The market prices aluminium as a commodity. The physics prices it as a commitment.

On March 3, QatarEnergy halted production at the Ras Laffan industrial complex after Iranian drone strikes destroyed the gas supply infrastructure.1 Norsk Hydro’s Qatalum smelter, a 636,000-tonne-per-year aluminium facility and a 50/50 joint venture with QatarEnergy, initiated a controlled shutdown expected to complete by end of March.2 Hydro issued force majeure to all customers.

This is the first major Middle Eastern aluminium smelter shutdown in history. The region’s advantage has always been cheap, abundant natural gas for captive power generation. That foundation cracked on February 28.

The three chokepoints analysis documented how the Iran war correlates previously independent risks through a single geopolitical transmission mechanism. This note traces a new vector through that mechanism: raw material supply.

I. The physics of a smelter

An aluminium smelter is a continuous electrochemical process running at roughly 960 degrees Celsius. The electrolysis cells, called pots, contain molten cryolite electrolyte with a superheat margin of 5 to 10 degrees above the liquidus temperature. They are always close to freezing.

Within 30 minutes of losing power or gas, the frozen ledge on the sidewalls begins growing inward. By two to three hours, the bath temperature drops below 900 degrees and large volumes begin solidifying. By four to five hours, the cells have frozen completely. The aluminium itself, with a melting point of 660 degrees, solidifies into a mass that must be physically broken out of each cell.3

The cathode linings are the critical component. Carbon blocks saturated with sodium over years of operation become brittle from sodium intercalation. The thermal stress of a cooling cycle cracks them irreversibly. Cracked cathodes cannot be repaired. Relining costs $100,000 to $300,000 per pot. A typical smelter has 300 to 720 pots.4

Qatalum is executing a controlled shutdown: metal and bath siphoned from each cell, anodes raised, cells cooled in sequence. This preserves the cell linings and reduces estimated restart time to four to five months from when gas resumes.5 An uncontrolled freeze creates catastrophic damage with restart timelines of 6 to 12 months and potline replacement costs of roughly $100 million per potline.

Even a controlled shutdown permanently reduces cathode life by 100 to 400 days. Normal cathode lifespan runs 1,700 to 3,000 days.6 Every cathode in the plant takes irreversible damage from the thermal cycle. The damage is invisible on a balance sheet but real in the physics: Qatalum will restart as a less durable plant than it was on February 27.

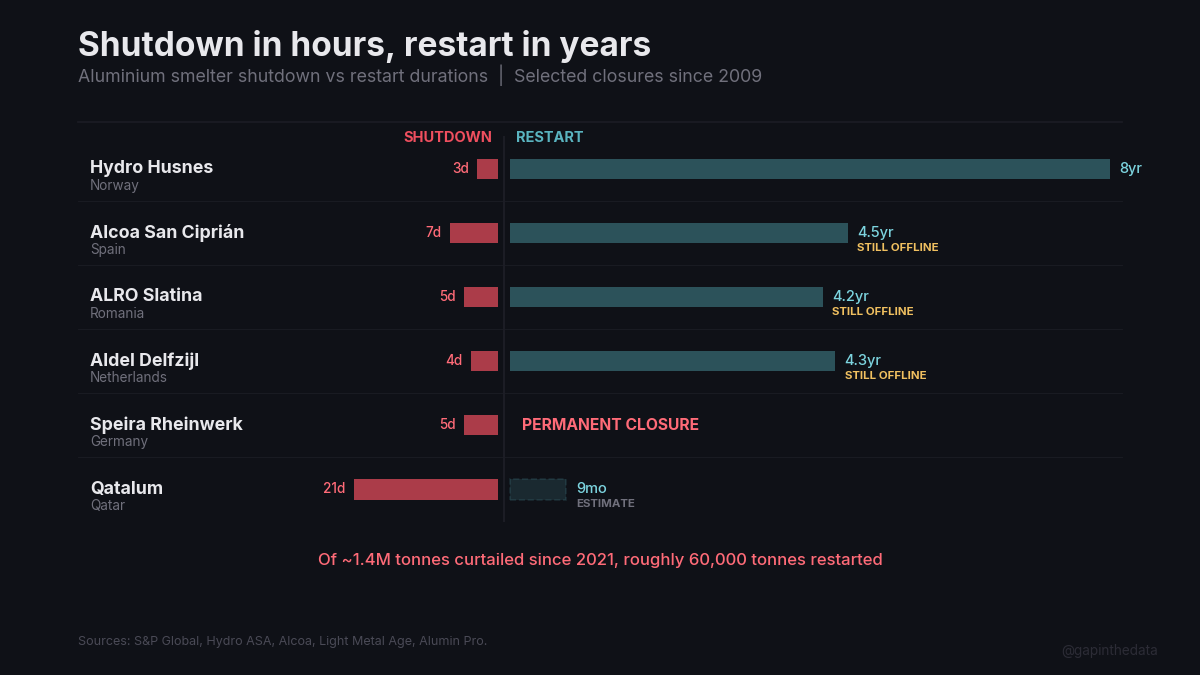

The historical record makes the asymmetry concrete. Hydro’s own Husnes smelter in Norway cut production 50% in 2009. The restart took eight years and NOK 1.3 billion.7 Alcoa’s San Ciprian smelter in Spain shut in December 2021; restart is projected for mid-2026, at total downtime of 4.5 years and losses of $90 to $110 million from delays alone.8 Speira Rheinwerk in Germany closed after 62 years and converted to recycling. Aldel in the Netherlands, ALRO Slatina in Romania, Uniprom in Montenegro, Talum in Slovenia: all closed between 2021 and 2023, all still offline.9

Of roughly 1.4 million tonnes curtailed in Europe since 2021, approximately 60,000 tonnes have fully restarted.10

Shutdown takes days. Restart takes quarters to years. Most never come back.

II. What went offline

The Gulf Cooperation Council operates approximately 5.9 million tonnes per year of aluminium smelting capacity, roughly 8% of global production and 20% of production outside China.11 Virtually all of it exports through the Strait of Hormuz.

Qatalum’s 636,000 tonnes are entering controlled shutdown. Alba, Bahrain’s 1.6 million tonne smelter and one of the world’s largest single-site facilities, declared force majeure on March 1, though the limitation is shipping access, not production damage.12 The smelter is physically intact despite Bahrain receiving 73 missiles and 91 drones. Mina Salman Port was hit; one worker was killed.

Emirates Global Aluminium is the largest single domino. EGA operates 2.5 million tonnes per year across Jebel Ali and Al Taweelah, the latter being the world’s largest single-site smelter at 1.3 million tonnes.13 Two vulnerabilities compound:

The Al Taweelah smelter sits at the terminus of the Dolphin Pipeline, which delivers 2 billion standard cubic feet per day from Qatar’s North Field at Ras Laffan.14 That is the same facility hit by Iranian drones. If Dolphin flow is interrupted, Al Taweelah faces a direct gas supply threat. ADNOC’s domestic sour gas could partially compensate but has historically been insufficient for total UAE demand.

EGA’s Al Taweelah alumina refinery covers only 49% of the smelter’s alumina needs. The remaining 51% is imported through the Strait of Hormuz.15 Kpler analysis shows 61,000 tonnes of alumina bound for GCC smelters currently in the Gulf, with 57,000 additional tonnes destined for Oman. At consumption rates, that is weeks of supply.

EGA secured $5 billion in debt financing on February 27, one day before the strikes.16 EGA has acknowledged export delays and said it may draw on stockpiles outside the region. No formal force majeure yet.

Ma’aden in Saudi Arabia (740,000 tonnes per year) and Sohar Aluminium in Oman (395,000 tonnes) are domestically fuelled but export-dependent on the Strait.17 If Hormuz remains contested, their metal cannot reach customers.

The blast radius is expanding: from one confirmed shutdown, to one force majeure, to three facilities where production or export is at risk. The combined capacity at stake is 5.9 million tonnes per year.

III. The ledger before the war

Qatalum did not go offline in a balanced market.

Pre-conflict consensus estimates for the 2026 aluminium supply deficit ranged from 365,000 tonnes (Reuters poll) to 400,000 tonnes (ING) to 600,000 tonnes (J.P. Morgan).18 The structural constraints that produced those estimates were already binding.

China operates at over 90% utilization against a self-imposed 45 million tonne capacity cap. No net new smelter capacity is being added.19 In December 2024, China cancelled its 13% export tax rebate on aluminium products, reducing Chinese export volumes by roughly 40% month-over-month.20 The policy was strategic: keep metal domestic and strengthen bargaining position against Trump-era tariffs. The effect was to remove Chinese surplus from global markets at exactly the wrong moment.

European primary aluminium capacity has fallen 40% since 2008, from roughly 4.8 million tonnes to 2.9 million tonnes.21 The US trajectory is worse: from 30% of global production in 1980 to approximately 1% today.22 European rollers that machine aerospace-grade plate, including Constellium and Novelis at Koblenz, increasingly depend on imported primary metal from the Middle East and Canada.

LME registered inventory stood at roughly 1.1 million tonnes before the strikes, representing 13 to 14 days of global consumption.23 US LME warehouses hit zero aluminium remaining after the last 125 tonnes were withdrawn in October 2025.24

The price response was immediate. LME aluminium moved from $2,750 to $2,850 per tonne in late February to $3,315 per tonne on March 3, a 3.8% single-day surge to a four-year high.25 European premiums reached $378 per tonne for March and $428 per tonne for April, both 3.5-year highs.26 Goldman Sachs modelled $3,600 per tonne if Middle East production halts for one month.27

Three major “green” P1020 aluminium sources face independent production uncertainties for 2026: Iceland’s Nordural cut output by two-thirds due to electrical equipment failure, and both Canadian and Mozambican output face constraints.28 The green aluminium premium, already elevated, has nowhere to find replacement supply.

The market entered this crisis with 13 days of inventory, a 400,000 to 600,000 tonne structural deficit, a production cap in China, a 40% capacity decline in Europe, and zero aluminium remaining in US warehouses. Then 636,000 tonnes of annual capacity entered shutdown and 1.6 million tonnes declared force majeure.

IV. Thirty-one tonnes

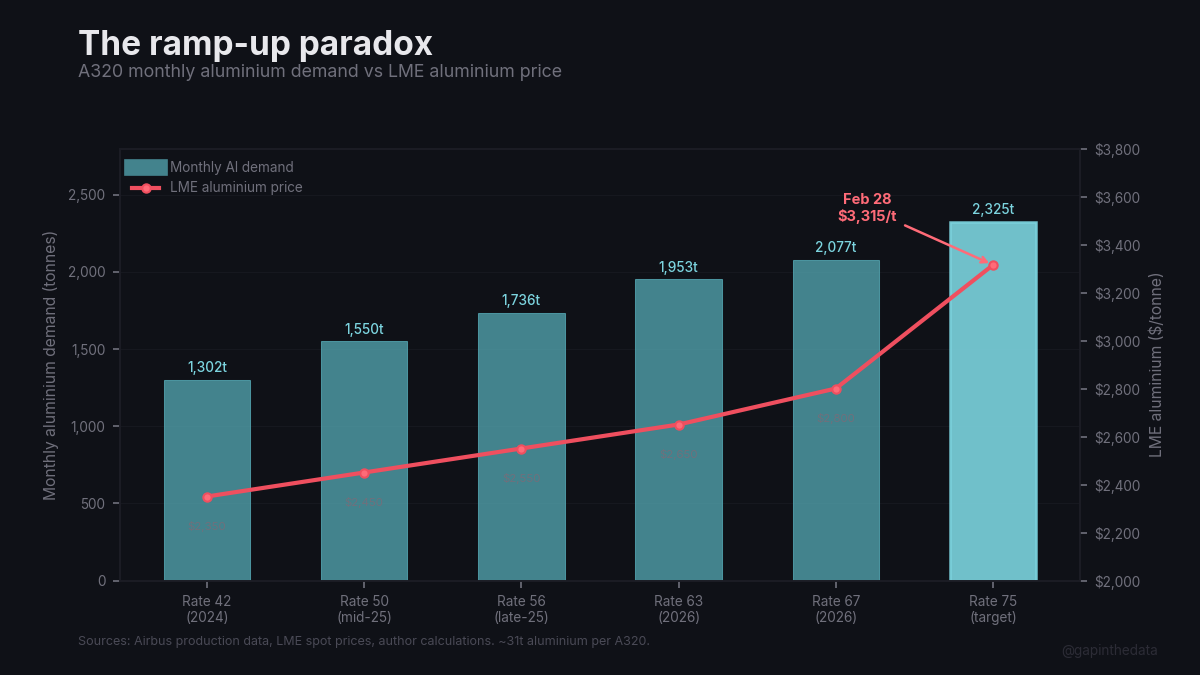

An A320 airframe is 75 to 80% aluminium by weight. At roughly 42 to 44 tonnes operating empty weight, each aircraft requires 31 to 33 tonnes of aluminium alloy.29

At the current production rate of approximately 50 per month, the A320 programme consumes roughly 1,550 tonnes of aluminium monthly. At the rate 75 target, that figure rises to 2,300 to 2,500 tonnes per month.30 The ramp from 50 to 75 requires 50% more metal each month, sourced from a market that just lost 8% of supply.

Airbus’s supply contracts with Constellium, Arconic, Novelis, and Kaiser Aluminum are structured as LME base price plus regional premium plus conversion premium, on multi-year terms.31 The conversion premium, the rolling mill’s margin, is relatively stable. The LME and regional premium components are variable. LME has moved 20% in days. European premiums are at 3.5-year highs.

Existing contracts provide volume security but not full price insulation. Contract renewals will reflect the new baseline. Spot purchases for incremental ramp-up volumes, the marginal tonnes needed to go from rate 50 to rate 75, will price at current market rates.32

The paradox: Airbus needs more aluminium precisely when aluminium is getting more expensive. The marginal cost of the marginal aircraft increases at exactly the production rates the 870 delivery target requires.

The aerospace plate market is a tight oligopoly. Constellium (Issoire, Ravenswood), Arconic (multiple US and EU facilities), Novelis (Koblenz), and Kaiser Aluminum (Trentwood) are the four qualified suppliers.33 Qualification cycles for new alloys or new suppliers run two to five years. These rollers are not smelters. They buy P1020 ingot and process it into aerospace-grade 2xxx-series alloys for fuselage skins and 7xxx-series alloys for wing structures. Their input cost is whatever the LME and the regional premium market say it is.

Boeing’s exposure runs parallel. The 737 MAX is 75 to 80% aluminium at roughly 45 tonnes operating empty weight, requiring 34 to 36 tonnes per aircraft.34 At 30 to 38 per month, that is 1,000 to 1,400 tonnes monthly. Composite-intensive programmes (A350, 787, A220) are relatively insulated. The A320 and 737 are not.

The 2018 Rusal sanctions caused aluminium prices to spike 30% in days.35 The 2022 European energy crisis drove European smelter closures and sustained premium elevation for over 18 months. Both were smaller disruptions than an 8%-of-global-supply threat from a region at war.

V. Where the buffer is not

The standard rebuttal is that aerospace consumes only 0.5 to 0.6% of global aluminium, roughly 417,000 tonnes in 2020 out of 70 to 80 million.36 The framing suggests aerospace is too small to be affected by a commodity disruption.

The framing is wrong. Aerospace does not buy aluminium. It buys qualified alloys from qualified mills on multi-year contracts with two-to-five-year qualification cycles. The market that matters is not the 80-million-tonne global aluminium market. It is the market for aerospace-grade 2xxx and 7xxx plate from four rollers, at least two of which source significant primary metal from the Middle East.37

Constellium’s European operations and Novelis at Koblenz source an estimated 30% of their primary aluminium from GCC smelters.38 If those flows are disrupted, the rollers face input cost spikes on existing contracts and potential volume constraints on incremental orders. They will pass the cost through. They have no choice: rolling margins are thin, and the LME price is the LME price.

The supply chain from smelter to airframe has four stages: primary smelting to P1020 ingot, rolling and processing to aerospace-grade plate, machining and forming to structural parts, and final assembly.39 Each stage has its own lead times, its own qualifications, and its own bottleneck potential. The constraint documented in What Safran Can’t Fix lives at stage zero: engines that do not arrive. The constraint documented in this note lives one stage earlier: raw material that has not been smelted.

Each layer of constraint is upstream of the last. Engines constrain final assembly. Fuselage panels constrain structural integration. Aluminium alloy constrains the panels themselves. The margin trap documents how each programme’s unit economics are already stretched. An input cost increase on the highest-volume programme at the highest-volume production rate compounds that pressure directly.

New smelter construction takes five to six years and costs $5,300 to $8,000 per tonne of annual capacity in Western countries.40 A replacement for Qatalum’s 636,000 tonnes would cost $3.4 to $5.1 billion and begin producing metal in 2031 at the earliest. Data centres now bid $115 per megawatt-hour for power; smelters need $40 per megawatt-hour on 10 to 20 year contracts.41 The competition for cheap electricity, which is the competition for aluminium smelting, is a contest the smelters are losing.

The 2026 guidance assumes 870 deliveries.42 Rate 75 on the A320, the path to that target, requires 2,300 to 2,500 tonnes of aluminium per month from an alloy market fed by smelters whose power comes from gas whose pipeline originates at a facility that was struck by Iranian drones four days ago.

The metal that becomes the fuselage panels on an aircraft delivered in Q4 2026 has to enter the rolling mill months before delivery. The ingot that feeds the rolling mill has to come from a smelter that is currently operational. Qatalum is not. Alba cannot ship. EGA’s gas supply runs through a pipeline from a destroyed facility, and its alumina arrives through a contested strait.

The market prices aluminium as a commodity. The physics prices it as a commitment. Commitments, once broken, do not restart on the same timeline they were built.

Footnotes

1 Bloomberg, “QatarEnergy Stops Output of Some Chemicals, Metal After LNG Halt,” March 3, 2026. Ras Laffan industrial complex halted after Iranian strikes destroyed gas supply infrastructure.

2 Hydro ASA, press release, March 3, 2026. Qatalum controlled shutdown initiated; force majeure declared to all customers. Capacity: 636,000 tonnes per year.

3 Tabereaux, “Survivability of Aluminum Potlines After Lengthy Electrical Power Outages,” Springer. Damage timeline from 30-minute manageable window to complete cell freeze at 4 to 5 hours.

4 Tabereaux, “Loss in Cathode Life Resulting from Shutdown and Restart,” Light Metals 2010, ResearchGate. Cathode relining costs $100,000 to $300,000 per pot; typical smelter has 300 to 720 pots.

5 Alumin Pro, “Challenges with Restarting Aluminum Smelters.” Controlled shutdown restart timeline: 4 to 5 months from gas resumption. Uncontrolled freeze: 6 to 12+ months.

6 Tabereaux (2010). Controlled shutdown permanently reduces cathode life by 100 to 400 days against normal lifespan of 1,700 to 3,000 days.

7 Hydro ASA, corporate disclosures. Husnes smelter: 50% production cut in 2009, restart completed 2017. Cost: NOK 1.3 billion (~$150M).

8 Alcoa, San Ciprian disclosures. Shutdown December 2021; restart projected mid-2026. Total downtime: 4.5+ years. Delay losses: $90 to $110 million.

9 S&P Global; Light Metal Age, “European Aluminum Smelters Face Closures.” Speira Rheinwerk (130,000 tpy, closed September 2023, permanent, converting to recycling), Aldel (110,000 tpy, October 2021, offline), ALRO Slatina (283,000 tpy, January 2022, offline), Uniprom (120,000 tpy, 2022, permanent), Talum (84,000 tpy, 2022, ceased).

10 S&P Global; Fastmarkets. Of ~1.4 million tonnes curtailed since 2021, roughly 60,000 tonnes restarted (Aluminium Dunkerque, with French government support).

11 Author calculations from EGA, Alba, Hydro, Ma’aden, and Sohar corporate disclosures. GCC total: ~5.9 million tonnes per year. Global production: ~73 million tonnes. Ex-China: ~29 million tonnes.

12 MINING.COM, “Alba Declares Force Majeure,” March 1, 2026. Shipping blockade, not production damage. Mina Salman Port struck; one worker killed.

13 EGA corporate disclosures. Jebel Ali: ~1.2M tpy. Al Taweelah: ~1.3M tpy. Total: ~2.5M tpy.

14 EGA; Dolphin Energy corporate data. Dolphin Pipeline: 2 billion scf/day from Qatar’s North Field at Ras Laffan to Al Taweelah and onward.

15 EGA; Kpler trade flow analysis. Al Taweelah alumina refinery covers ~49% of smelter needs. 61,000 tonnes alumina in transit to GCC; 57,000 additional tonnes to Oman.

16 EGA, “EGA Secures $5 Billion Financing,” February 27, 2026. One day before Iranian strikes.

17 Ma’aden (vertically integrated with domestic bauxite mine, 740K tpy) and Sohar Aluminium (Oman domestic gas, 395K tpy). Both export through Hormuz.

18 Reuters poll: 365,000t deficit. ING Think, “Aluminium deficit will support prices in 2026”: ~400,000t. J.P. Morgan: 600,000t.

19 China’s 45M tonne self-imposed capacity cap; >90% utilization. No net new smelter capacity additions.

20 China cancelled 13% aluminium product export tax rebate, effective December 2024. Export volumes fell ~40% month-over-month immediately.

21 S&P Global; Light Metal Age. European primary aluminium capacity: ~4.8M tonnes (2008) to ~2.9M tonnes (2025). 40% structural decline.

22 Aluminum Association, “Powering Up American Aluminum,” 2025 white paper. US: 30% of global production (1980) to ~1% (2025).

23 LME data. Registered inventory: ~1.1M tonnes. Global consumption: ~73M tpy / 365 = ~200K t/day. 1.1M / 80K = ~13 to 14 days (adjusting for non-exchange inventory).

24 LME warehouse data. US warehouses: zero aluminium remaining after last 125 tonnes withdrawn, October 2025.

25 LME spot prices. February 27: $2,750 to $2,850/t. March 3: $3,315/t (+3.8% single day; 4-year high).

26 Fastmarkets. European duty-paid premium: $378/t (March), $428/t (April). Both 3.5-year highs. US Midwest premium: record above $1/lb, February 2026.

27 Goldman Sachs, aluminium market note. $3,600/t scenario if Middle East production halts for one month.

28 Fastmarkets, “Green aluminium deficit looms in Europe.” Nordural (Iceland): output cut by two-thirds due to electrical equipment failure. Canadian and Mozambican constraints per S&P Global.

29 Airbus programme specifications. A320 family: ~42 to 44 tonnes OEW, ~75 to 80% aluminium by weight. Per-aircraft aluminium: 31 to 33 tonnes.

30 Author calculation. Rate 50: 50 x 31t = 1,550t/month. Rate 75: 75 x 31t = 2,325t/month (rounded to 2,300 to 2,500t range given 31 to 33t per aircraft).

31 Constellium, 10-year Airbus contract announcement, June 2020. Arconic, ~$1B multi-year Airbus contract, November 2016. Contract structure: LME + regional premium + conversion premium.

32 ING Think, “Middle East conflict tilts aluminium risks further to the upside,” March 2026. Spot pricing for incremental volumes at current market rates.

33 Constellium (Issoire, Ravenswood), Arconic (multiple), Novelis/Koblenz, Kaiser (Trentwood). Qualification cycles: 2 to 5 years for new alloys or suppliers.

34 Boeing 737 MAX specifications. ~45 tonnes OEW, 75 to 80% aluminium, ~34 to 36 tonnes per aircraft. At 30 to 38/month: 1,000 to 1,400t/month.

35 2018 Rusal sanctions: aluminium prices +30% in days. 2022 European energy crisis: sustained premium elevation 18+ months with multiple smelter closures.

36 Aerospace aluminium market: ~417,000 tonnes (2020) of ~70 to 80M tonnes global. Market value: ~$34.7B (2023).

37 Author analysis. Aerospace-grade 2xxx (Al-Cu, fuselage skins) and 7xxx (Al-Zn-Mg, wing skins, spars, beams) alloys require specific qualification from specific mills.

38 Author estimate based on European roller sourcing patterns and GCC export data. Constellium and Novelis European operations: ~30% of primary aluminium from Middle Eastern smelters.

39 Supply chain stages: (1) primary smelting to P1020 ingot, (2) rolling/processing to aerospace plate, (3) machining/forming to parts, (4) final assembly.

40 Aluminum Association (2025). New smelter construction: 5 to 6 years, $5,300 to $8,000 per tonne annual capacity in Western countries.

41 Data centre power bids per industry reporting. Smelters require $40/MWh on 10 to 20 year contracts; data centres bid $115/MWh on shorter terms.

42 Airbus SE, FY2025 results, February 19, 2026. 2026 guidance: ~870 deliveries. Assumes “no additional disruptions to global trade or the world economy, air traffic, the supply chain.”