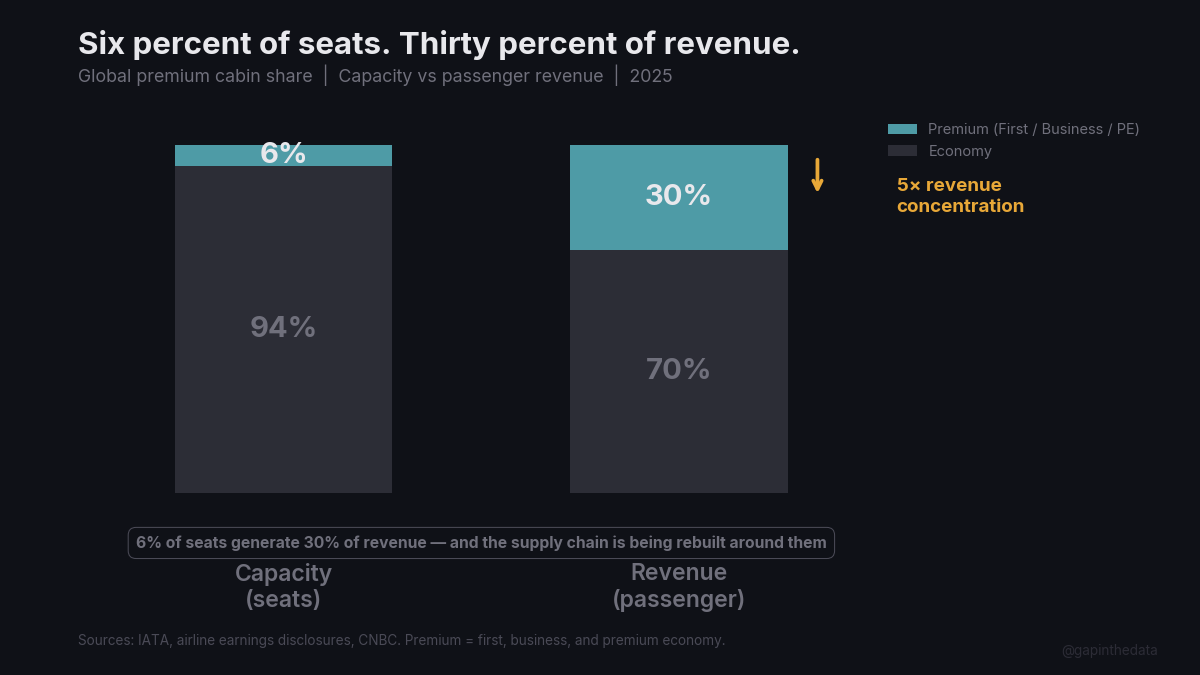

Premium seats occupy 6% of global capacity but generate 30% of passenger revenue.1 The entire aerospace supply chain is being restructured around this 6%: increasing per-unit labor, thinning margins, and locking OEMs into irreversible commitments. All of it built on four years of post-pandemic data with no recession precedent.

A companion to Thirty-Three Percent and The Margin Trap

I. The Reconfiguration

The top 10% of U.S. households now account for nearly 50% of all consumer spending.2 Airlines are following the money through labor costs and seat economics, not pricing algorithms.

In Q3 2025, Delta’s premium cabin revenue surpassed main cabin revenue for the first time in the airline’s 100-year history, two years ahead of plan.3 Full-year premium revenue grew 7% to $22.1 billion while main cabin revenue declined 5%.4 American’s new A321XLR carries just 155 seats: 20 lie-flat Flagship Suites, 12 premium economy, 123 main cabin, 30% fewer seats than a single-class A321neo.5 United’s calculus is explicit: “an 80% full premium plane is more profitable than a 100% full economy plane."6

Southwest ended 50 years of open seating and added premium seats; its stock surged 17%.7 Spirit Airlines, in its second bankruptcy, is shrinking from 214 to 94 aircraft while pivoting to premium.8 Frontier lost $76 million in Q3 2025 and is debuting “First Class” in 2026.9 JetBlue will launch domestic business class by mid-2026.10

The consultant Robert Mann: “the airline version of the K-shaped economy: monetize the top of the K and minimize the shortfall at the bottom."11 Delta CEO Ed Bastian was blunter: “The strength in the consumer sector is at the higher end of the curve. The lower-end consumer is struggling greatly."4

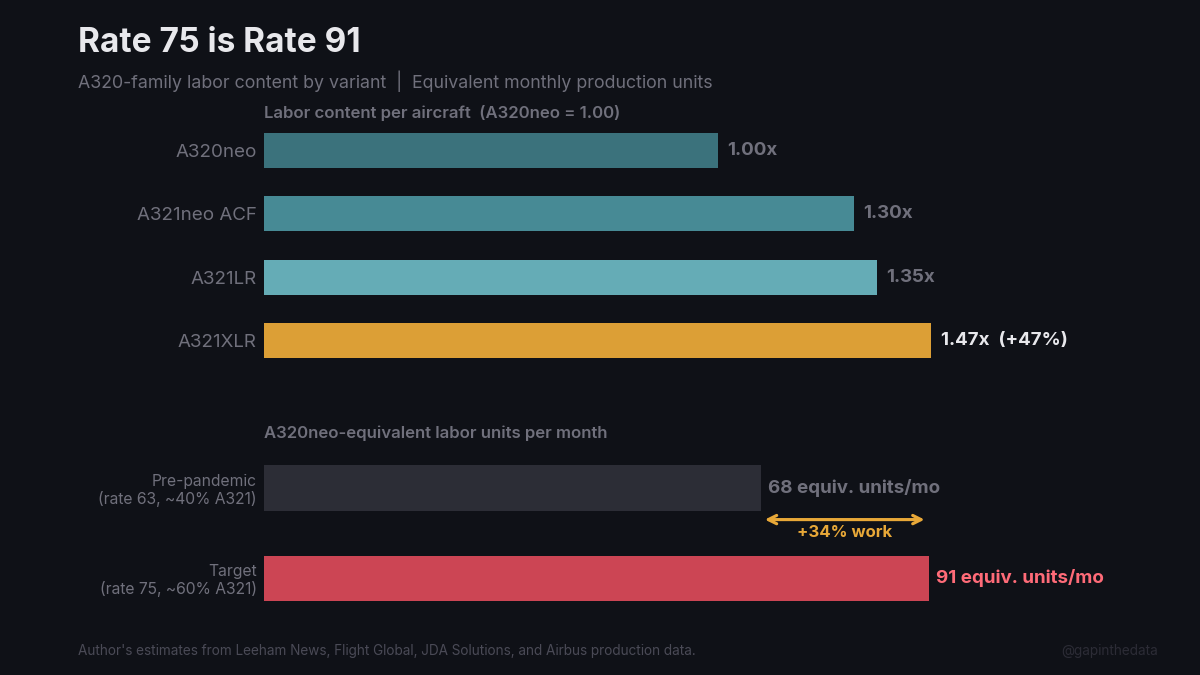

II. What Rate 75 Actually Means

Airbus’s headline target, 75 A320-family aircraft per month by end of 2027, obscures a shift in product mix that has significantly increased per-unit work content.

The A321neo ACF, now the standard production configuration, requires approximately 30% more labor than a base A320neo, what former CFO Harald Wilhelm called a “complex aircraft."12 The A321XLR adds 10–15% on top of that, requiring a dedicated assembly hall in Augsburg for the Rear Centre Tank: 900+ flight test hours, 500+ certification documents.13

| Variant | Labor content (A320neo = 1.00) |

|---|---|

| A320neo | 1.00 |

| A321neo ACF | 1.30 |

| A321LR | ~1.35 |

| A321XLR | 1.43–1.50 |

With 60% of the backlog now A321 variants, rate 75 yields 91 A320neo-equivalent labor units per month.14 Pre-pandemic rate 63 produced 68 equivalent labor units at a ~40% A321 mix, predominantly lower-content A321ceo variants. Airbus is attempting a 34% increase in total work content while marketing it as a 19% increase in unit count.

The XLR’s incremental margin is thinner than it appears. The $16 million list-price premium over a standard A321neo absorbs $8–14 million in additional costs: extra labor ($4.5–6.75M), the Rear Centre Tank system and integration ($2–4M), structural reinforcement ($1–2M), and certification amortisation ($0.5–1M).15 Incremental margin: $2–8 million. At the low end, that barely covers the production disruption. Boeing has no competing product through the rest of the decade, the MAX 10 remains uncertified, with 1,600nm less range, yet Airbus prices the XLR at only $16 million above the standard variant.16

The XLR cannibalises Airbus’s own higher-margin widebody. TAP Air Portugal replaced A330-300 service on Lisbon–Belém with A321LR.17 Air Canada ordered 30 A321XLRs specifically for transatlantic routes that would otherwise require an A330neo.18 Each substitution still results in a sale, but costs Airbus $27 million in revenue and $5–13 million in margin per aircraft.19

Faury has already quietly adjusted the rate target to “70 to 75”; the range is telling.20 Per-aircraft reported EBIT fell 14% in FY2025 despite 27 more deliveries, a consequence of the structural gap between units produced and work performed explored further in Thirty-Three Percent.

III. The Supply Chain That Serves the 6%

A single premium seat requires up to 3,000 parts from 50 suppliers across 15 countries.21 The industry needs 8 million seats over the next decade, a $52 billion pipeline, but supply chain challenges cost airlines $11 billion in 2025 alone, delivery shortfalls total 5,300+ aircraft, and normalisation is unlikely before 2031–2034.22

American Airlines’ first A321XLR was delivered and immediately grounded due to seat shortages.23 United’s A321XLR delivery was delayed more than six months, pushed to summer 2026.24 Lufthansa’s 15 Boeing 787-9s entered service with only 4 of 28 business-class Allegris seats bookable; Collins Aerospace’s seats failed FAA impact testing; full resolution is expected in April 2026.25

Airbus had 60 “gliders” parked in H1 2025, complete airframes missing engines or interiors, tying up €1 billion in inventory and driving free cash flow to negative €1.6 billion.26 Faury described cabin equipment delays as “probably more of a mid-term issue than a short-term one,” with seat and toilet constraints expected to continue into 2027.27

Only 200 engineers worldwide can certify new premium seat designs.28 As airlines demand bespoke cabins, the bottleneck tightens, constraining delivery rates below production rates. AerCap CEO Aengus Kelly: “Stop inventing more seats. Take one that is certified, that’s a very good product, and you’ll get your airplane in the air faster."29 Riyadh Air CEO Tony Douglas: “I want a brand that’s unique and that uniqueness is presented in the cabin."29

Engines were the first constraint on rate 75; the cabin supply chain, with its 200-engineer bottleneck and bespoke certification cycles, may prove harder to solve than the engine duopoly.

IV. The Irreversible Bet

The A321XLR’s Rear Centre Tank is permanently integrated into the fuselage primary structure: structural, load-bearing, not reversible.13 If premium demand drops, no airline needs 4,700nm range on a 155-seat narrowbody. A standard A321neo with 220+ seats and 4,000nm range has far better per-seat economics.

Reconfiguration is physically possible but economically punishing: gutting wiring, seats, and monuments costs hundreds of thousands of dollars and takes weeks to months30, destroying the investment thesis of an aircraft designed around premium yields that have been tested for one business cycle phase.

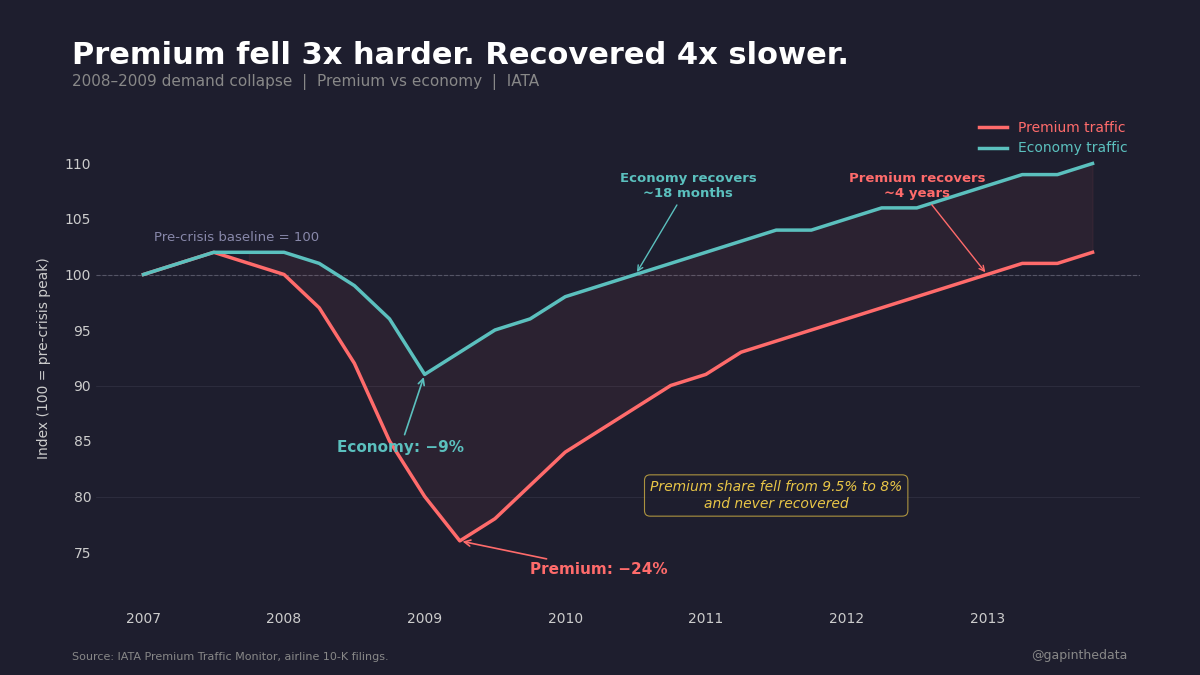

The 2008–2009 precedent is instructive. Premium passengers fell 24% peak-to-trough, while economy fell only 7–9%.31 Premium revenues fell 30% in H1 2009.32 Economy recovered in 18 months; premium took four years. Premium’s share of passengers declined from 9.5% to 8%, permanently.31

The backlog-to-fleet ratio has reached 57%, 17,000 orders against 30,000 active aircraft, up from a historical 30–40%.33 That is the over-ordering pattern that preceded mass cancellations in 2009. Boeing must disclose at-risk orders under ASC 606; Airbus does not make equivalent disclosures.34 The Airbus backlog of 8,754 includes an unknown number of financially fragile customers that Boeing would have already flagged.

Spirit cancelled 52 Airbus orders and forfeited 36 undelivered jets in bankruptcy;35 Frontier cancelled its entire A321XLR order of 18 aircraft and deferred 54 deliveries to 2029–2031;36 JetBlue delayed its A321XLR orders to 2030, and the rejection chain continues.37 CAPA has flagged softening forward bookings on North Atlantic routes for summer 2026, precisely the routes the A321XLR was built to serve.38

The tail risks compound from here. Deloitte found the share of high-income travelers ($200K+) with negative financial sentiment jumped to 15% from 9% in one year.39 J.P. Morgan: “little precedent for how the post-pandemic premium travel customer may react” in a downturn.40

The backlog’s structural fragility compounds with the A350’s Rolls-Royce dependency, which concentrates premium widebody demand on a single engine source: the same margin trap playing out at a different scale.

V. The Winners They Don’t Name

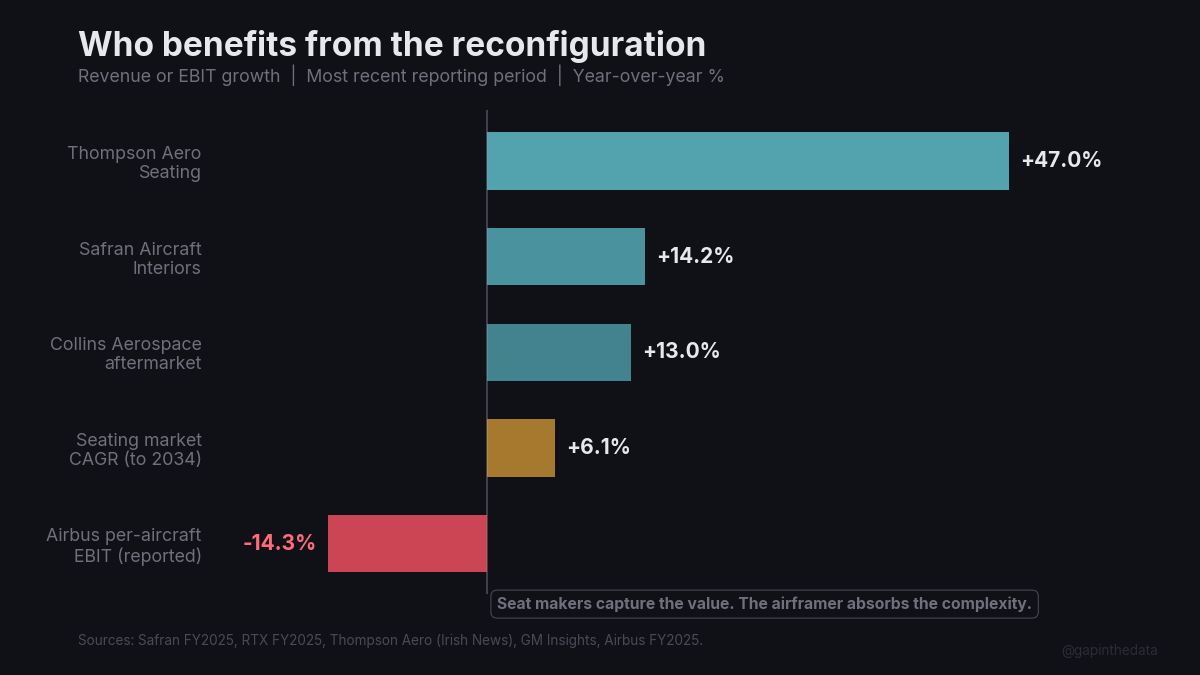

Premiumisation is restructuring the supply chain, but the value accrues to seat makers, not airframers.

Safran’s Aircraft Interiors division grew revenue 14.2% in 2025, with business-class seat deliveries up 65% year-over-year in the first half.41 Thompson Aero Seating reported revenue of GBP 118 million, up 47% from a smaller base, with an order book of approximately GBP 1 billion.42 Collins Aerospace’s commercial aftermarket grew 13% in Q4 2025.43 The global aircraft seating market is projected to grow from $8.7 billion in 2025 to $14.9 billion by 2034, a 6.1% CAGR.44

The mega-contracts tell the story. Emirates awarded Safran $1.2 billion for A350 and 777X seats. Air India awarded Safran $1.2 billion for seats, galleys, and lighting across its fleet renewal. Singapore Airlines committed $835 million to A350 retrofits.45 These are contracts paid on the seat maker’s schedule, not the airframer’s. When an Airbus glider sits waiting for engines, Safran Seats still books revenue on the interiors it has already delivered to the completion center.

The metrics are not like-for-like, Thompson’s 47% growth is from a GBP 80 million base; Airbus’s -14.3% per-aircraft EBIT decline reflects Spirit integration charges on €52.6 billion in revenue46, but the pattern holds: seat makers capture the margin while the airframer absorbs the complexity, the working capital, the glider inventory, and the delivery risk.

The premium cabin supply chain, Safran, Collins, Thompson, Recaro, Panasonic, Thales, and the 200 engineers worldwide who can certify new seat designs, constitutes a Western moat that may run deeper than the engine duopoly constraining COMAC: COMAC’s C919 uses basic Chinese-manufactured seats and has no path to the decades of testing data and bespoke airline relationships that premium cabins require. Engines can be commoditised; the cabin cannot.

Footnotes

1 IATA premium traffic data and airline earnings disclosures. Premium cabins (first, business, and premium economy) account for approximately 6% of global seat capacity but generate roughly 30% of total passenger revenue. CNBC, January 2, 2026, citing industry data. Bloomberg Intelligence reported business and first class load factors exceeded 90% for 14 consecutive months through October 2025.

2 Moody’s Analytics, reported by CNBC, Q2 2025. Top 10% of U.S. households accounted for nearly 50% of all consumer spending.

3 Delta Air Lines Q3 2025 earnings. Premium cabin revenue surpassed main cabin revenue for the first time, reported by Fortune, October 9, 2025. Originally targeted for 2027.

4 Delta Air Lines FY2025 results and Q4 2025 earnings call. CEO Ed Bastian: “The strength in the consumer sector is at the higher end of the curve. The lower-end consumer is struggling greatly.” Premium revenue +7% to $22.1B; main cabin revenue -5% to $23.4B. Reported by Fortune, January 13, 2026.

5 American Airlines A321XLR configuration: 20 Flagship Suite lie-flat seats, 12 premium economy, 123 main cabin = 155 total. A standard economy-dense A321neo typically seats 220+. Aviation Today, February 5, 2026.

6 United Airlines Q4 2025 earnings. “An 80% full premium plane is more profitable than a 100% full economy plane.” Market Minute, January 23, 2026.

7 Southwest Airlines ended 50-year open seating policy, added extra-legroom premium seats, and began charging for checked bags. Stock surged 17% on the announcement. Market Minute, January 29, 2026.

8 Spirit Airlines second bankruptcy filing, February 2026. Fleet shrinking from 214 to approximately 94 aircraft. 1,800 flight attendants furloughed. Pivoting to premium seats. CNBC, February 24, 2026.

9 Frontier Airlines Q3 2025 loss of $76 million. Debuting “First Class” in 2026. Market Minute, January 23, 2026.

10 JetBlue launching domestic business class mid-2026. Airline Geeks, “JetBlue to debut business class on domestic routes,” 2025.

11 Robert Mann, aviation consultant, quoted by CNBC, January 2, 2026: “the airline version of the K-shaped economy: monetize the top of the K and minimize the shortfall at the bottom.”

12 Leeham News, “A321neo configurations and A320 production,” January 18, 2015. The A321neo ACF (Airbus Cabin Flex) requires approximately 30% more work content than a standard A320neo due to larger fuselage sections, additional structural reinforcement, and more complex systems integration. Flight Global, “Airbus battles A321neo complexity and automation hit”: former CFO Harald Wilhelm described the A321neo ACF as a “complex aircraft” requiring heightened customisation levels. Simple Flying, “How much does the Airbus A321XLR cost?”: the A321XLR adds 10–15% labor content above the ACF baseline due to the Rear Centre Tank integration, structural reinforcement, and additional certification requirements.

13 JDA Solutions, “What EASA’s Airbus A321XLR’s Rear Central Tank tale tells about the TC process.” The RCT required 900+ flight test hours and 500+ certification documents. The tank is permanently integrated into the fuselage primary structure: structural, load-bearing, and not removable.

14 Author’s calculation. At approximately 60% A321 variants (blending ACF at 1.30, LR at ~1.35, and XLR at ~1.47) and 40% A320neo (1.00), the blended fleet labor content is approximately 1.21× per unit. Rate 75 × 1.21 ≈ 91 A320neo-equivalent labor units per month. Pre-pandemic rate 63 at ~40% A321 mix, predominantly A321ceo variants, with lower labor content (~1.20) than the current ACF standard, yielded approximately 68 equivalent units (63 × 1.08). The 34% work increase (68 → 91) is marketed as a 19% unit increase (63 → 75).

15 Author’s estimates from industry data. A321XLR list price ~$80M vs A321neo ~$64M = $16M premium. Incremental costs: extra labor $4.5–6.75M, RCT system and integration $2–4M, structural reinforcement $1–2M, certification amortisation $0.5–1M. Total incremental cost: $8–14M. Incremental margin: $2–8M.

16 Simple Flying, “Will Boeing ever build a true Airbus A321XLR competitor?” The A321XLR has no competitor through the rest of the decade. The Boeing 737 MAX 10 remains uncertified and has a range of approximately 3,100nm vs the XLR’s 4,700nm. Cirium reports Airbus is seeking price hikes, but the question remains whether they are fully exploiting their monopoly position.

17 Simple Flying, “TAP Air Portugal loves the Airbus A321LR.” TAP replaced A330-300 service on Lisbon–Belém and expanded A321LR service to Newark, Boston, and Dulles routes previously served by widebodies. TAP head of strategy: the LR gives “nearly the same economics as a widebody.”

18 Skies Magazine, “Airbus A321XLR: An exclusive look at Air Canada’s new narrowbody game-changer.” Air Canada ordered 30 A321XLRs specifically for transatlantic routes that would otherwise require an A330neo.

19 Author’s estimate. A330neo market price $107M vs A321XLR $14–22M).$80M = $27M revenue loss per substitution. Estimated margin loss $5–13M based on A330neo margin of 20–25% ($22–27M) vs A321XLR margin of 18–28% (

20 Airbus SE press release, Production Ramp-Up Targets, February 2026. A320 Family: “70–75 aircraft/month” by “End of 2027, stabilising at 75 thereafter.” See also Thirty-Three Percent, footnote 24.

21 AJOT, “Inside the airline seat industry crisis delaying jet deliveries.” A single luxury premium seat requires up to 3,000 parts from approximately 50 suppliers in approximately 15 countries.

22 Industry estimates compiled from GM Insights, IATA, Acumen Aero, and seat manufacturer disclosures. The industry needs 8+ million seats over the next decade, representing a $52 billion pipeline. IATA (December 9, 2025): supply chain challenges cost airlines more than $11 billion in 2025. Acumen Aero, “Global aviation supply chain 2025”: delivery shortfalls total at least 5,300 aircraft, with normalisation unlikely before 2031–2034.

23 Simple Flying, “American Airlines’ first A321XLR already grounded.” The aircraft was delivered but immediately grounded due to premium seat shortages.

24 ePlane, “United Airlines’ first Airbus A321XLR delivery delayed again.” Delivery delayed 6+ months, pushed to summer 2026.

25 Simple Flying, “Why Lufthansa still can’t sell every seat on Boeing 787 Dreamliners.” Lufthansa’s 15 Boeing 787-9s delayed for months because Collins Aerospace’s Allegris business-class seats failed FAA impact testing. Only 4 of 28 business-class seats could be sold when aircraft entered service (October 2025). Full resolution scheduled for April 15, 2026: 25 of 28 seats bookable. Guru Focus, “Lufthansa restores 25 of 28 787 business-class seats.”

26 AirInsight, “Airbus gliders limit H1 2025 performance.” Approximately 60 gliders parked, causing roughly €1 billion in excess inventory and negative €1.6 billion free cash flow in H1 2025. Airbus recognises revenue at delivery, not production.

27 Airbus FY2025 press release and press conference, February 19, 2026. Faury described cabin equipment delays as “probably more of a mid-term issue than a short-term one,” with constraints expected to continue “into 2026 for engines and 2027 for seats and toilets.”

28 Industry estimates. Approximately 200 seat certification engineers exist worldwide. The premium cabin supply chain is overwhelmingly Western: Safran, Collins, Thompson, Recaro, Panasonic, Thales. COMAC’s C919 uses basic Chinese-manufactured seats; its localisation strategy moves it away from these suppliers. Cirium, “Can COMAC truly challenge the Airbus-Boeing duopoly?”

29 AJOT, “Inside the airline seat industry crisis delaying jet deliveries.” AerCap CEO Aengus Kelly: “Stop inventing more seats. Take one that is certified, that’s a very good product, and you’ll get your airplane in the air faster.” Riyadh Air CEO Tony Douglas: “I want a brand that’s unique and that uniqueness is presented in the cabin.”

30 Simple Flying, “Airliner cabin reconfiguration duration guide.” Reconfiguration from premium to economy requires gutting the entire interior, wiring, systems, seats, monuments, costing hundreds of thousands of dollars and taking weeks to months.

31 IATA, “Premium traffic and revenue are back on track.” Premium passengers fell 24% peak-to-trough (May 2009), while economy fell only 7–9%. Economy recovered in 18 months; premium took four years. Premium’s share of passengers permanently declined from approximately 9.5% to 8%.

32 IATA, June 8, 2009. Premium revenues fell 30% in H1 2009.

33 CAPA, “Airbus 2025 deliveries: momentum meets reality as the supply chain bites back.” Current backlog-to-fleet ratio approximately 57% (17,000 orders vs ~30,000 active fleet), up from historical 30–40%.

34 Boeing applies ASC 606 accounting and has flagged 650+ at-risk orders. Airbus, reporting under IFRS, does not apply ASC 606 and is not required to make equivalent at-risk disclosures.

35 ePlane, “Spirit Airlines cancels Airbus order as part of bankruptcy settlement.” Spirit cancelled 52 Airbus orders and forfeited 36 undelivered jets.

36 Simple Flying, “Frontier Airlines cancels Airbus A321XLR order.” Frontier cancelled its entire A321XLR order of 18 aircraft. Lara News: Frontier deferred 54 deliveries from 2025–2028 to 2029–2031.

37 Airline Geeks, August 8, 2024. JetBlue delayed A321XLR orders to 2030.

38 CAPA, Centre for Aviation, 2026 outlook. Summer 2026 forward bookings and fares showing softness on North Atlantic routes.

39 Deloitte, “2026 travel and hospitality industry outlook.” Share of high-income travelers ($200K+) with negative financial sentiment jumped to 15% from 9% in one year.

40 J.P. Morgan, airline outlook. “There is little precedent for how the post-pandemic premium travel customer may react” in a downturn.

41 Safran, “Safran reports excellent financial performance for 2025 and raises its 2028 ambitions,” February 13, 2026. Aircraft Interiors revenue +14.2%. Business-class seat deliveries +65% YoY in H1 2025. Group backlog €87 billion.

42 Irish News, “Thompson Aero Seating confirms £1 billion order book as 2024 sales soar by 47%.” Revenue GBP 118 million (+47% YoY). VantageNOVA lie-flat seat driving growth.

43 RTX, “RTX reports 2025 results and announces 2026 outlook,” January 27, 2026. Collins Aerospace commercial aftermarket +13% in Q4 2025. Group backlog $268 billion.

44 GM Insights, “Aircraft seating market.” Global aircraft seating market $8.7 billion (2025) → $14.9 billion by 2034 (6.1% CAGR).

45 Emirates → Safran: $1.2 billion (A350 + 777X seats). Air India → Safran: $1.2 billion (seats, galleys, lighting for fleet renewal). Singapore Airlines: $835 million A350 retrofit program. Sources: Safran press releases, airline disclosures.

46 Airbus SE FY2025 press release. Commercial Aircraft EBIT Reported: 4,555M / 793 deliveries = 5.74M per aircraft vs 5,133M / 766 = 6.70M per aircraft in FY2024. Decline of 14.3%. FY2025 reported EBIT was depressed by Spirit AeroSystems integration charges (net -188M). See Thirty-Three Percent, footnotes 12 and 15.