025,” February 21, 2025. AeroTime, “What to Expect from Airbus in 2025,” December 31, 2024. Estimated target of eight A350s per month in 2025.

4 Forecast International, “Airbus and Boeing October 2025 Production Rates,” November 3, 2025. A350 averaged 4.5 per month through October 2025; “no signs of stabilizing, even at the six-per-month rate.”

5 Forecast International, “Supply Chain Challenges Limit A350 Production to Six Aircraft Per Month,” February 26, 2025. A350 limited to ~6/month in 2025; supply chain disruptions stemming from Spirit AeroSystems; rate 12 likely not before 2029.

6 Aviation Week, “Airbus Seeks Higher A350 Rates Despite Supply Constraints,” February 2026. Faury stated Airbus wants “significantly higher rates” for the A350. Transcript accessed via Aviation Week Intelligence Network.

7 Airbus, “Airbus Reports Nine-Month (9M) 2025 Results,” October 29, 2025. “Increase of deliveries embeds an unfavourable mix.”

8 Wikipedia, “Airbus A220,” accessed February 2026. Airbus acquired controlling stake 2018; increased to 75% in 2020. Over 940 orders.

9 Airbus FY2025 Financial Statements, February 19, 2026. Spirit acquisition impact: +€738M gain (pre-existing relationship settlement), −€500M A220 impairment, −€249M onerous contract provisions, −€122M transaction costs, and other adjustments; net −€188M. Five sites, 4,000+ employees. CFO Toepfer: turnaround “about three years”; “mid-triple-digit million” negative cash flow in 2026–27; integration costs “slightly higher in 2026 than anticipated.” Sources: Airbus press release, MarketScreener.

10 ch-aviation, “Québec Writes Off US$285M in A220 Programme,” October 13, 2025. C$400M write-down.

11 Flight Global, “Airbus Trims A220 Production Targets Over Supply and Demand Considerations,” October 30, 2025. Rate 12 target for 2026 (down from 14). Faury: Spirit integration “changing a bit the picture” on breakeven; “a bit premature to be more specific on a date.”

12 Lara News, “Airbus Pushes A220 Production Target Back,” November 3, 2025. ~22% of global A220 fleet grounded; turnaround ~300 days. Air France-KLM confirmed 21% of its own A220 fleet grounded with 42% requiring inspections (FY2025 results coverage).

13 Spirit AeroSystems, “Q1 2025 Results,” May 1, 2025; “Q3 2025 Results,” Q3 2025. Going concern doubt; forward losses: $293M (Q1), $219M (Q2), $585M (Q3); total $1,097M through 9M 2025. “Lack of price increases on Airbus programs” cited as depressing cash flows.

14 Airbus, production ramp-up disclosures, October 2025 and February 2026. P&W supplies ~40% of A320neo-family engines. Supply volumes for 2026–2027 not finalised. In the FY2025 earnings call, Faury stated: “P&W has resigned from the orders we had placed and they had accepted for the volumes in 2026” (transcript excerpt; full transcript). Sources: Airbus newsroom, CNBC.

15 Market and analyst reaction, February 19, 2026. 870 deliveries vs ~907 consensus; UBS cut EBIT estimate by ~€400M; Oddo BHF expects ~10% consensus cuts. Sources: Investing.com, MarketScreener. See also our initial analysis.

16 Author’s analysis from Airbus FY2025 results and 2026 guidance. Group incremental EBIT: €7,500M − €7,128M = €372M on 77 deliveries = €4.83M per aircraft. FY2025 commercial average: €5,470M / 793 = €6.90M. Commercial aircraft EBIT bridge (author’s estimate): €5,470M → €5,251M, a decline of €219M despite +77 deliveries. FX headwind ~€300M; R&D increasing (FY2025: €3,153M, −3% YoY).

17 Author’s calculations from Airbus annual results. EBIT Adjusted per aircraft: €6.90M (2025), €6.65M (2024). EBIT Reported per aircraft: €5.74M (2025, −14.3%), €6.70M (2024). Adjusted-reported gap: ~€40M (2024) to €915M (2025). Gap composition: €624M FX + €188M Spirit charges. CFO Toepfer: “margin in commercial is not particularly affected, on a per aircraft basis.”

18 Airbus SE enterprise value ~€130B on trailing revenue of €73.4B (~1.8x) as of February 2026.