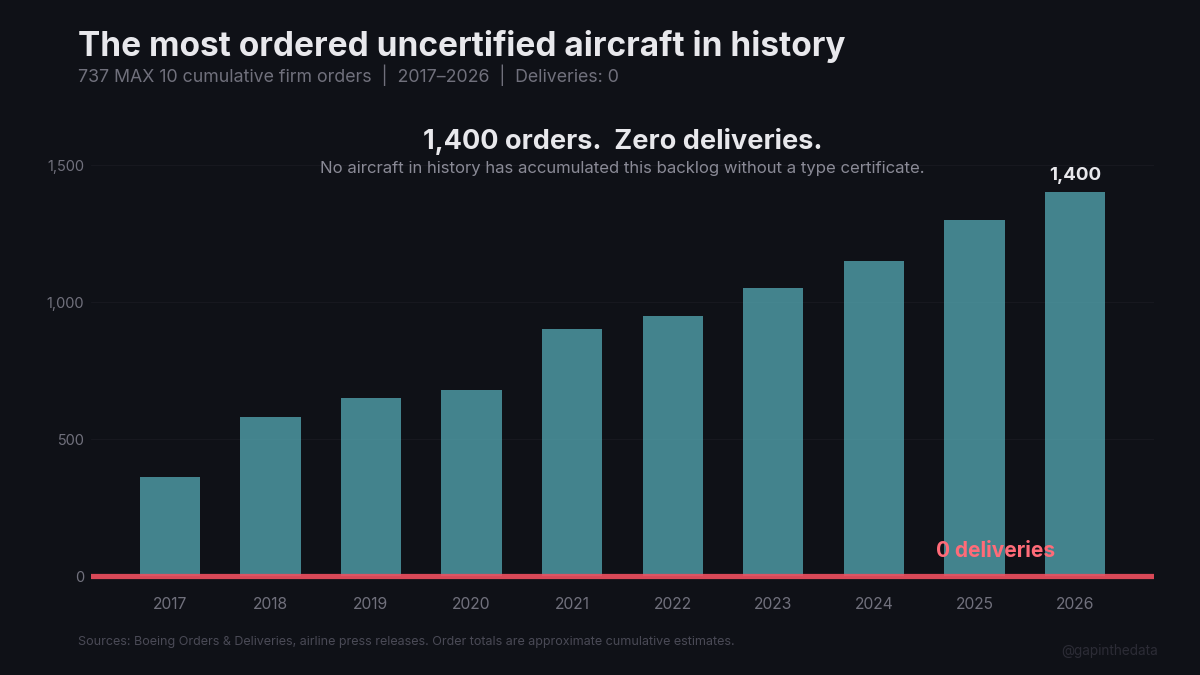

1,400 firm orders. Zero deliveries. The market has priced in a type certificate that does not exist.

No aircraft in commercial aviation history has accumulated this order book without a type certificate. The Boeing 737 MAX 10 has more than 1,400 firm orders from airlines on five continents and has delivered none of them.1 The FAA cleared Boeing for Phase 2 flight testing before Christmas 2025, the first forward movement in more than three years.2 Two problems remain before the FAA can issue the certificate: a nacelle anti-ice redesign that Boeing completed and the FAA has not accepted, and a set of congressionally mandated safety enhancements the FAA began reviewing on December 12.3 Airlines have committed billions on the assumption both will be resolved. The assumption is unverified.

I. What Phase 2 actually means

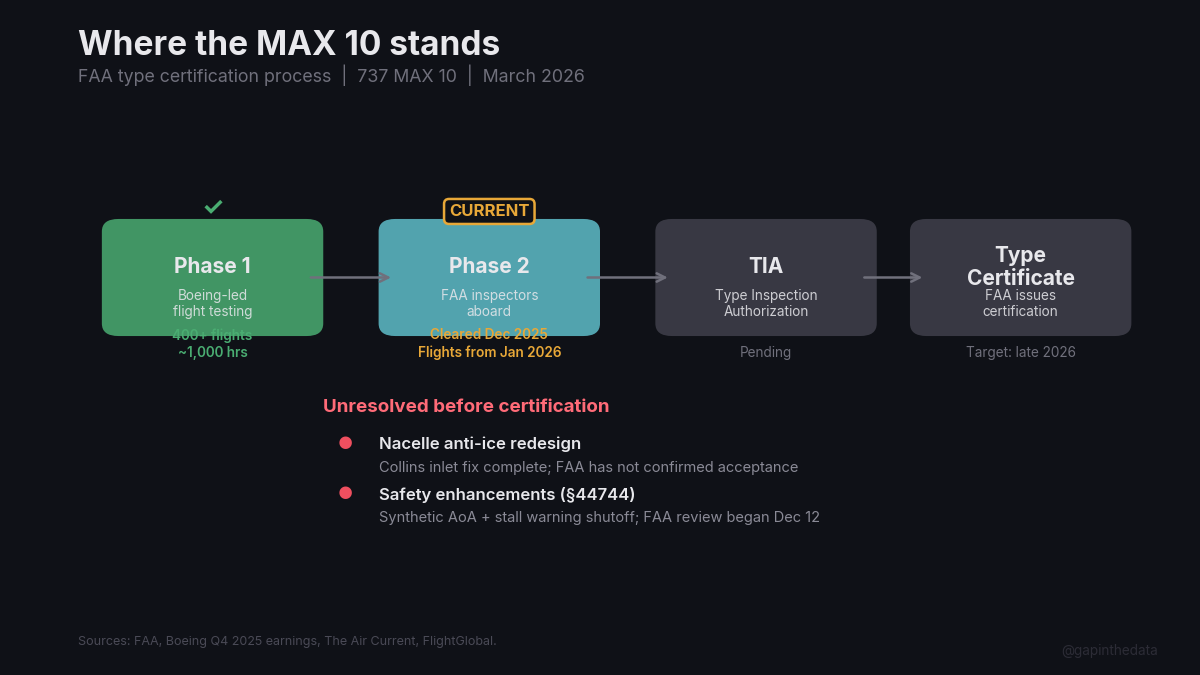

FAA type certification is sequential. Phase 1 is Boeing-led: the manufacturer conducts flight testing and generates compliance data. Boeing completed more than 400 flights and nearly 1,000 hours on three MAX 10 test aircraft during Phase 1.4 Phase 2 puts FAA inspectors aboard. Only flights under FAA oversight accumulate certification credit.5

The FAA cleared Boeing for Phase 2 just before the Christmas 2025 holiday, and Boeing began conducting flights in early January 2026.2 This clearance applies only to the MAX 10; the MAX 7 has not yet received it. The MAX 10 was originally expected in 2020. The cumulative delays, driven by the MCAS redesign, the production cap following the door plug incident, the machinist strike, and the nacelle redesign, span six years.6

Two issues remain.

The nacelle inlet’s carbon-composite inner barrel, built by Collins Aerospace, overheats when the anti-ice system pumps hot bleed air through it in dry conditions for more than five minutes. Temperatures exceed the composite’s design limits, causing thermal degradation. The FAA’s concern: inlet failure could cause the engine inlet or fan cowl to separate from the aircraft.7 Boeing requested an exemption from certification rules in November 2023, withdrew it under congressional pressure in January 2024, pursued a redesign, scrapped that redesign in mid-2025, and completed a second redesign after more than 3,000 hours of lab testing.8 Ortberg on the Q4 2025 call: Boeing is “following the lead of the FAA as we work to certify the suite of design changes."9 The FAA has not publicly confirmed acceptance.

The second issue is statutory. The 2020 Aircraft Certification Reform Act required modernized crew alerting on new type certificates, a direct response to the MCAS failures. Boeing could not meet the deadline. Congress then passed an amendment (codified at 49 USC §44744) that exempted the MAX 7 and MAX 10 from the full crew alerting requirement but imposed two specific safety enhancements: a synthetic angle-of-attack system providing computed redundancy beyond the two physical sensors, and a means for pilots to shut off erroneous stall warnings.10 The statute then starts a clock: within one year of the MAX 10 type certificate, all new MAX production must include these enhancements; within three years, every MAX in service must be retrofitted at Boeing’s expense.11 The FAA published its implementation plan on December 15, 2025.12

The fraud claims that SWAPA brought against Boeing exist because Boeing told pilot unions “same plane, no retraining” while concealing MCAS. The safety enhancement mandate exists because Congress agreed the problem was real. The MAX 10 is the first aircraft that must pass through a certification regime redesigned in response to that failure.

Phase 2 means the FAA is actively testing, not waiting. The nacelle and the safety enhancements are specific, bounded problems with defined endpoints. They are not the open-ended cultural reckoning that followed the crashes.

II. Who bet what

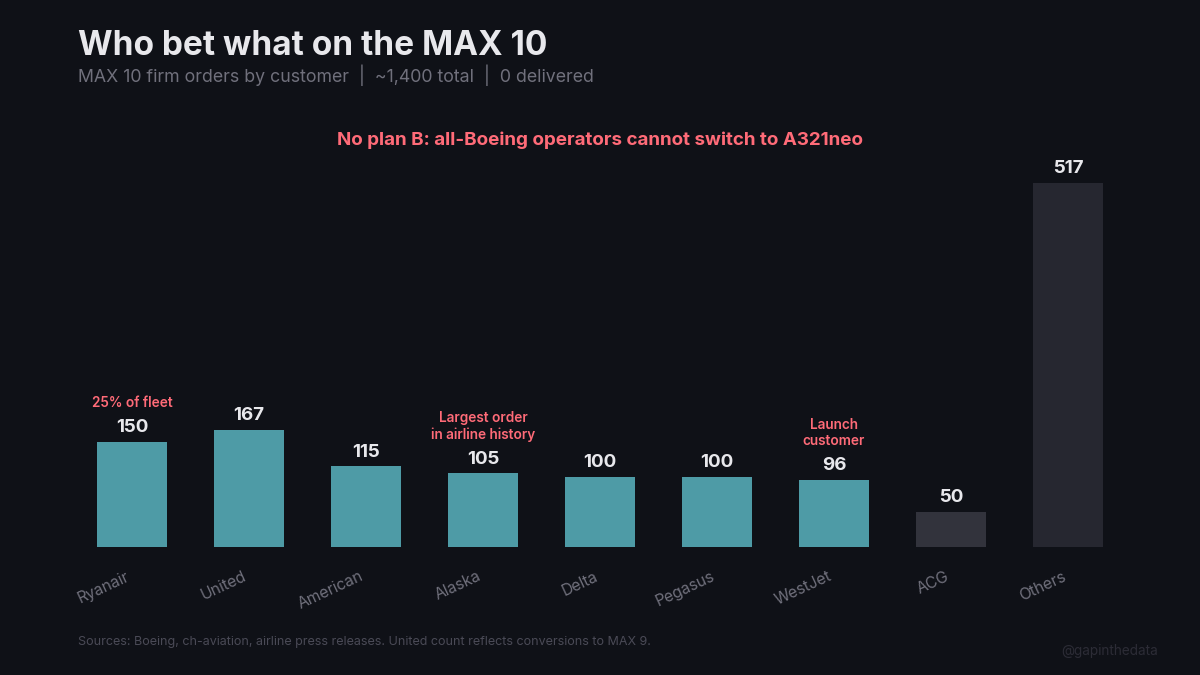

Boeing does not publicly break out sub-variant orders. The figures below are from press releases, Cirium, and ch-aviation.1

Ryanair holds 150 firm orders plus 150 options, announced May 2023. All-Boeing fleet of 611 aircraft. O’Leary says Boeing has provided written guarantees to deliver the first 15 MAX 10s in spring 2027.13 Ryanair will configure them with 228 seats and projects they will lift profit per passenger from approximately €10 toward €12 to €14.14 But 150 aircraft represent 25% of the current fleet, and Ryanair took delivery of its final MAX 8-200 in February 2026.15 The MAX 10 is now its sole outstanding narrowbody order.

American Airlines holds 115 firm orders (85 new, 30 converted from MAX 8) plus 75 options.16 Alaska Airlines holds 105 firm orders plus 35 purchase rights, its largest order ever.17 Alaska’s fleet math: 248 current 737s, growing to 475 by 2030 and 550+ by 2035, with international expansion to London Heathrow, Rome, and Reykjavik launching in May 2026. The MAX 10 provides high-density domestic capacity to fund that expansion with 787s.18

United Airlines holds approximately 167 firm orders, though that number has been falling. United has converted a significant portion to the already-certified MAX 9 due to certification delays. CCO Nocella: “We originally intended to be the first delivery customer for the Max 10. We may not be that, and we are perfectly fine with that."19 Delta holds 100 plus 30 options, its first Boeing narrowbody order in over a decade.20 Pegasus holds 100 plus 100 options. WestJet holds approximately 96 and is the planned launch customer.21 Aviation Capital Group holds 50, the largest lessor commitment, after adding 25 MAX 10s in January 2026.22 Other customers include flydubai, Lion Air, GOL, TUI, Virgin Australia, Air India, and undisclosed buyers.23

Airlines commit to uncertified aircraft because Boeing’s contractual guarantees include delay penalties, because delivery slots are scarce, and because the switching cost to A321neo is prohibitive for all-Boeing operators. Pilot type ratings alone run $18,000 to $35,000 per pilot; a major carrier switching manufacturers faces $150 to $300 million in total transition costs.24 But order fluidity is high. United has already converted MAX 10s to MAX 9s. WestJet swapped 6 for 787-9s. Qatar cancelled 25 entirely.23 The hedge only works if the aircraft eventually certifies.

III. The competitive frame

MAX 10 versus A321neo, the numbers: 230 seats versus 244 (a 14-seat gap), 3,100 nm versus 4,000 nm (a 900 nm gap), and trip cost at near parity per independent analysis.25 Leeham News finds low single-digit differences depending on configuration and engine choice. Boeing claims 5% better; Airbus claims 10% better; the truth is negligible.25

The A321XLR, certified in July 2024 and delivered to Iberia in October, pushes range to 4,700 nm and opens transatlantic routes the MAX 10 cannot serve.26 Any A321neo can become an LR by installing additional center tanks with no structural modification. Leeham’s conclusion: the A321LR and A321XLR, “the two margin-rich variants,” have no Boeing competitor.27 The MAX 10 occupies a narrower niche than the aircraft it was designed to match.

What the MAX 10 can do is exist. The A321neo has over 5,300 aircraft in backlog, 7+ years of production at current rates.28 Airbus controls 82 to 84% of the committed backlog in the 180- to 230-seat category through 2030.29 Since at least 2022, the 200+ seat narrowbody segment has been effectively uncontested. Every Boeing-committed operator in that segment has had no modern replacement. Certification would change that. Whether it changes enough depends on how many of the 1,400 orders survive contact with the timeline.

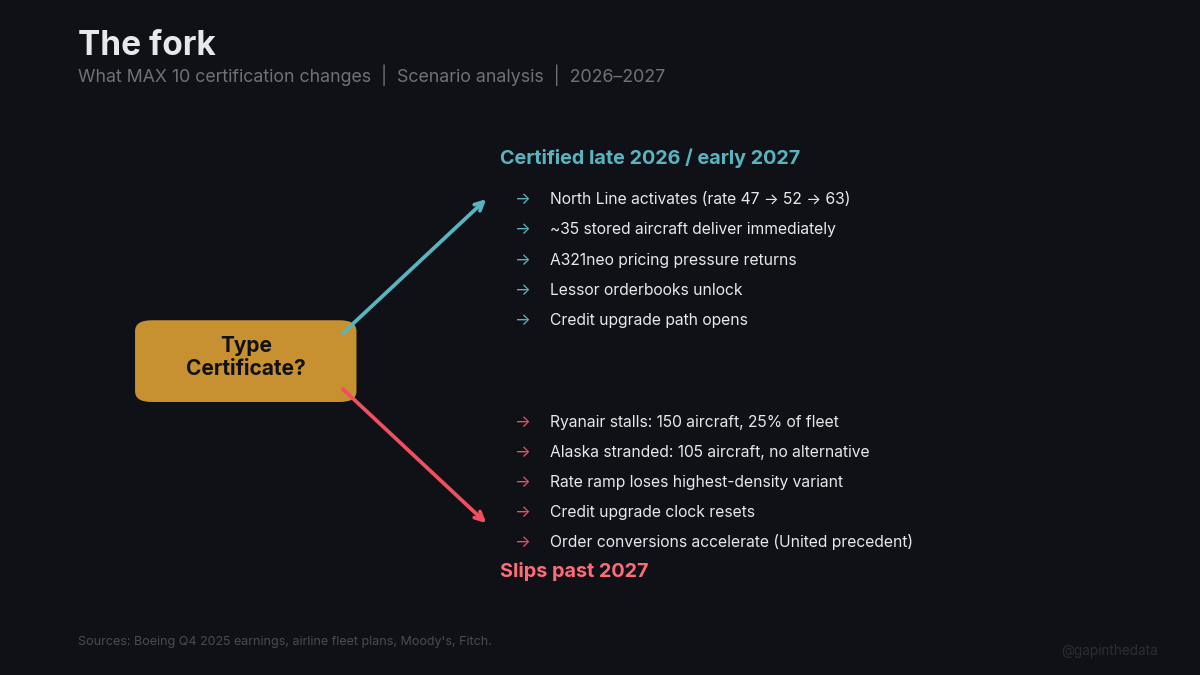

IV. The fork

Ortberg told investors on the Q4 2025 call: “We still anticipate certification for both the 737-7 and 737-10 in 2026."30 CFO Malave was more specific: approximately 30 MAX 10 airframes will be built in 2026 but “will not be delivered in 2026. Be delivered in 2027. Upon certification."31 The FAA has declined to commit to any date.

If certified in late 2026 or early 2027: Boeing’s North Line in Everett, the first single-aisle final assembly line outside the Renton factory, activates. Facility and tooling investments are complete; mid-summer 2026 is the target.32 The three Renton lines handle rate 42 now and will push to 47; the North Line is the capacity mechanism for the path from rate 47 to 52 to 63. Approximately 35 stored MAX 7 and MAX 10 aircraft (roughly 26 to 27 MAX 7s and 4 to 5 MAX 10s) deliver immediately.33 Lessors can market delivery positions. And Airbus’s uncontested pricing power in the 200+ seat segment faces competitive pressure for the first time since 2022.34

If certification slips past 2027: Ryanair’s fleet renewal stalls. Alaska’s growth plan loses its domestic capacity. Boeing’s rate ramp loses its highest-density variant, constraining the path from rate 47 to rate 52. The credit agencies are patient but not indefinitely: Moody’s moved Boeing to stable in December 2025 but said upgrade pressure is unlikely until debt-to-EBITDA approaches 3.0x and free cash flow sustains above $8 billion, conditions it described as “years away."35 Fitch signaled a possible upgrade within 6 to 12 months from its June 2025 revision, a window now more than half elapsed with no action.36 And the precedent United has set, converting MAX 10 orders to MAX 9s, becomes available to every customer in the backlog.

V. The ground truth

Forty-Six to Nineteen showed Boeing executing on deliveries at rate 42, heading to 47. Rate 47 has slipped from 2026 to 2027; the supply chain harmony Ortberg cited on the Q4 call (“Spirit has some work to do”) is a precondition that reintegration has not yet delivered.37 Rate 47 is achievable without the MAX 10 certificate. The North Line and rates above it require it. What Safran Can’t Fix showed five competing claims on every LEAP engine CFM International produces. The MAX 10 uses the LEAP-1B from the same upstream pool. Certification adds another claim on shared capacity, which means tighter allocation for the LEAP-1A that powers the A320neo. And What You Tell Pilot Unions showed how “same plane, no retraining” created legal liability when MCAS was exposed. The congressionally mandated safety enhancements exist because of that history and are now statutory preconditions for the type certificate.

Boeing under Ortberg has made different choices than under Calhoun or Muilenburg. The 787 programme reduced average rework hours by nearly 30% in 2025; 737 travelled work is down approximately 75% since February 2024.38 Spirit reintegrated. All three credit agencies moved to stable in 2025.39 Ortberg in Senate testimony: “I’m not pressuring the team to go fast. I’m pressuring the team to do it right."40 These are Boeing’s self-reported metrics and Boeing’s stated philosophy. Between them and 1,400 unfilled orders sit a nacelle redesign that was scrapped and restarted, safety enhancements Congress mandated and tied to a retrofit clock, six years of missed dates, and a regulatory process redesigned in response to the last time Boeing’s words did not match its engineering. The certificate will say whether they match now.

Footnotes

1 Boeing Orders & Deliveries, March 2026. MAX 10 total firm orders exceed 1,400 per ch-aviation. Boeing does not publicly break out sub-variant totals. Zero deliveries to date. The overall 737 MAX backlog stands at approximately 4,887 unfilled orders across all variants. Per ch-aviation, Forecast International, Simple Flying.

2 The Air Current, January 8, 2026. “Boeing advances 737 Max 10 into next phase of FAA flight testing.” FAA cleared Boeing for Phase 2 (TIA-2) just before Christmas 2025. Phase 2 flights began early January 2026. Clearance applies only to the MAX 10. See also Seattle Times, January 8, 2026.

3 Nacelle anti-ice redesign: Boeing Q3 2025 earnings call (complete); FAA has not publicly confirmed acceptance. Safety enhancements: FAA review began December 12, 2025; Federal Register notice December 15, 2025 (FR Doc 2025-22787). Per Boeing investor relations, Regulations.gov.

4 Boeing completed more than 400 flights and nearly 1,000 flight hours on three MAX 10 test aircraft (N27751, N27752, N27753, all originally built for United Airlines). Per Seattle Times, January 8, 2026, citing Boeing internal communications.

5 FAA Type Certification process. Phase 1: manufacturer-led flight testing. Phase 2: FAA flight test and evaluation (inspectors aboard). Per FAA Order 8110.4C. Boeing refers to Phase 2 as “TIA-2.”

6 Boeing certification timeline. MAX 10 originally expected 2020. MCAS redesign (2019-2020), production quality issues (2021-2023), FAA production cap (January 2024-mid-October 2025), machinist strike (September-November 2024), nacelle anti-ice redesign (scrapped and restarted). Per FlightGlobal, The Air Current. See also Forty-Six to Nineteen, footnote 31.

7 The nacelle inner barrel is built by Collins Aerospace (RTX), not CFM International. GE Aerospace has stressed the issue concerns the inlet, not the LEAP-1B engine. FAA airworthiness directive (mid-2023) limited anti-ice use to five minutes in dry air. Potential consequences include inlet or fan cowl separation, wing/empennage damage, and depressurization risk. Fewer than two dozen inlets on in-service aircraft have shown thermal damage; no structural failures in service. Per FlightGlobal, Aviation Week, FAA.

8 Boeing requested a nacelle exemption November 2023; withdrew January 2024 after opposition from Senator Duckworth. Ortberg, Q2 2025 earnings call: “We found some issues with the design implementation we had, so we’re going to have to back up.” Ortberg, Q3 2025 call: “more than 3,000 hours of lab testing and analysis” supporting “a final set of design changes.” Per CBS News, FlightGlobal, Boeing investor relations.

9 Ortberg, Q4 2025 earnings call, January 27, 2026: Boeing has “a final set of design changes to permanently address the engine NII issues on the 737-7 and 737-10” and is “following the lead of the FAA.” Test aircraft must be modified with newest hardware. Per Motley Fool transcript.

10 Aircraft Certification, Safety, and Accountability Act, P.L. 116-260, Division V, Section 116 (2020): required modernized crew alerting on new type certificates. Deadline: December 2022. Boeing could not meet it. Congress passed P.L. 117-328, Section 501, codified at 49 USC §44744. Safety enhancements: (1) synthetic enhanced AoA system (computed third reference from multiple sensors, addressing the MCAS single-sensor vulnerability); (2) means to shut off erroneous stall warning and overspeed alerts.

11 49 USC §44744 retrofit timelines. One year after MAX 10 type certificate: no new airworthiness certificates for any MAX without enhancements. Three years after: no person may operate any MAX without them. Boeing bears retrofit costs.

12 FAA Federal Register notice, December 15, 2025 (FR Doc 2025-22787, Docket FAA-2025-0799). Four-part implementation plan. FAA review of Boeing’s design began December 12, 2025.

13 Ryanair/Boeing, May 9, 2023. 150 firm + 150 options. Over $40 billion at list prices. Written guarantees for first 15 deliveries spring 2027. CFO Sorahan: Boeing “increasingly confident” about Q3 2026 certification. Per Ryanair corporate, Air Data News.

14 Ryanair FY2025. Net profit €1.6 billion. Net cash approximately €1.2 billion. Fleet: 611 aircraft, all Boeing 737. O’Leary: MAX 10 will lift profit per passenger from ~€10 toward €12-14 (20% more seats, 20% less fuel per flight). Per Ryanair Holdings annual report.

15 Ryanair took delivery of its 209th and final 737 MAX 8-200 in February 2026, completing its Gamechanger order. Per Engine Cowl.

16 American Airlines, March 4, 2024. 85 new MAX orders (including MAX 10), 30 MAX 8 conversions to MAX 10, 75 options. Per Boeing investor relations.

17 Alaska Airlines, January 7, 2026. 105 737-10 firm orders + 35 purchase rights. Total Boeing order book: 245 aircraft. “The largest aircraft order in Alaska Airlines history.” Per Boeing press release, Alaska Airlines newsroom, CNBC, Aviation Week.

18 Alaska fleet plan. Current: 248 737s (413 total across Alaska Air Group). Target: 475+ by 2030, 550+ by 2035. International: London Heathrow, Rome, Reykjavik from Seattle, May 2026. Hawaiian integration ongoing. Per Alaska investor day January 2026, SEC filings.

19 United: originally 100 MAX 10s (2017 Paris Air Show) + 150 additional (June 2021 “United Next”). Current count ~167 per Cirium (mid-2025), reflecting conversions to MAX 9. Nocella: first deliveries expected 2027 or 2028. Per FlightGlobal, AirlineGeeks.

20 Delta, Farnborough 2022. 100 firm + 30 options. First Boeing narrowbody order in over a decade. Per Boeing investor relations.

21 Pegasus, December 19, 2024: 100 firm + 100 options, deliveries from 2028. WestJet: ~96 firm (originally 102, minus 6 converted to 787-9s February 2026) + 25 options. WestJet planned as launch customer. Per Boeing, Simple Flying.

22 Aviation Capital Group, January 13, 2026. 50 additional MAX (25 MAX 8 + 25 MAX 10), bringing MAX 10 total to 50 firm. Total MAX book: 121 aircraft. Largest lessor MAX 10 customer. Per Boeing press release, FlightGlobal.

23 Other customers include: flydubai (~50+), Lion Air (~50), GOL (25), TUI (24), Virgin Australia (22), Air India (10, confirmed Wings India January 29, 2026), Copa (9). Qatar cancelled 25. flydubai has also ordered 150 A321neos as hedge. Per Boeing, airline press releases.

24 Switching costs. Full cross-manufacturer type rating: $18,000-$35,000+ per pilot. Maintenance certifications, parallel spare parts, new simulators. Estimated total: $150-$300M+ for a major carrier over 6-10 years. Per AeroStar, BAA Training. Southwest’s single-type 737 fleet enables flexible crew scheduling worth hundreds of millions annually.

25 Leeham News, Bjorn Fehrm analysis. Trip cost differences in low single digits. Boeing claims 5% better; Airbus claims 10% better. Leeham: both exaggerated, real difference negligible. Per Leeham News.

26 A321XLR: EASA type certification July 19, 2024. First delivery to Iberia October 30, 2024. First revenue service: Madrid to Boston, November 14, 2024. Range: 4,700 nm. Over 550 ordered. Per Airbus, Simple Flying.

27 Leeham News, September 30, 2025: “the two margin-rich variants, the A321LR and XLR, the Boeing 737 MAX 10 can’t compete with once it gets certified.” Any A321neo becomes an LR with additional center tanks, no structural modification. Leeham broader view: Airbus ~54% narrowbody share, Boeing ~33%. Per Leeham News.

28 A321neo: ~7,064 orders (88 disclosed customers, mid-2025), ~1,752 delivered, backlog ~5,300+. Most ordered single-aisle variant in aviation history, surpassing the 737-800 in July 2023. Per Airbus Orders & Deliveries, Leeham News.

29 Analysts project Airbus controls 82-84% of committed backlog in the 180-230 seat category through 2030. Per Fleet Wire, Aerospace Global News.

30 Ortberg, Q4 2025 earnings call, January 27, 2026: “We still anticipate certification for both the 737-7 and 737-10 in 2026.” FAA has declined to commit to a date. Per Motley Fool transcript, CNBC.

31 Malave, Q4 2025 earnings call: ~30 MAX 10 airframes built in 2026, “will not be delivered in 2026. Be delivered in 2027. Upon certification.” UBS Conference, December 2, 2025: expects MAX 10 certification “to be later in” 2026. Per Boeing investor relations.

32 Boeing North Line: fourth 737 MAX final assembly line in Everett, repurposed from widebody space (747 ended 2022, 787 to South Carolina). Dedicated to MAX 10 (“has the most complexity”). Tooling complete, targeting mid-summer 2026. Renton lines handle rate 42 → 47; North Line enables path to rate 63. Per Simple Flying, Spokesman-Review, Reuters, Boeing Q4 2025 call.

33 ~35 MAX 7 and MAX 10 stored: ~26-27 MAX 7s (averaging 3.1 years age), ~4-5 MAX 10s. Boeing cautious about building MAX 10s ahead of certification. Per Forecast International (April 2025), FlightGlobal, Boeing Q4 call. See also Forty-Six to Nineteen, footnote 32.

34 Airbus: ~29x 2026E consensus EPS. Per Bloomberg consensus. See What Safran Can’t Fix, footnote 34.

35 Moody’s, December 12, 2025. Affirmed Baa3, outlook negative to stable. Upgraded governance rating to G-4. SVP Roche: “The stable outlook reflects our expectation that ongoing enhancements in Boeing’s quality control and safety processes will support improvements in assembly operations.” Upgrade conditions: debt/EBITDA approaching 3.0x, FCF above $8 billion, “years away.” Per Moody’s Rating Action.

36 Fitch, June 30, 2025. Revised outlook to stable, affirmed BBB-. Could support upgrade “in six to 12 months” if operational momentum sustained. Conditions: EBITDA leverage below 4.0x in 2026, 3.0x in 2027; gross debt below $50 billion. That window (December 2025-June 2026) is running. Per Yahoo Finance/Reuters, FlightGlobal.

37 Ortberg, Q4 call: “Supply chain harmony has to happen in that 47 to 52 rate… Spirit has some work to do.” Rate 47 slipped from 2026 to 2027. Increments of five, minimum six-month gap. 2026 delivery guidance: 500 MAX, 90-100 787. FCF: $1-3 billion (including ~$1 billion Spirit integration headwind). Per Boeing investor relations.

38 Quality. 787: average rework hours reduced nearly 30% in 2025 (Ortberg, Q4 call; this is 787-specific, not company-wide). 737 travelled work: down ~75% since February 2024, ~50% at roll-out. 5,100+ work instructions simplified. Per Boeing investor relations, SC Daily Gazette.

39 Credit ratings early 2026: Fitch BBB- stable (June 30, 2025), S&P BBB- stable (October 31, 2025), Moody’s Baa3 stable (December 12, 2025). All three at lowest investment-grade rung. Per S&P Global, Moody’s, Fitch.

40 Ortberg, Senate testimony and Q4 2025 earnings call: “I’m not pressuring the team to go fast. I’m pressuring the team to do it right.” Also: “We haven’t fully turned the corner, but we’re making real progress.” Per Boeing investor relations, CNBC.