Shared constraints get worse when the competitor starts executing.

Boeing delivered 46 aircraft in January 2026. Airbus delivered 19.1 It was the lowest January for Airbus since the pandemic, following a December in which 136 aircraft were contractually delivered, 17.2% of the annual total, and physically ferried to operators throughout January.2 The 136-to-19 pair is one event split across a calendar boundary, and January alone overstates the gap.

February was less distorted. Boeing delivered an estimated 52, anchored by 43 737 MAXs. Airbus delivered an estimated 33, led by 23 A320neo-family narrowbodies.3 Through two months: an estimated 98 to 52. Boeing also led net orders in January (103 to 49), its first monthly lead since at least early 2019.4

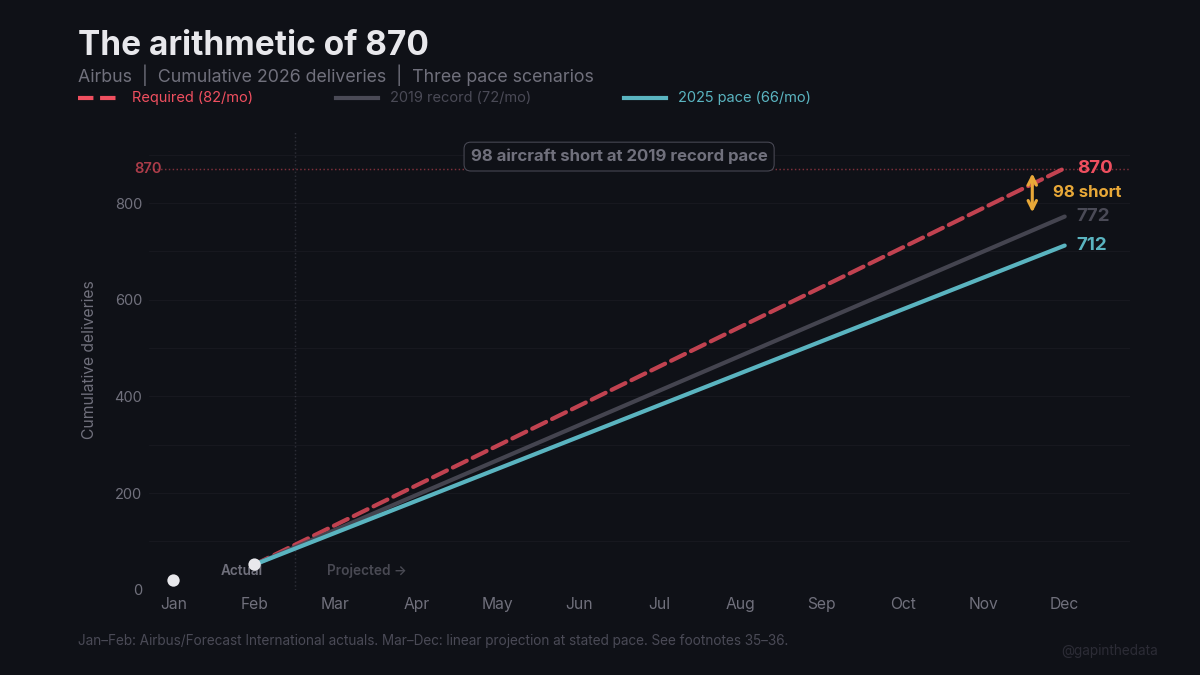

Airbus shares fell 6 to 8% on February 19, depending on reference price, when Faury guided 870 deliveries against a consensus above 900.5 Boeing shares were at a twelve-month high.6

The financial press framed this as a competition story: Boeing is “catching up,” Airbus is “under pressure.” The framing misreads the structure. The two companies share a supply chain, and Boeing’s acceleration tightens the constraints already binding on Airbus.

I. Claim One is growing

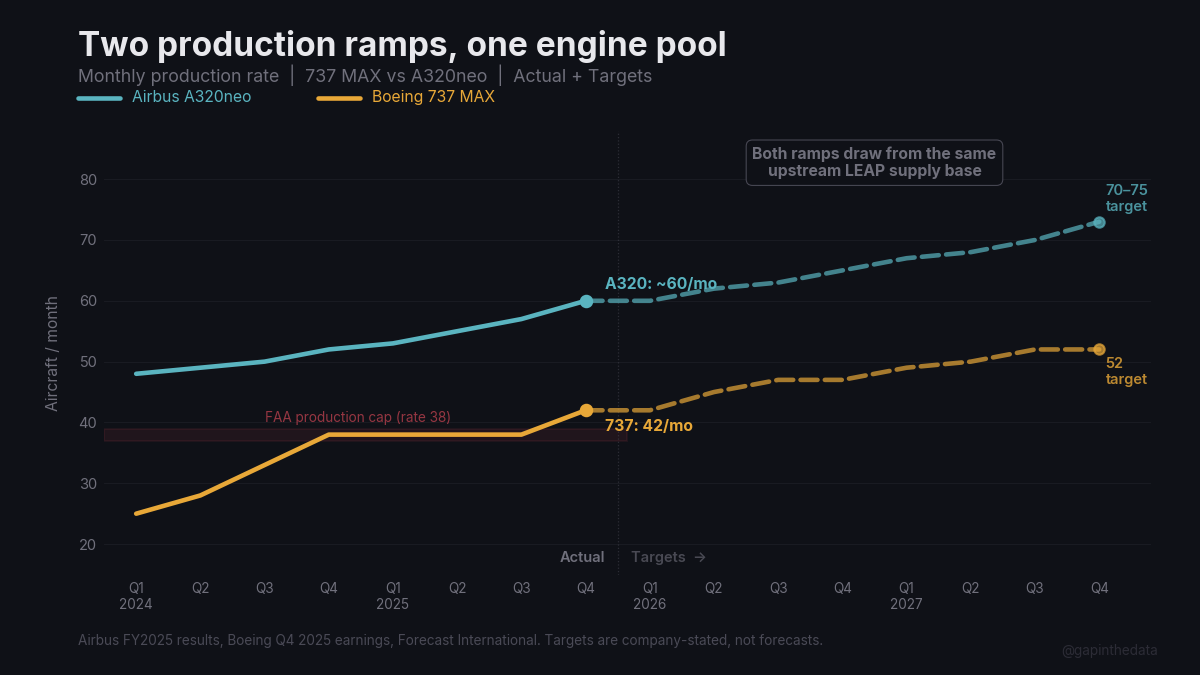

What Safran Can’t Fix identified five competing claims on every LEAP engine CFM International produces. Boeing was Claim One: 447 737s delivered in 2025, requiring roughly 890 LEAP-1Bs before spares.7

That claim is accelerating: Boeing exited 2025 at rate 42 (forty-two 737 MAXs per month) after the FAA lifted an eighteen-month production cap imposed following the door plug incident.8 The target is rate 47 by mid-2026 and rate 52 thereafter.9 Boeing has missed rate targets repeatedly since 2019, and the 47-to-52 sequence depends on a supply chain that was dysfunctional eighteen months ago, but even at the current rate 42, Boeing requires approximately 1,008 LEAP-1B engines per year for new aircraft, before spares. At rate 47: approximately 1,128. At rate 52: approximately 1,248.10 All three exceed Boeing’s 2025 consumption.

The LEAP-1A (A320neo) and LEAP-1B (737 MAX) are assembled on separate final assembly lines, Villaroche for the 1A and Durham for the 1B, so the competition is not for finished engines but for the upstream supply base: high-pressure turbine blades, compressor disks, forgings, castings.11 CFM does not publish the variant split.12

Safran’s total LEAP output grew 28% in 2025.13 If that pace continued, total upstream capacity could theoretically accommodate both ramps. But Faury already conceded that it will not. On February 19, he confirmed that CFM “will not be able to deliver more engines in 2026 than already committed."14 Safran’s new Morocco LEAP-1A assembly line does not come online until 2028.15

The five claims compete more intensely as Boeing’s upstream demand grows. Rate 75, Airbus’s A320neo production target, has slipped to “70 to 75 by the end of 2027."16 Reaching it requires the shared upstream base to expand capacity for Airbus while simultaneously feeding a Boeing that is ramping, an aftermarket that is tripling, and a spare engine pool that every new fleet entrant draws from. When Boeing was in crisis, CFM’s upstream allocation was effectively Airbus-first by default; that ended when the FAA lifted the production cap.

II. The Spirit inversion

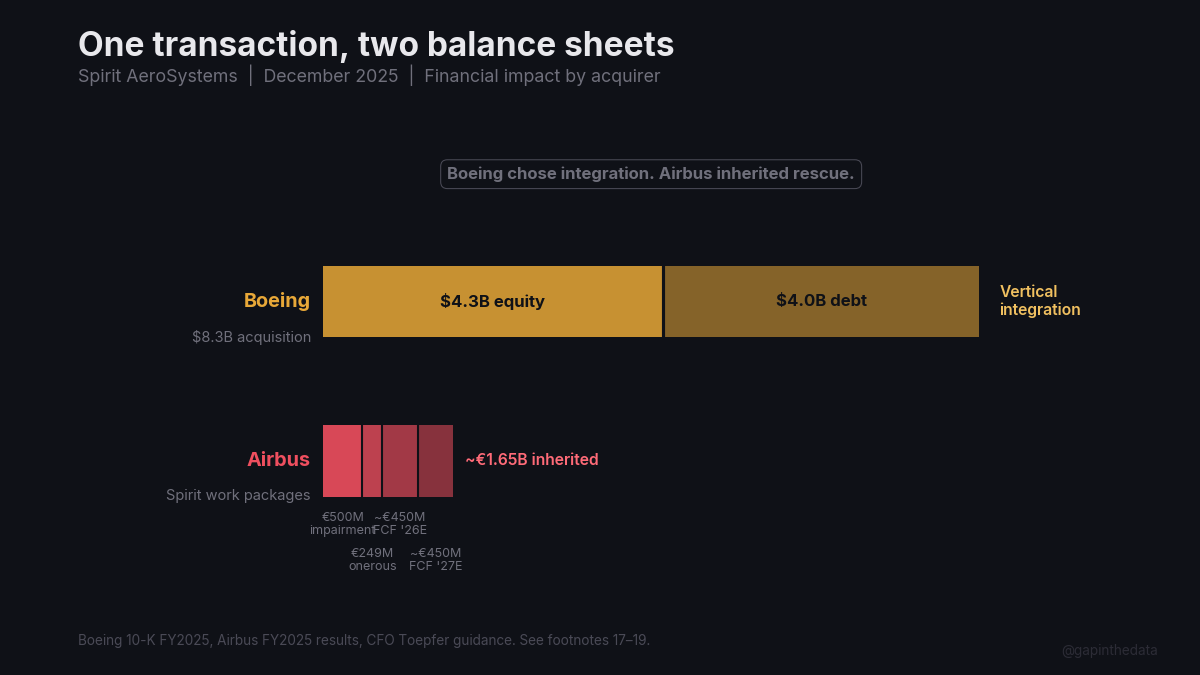

The same transaction appears in both companies’ financial statements with opposite signs.

Boeing completed its $8.3 billion acquisition of Spirit AeroSystems in December 2025, reintegrating 70% of 737 aerostructure production and major structures for the 787, 767, and 777.17 On the same day, Airbus took over Spirit’s Airbus-related work packages: A220 fuselage, A320 and A350 structures, six facilities, more than 4,000 employees.18 The financial impact on Airbus, detailed previously, runs to hundreds of millions in impairments, onerous contract provisions, and projected negative cash flow through 2027.19

For Boeing, the logic is vertical integration. The fuselages that were arriving with incorrectly drilled holes and wrong-spacing fasteners are now under direct quality control.20 Whether reintegration fixes the quality culture that produced those defects is unproven; Boeing’s own quality problems predate Spirit’s 2005 spin-off, and the door plug that blew off an Alaska Airlines MAX 9 came from a Boeing-supervised production system. Reintegration gives Boeing control over a culture it created and then allowed to degrade.

For Airbus, the logic is rescue. Spirit’s work packages were loss-making before Airbus acquired them, and someone had to take them.21 Bringing them in-house moved the losses from Spirit’s balance sheet to Airbus’s and added integration costs on top.

Spirit’s constraint on A350 fuselage panels remains the primary bottleneck preventing the A350 from reaching rate 12.22 Boeing’s Spirit integration is attempting to address the equivalent constraint on the 737 directly. The asymmetry is structural: Boeing chose to reintegrate the core of its production system; Airbus inherited the obligation to fix someone else’s.

III. The cash flow gap

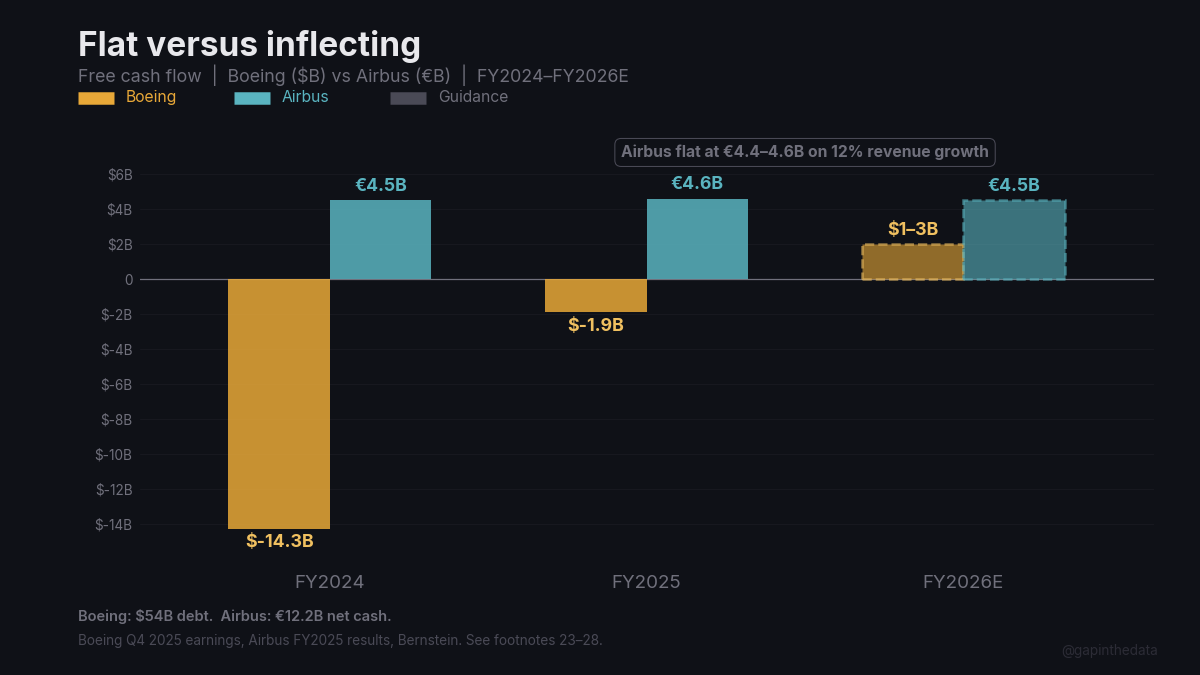

Boeing reported Q4 2025 free cash flow of $375 million, its first positive quarter since the door plug incident, on operating cash flow of $1.3 billion.23 Full-year 2025 FCF was still negative $1.9 billion, down from negative $14.3 billion in 2024, and Boeing guided 2026 at $1 to $3 billion.24,25 Airbus guided 2026 free cash flow before customer financing of approximately €4.5 billion.26

At current exchange rates, Airbus’s guided FCF is roughly two to five times Boeing’s, and the absolute gap persists. Boeing’s trajectory is the shift: from negative $14.3 billion to negative $1.9 billion to a positive guide, while Airbus’s FCF has been essentially flat at €4.4 to €4.6 billion on 12% revenue growth.27 Ortberg has stated the company is “marching to” a $10 billion FCF target; Bernstein models $9 to $10 billion annually by 2028.27

Boeing’s balance sheet qualifies every comparison. Airbus holds approximately €12.2 billion in net cash; Boeing carries approximately $54 billion in total debt against $29.4 billion in cash and investments.28 Boeing’s FCF must service that debt before a dollar becomes available for investment, and Boeing’s guidance track record, with annual targets missed every year from 2019 through 2024, gives the $1 to $3 billion range a wider confidence interval than Airbus’s demonstrated €4.5 billion. The Bernstein target sits two years out, from analysts whose sell-side estimates for Boeing have been systematically optimistic over the same period.

The distinction between absolute gap and direction of travel matters for supplier leverage. Airbus’s financial strength is real, but its relative advantage is narrowing. When a competitor is in crisis, suppliers have no alternative buyer for marginal capacity; when that competitor is ramping and generating cash, suppliers have options. Long-term take-or-pay contracts, technical lock-in, and Airbus’s larger single-aisle order book all insulate it, but the direction favours Boeing at the margin.

Pratt & Whitney’s decision to “reallocate more to the in-service” fleet at Airbus’s expense is driven by the GTF recall; Boeing does not use the PW1100G.29 But Pratt’s willingness to prioritise the recall over Airbus’s production needs is easier to sustain in a market where Airbus has less pricing leverage than it did when Boeing was grounded.

IV. What certification unlocks

The 737 MAX 7 and MAX 10 remain uncertified, and Boeing has missed every certification date since 2019.31 The expiration date on Airbus’s uncontested position in these segments is nonetheless approaching. Southwest Airlines, which holds approximately 90% of all MAX 7 orders and operates 310 first-generation 737-700s requiring replacement, expects FAA certification by August 2026.30 The same skepticism this analysis applies to Airbus’s rate 75 timeline applies to Boeing’s certification timeline, but the direction is toward resolution: FAA review is underway, Boeing has completed the engine anti-ice redesign, and 35 stored aircraft await delivery.32

If the MAX 7 is certified in 2026, it competes directly with the A220-300 in the 130- to 160-seat segment, where Airbus is still trying to reach breakeven. If the MAX 10 follows in late 2026 or 2027, it enters the A321neo’s market.31 The A321neo has operated effectively uncontested for three years, allowing Airbus to push pricing. Even partial certification progress introduces competitive pressure into Airbus’s pricing model.

The A220-500, the stretched variant Airbus is reportedly marketing for a potential 2027 programme launch, would enter a market where the MAX 7 may already be certified and the A220-300 still loses money.33 The investment case for a derivative is weaker when the base programme is unprofitable and the competitive gap has closed.

V. The backlog question

Airbus reported a backlog of 8,754 aircraft at year-end 2025, roughly 9.7 years of production at projected rates.34

A backlog only converts at the rate the production system allows, and Airbus’s system is constrained at every major stage. The 870-unit guidance requires 82 deliveries per month for the remaining ten months after an estimated 52-unit start.35 The all-time monthly average, set in 2019, is 72.36

Boeing’s backlog is converting at a steadier pace (46 in January, an estimated 52 in February, rate 42 heading to 47), though Boeing has its own stored aircraft, its own quality problems, and its own history of missing production targets. Airlines already in Airbus’s queue cannot switch; engine selection, pilot training, and fleet commonality create switching costs measured in billions.37 But airlines placing new orders can.

Boeing leading net orders in January is one data point, and January is often noisy. But some of what drove it was structural: Qatar’s $96 billion widebody order during Trump’s Doha visit (130 787s and 30 777Xs) went entirely to Boeing.38 The deal was diplomatic as much as commercial, part of a $1.2 trillion bilateral package, and no less real for it. Airlines whose governments are negotiating with Washington buy Boeing. Airbus’s political leverage in that market is near zero.

Airbus trades at approximately 29 times 2026 estimated earnings.39 Boeing still carries $54 billion in debt, a 777X programme seven years behind schedule, and the operational consequences of the door plug incident.40 Both companies’ constraints persist, but the competitive context around them has shifted. For four years, Airbus’s constraints were offset by the absence of a functioning competitor, and that offset is ending. Engines, fuselages, and supplier capacity all bind harder when both manufacturers are pulling from the same pool.

Footnotes

1 Airbus, January 2026 Orders and Deliveries, February 6, 2026: 19 aircraft to 15 customers. Boeing, January 2026 Orders and Deliveries: 46 aircraft, 103 net orders. Per Forecast International, AeroTime.

2 Airbus December 2025: 136 aircraft, 17.2% of 793 annual total. See What Safran Can’t Fix, footnote 22. Forecast International: aircraft “contractually delivered on December 31st to support year-end performance metrics were physically ferried to their operators throughout January.”

3 Forecast International, “February 2026 Commercial Aircraft Production,” March 2, 2026. Boeing estimated 52 (43 MAX, 4 767, 2 777, 3 787). Airbus estimated 33 (23 A320neo-family, 8 A220, 2 A350). February described as “notably weak” for Airbus.

4 Boeing January 2026: 103 net orders versus Airbus’s 49. Boeing last led Airbus in annual net orders in 2018; individual monthly leads may have occurred between 2019 and 2025 but are not tracked in the public data with precision. Per Simple Flying, ePlaneAI.

5 Airbus (AIR.PA) fell from approximately €200 to intraday lows of €185–187 on February 19, 2026. Decline estimates range from 6.2% to 7.9% depending on reference price and timing. Per Investing.com, CNBC. See also Thirty-Three Percent, footnote 3.

6 Boeing (BA) twelve-month performance. Bernstein raised price target to $298, named Boeing a “best idea” for 2026. Per CNBC.

7 Boeing delivered 447 737s in 2025, nearly all MAX variants. At two engines per aircraft: approximately 890 LEAP-1Bs. See What Safran Can’t Fix, footnote 5.

8 Boeing exited 2025 at rate 42 after FAA approval in September 2025. Production had been capped at 38/month since shortly after the Alaska Airlines 737 MAX 9 door plug incident (January 5, 2024). Per FlightGlobal.

9 Boeing VP Katie Ringgold, 737 Program: rate 47 by “late spring or early summer” 2026. Rate increases proceed in increments of five (42–47–52–57), with no less than six months between steps. Ortberg and Ringgold have cited 47 and 52 as the next two targets; earlier Boeing guidance referenced rate 53 by end of 2026, which may reflect rounding or a revised milestone. Per Simple Flying, Air Data News, FlightGlobal.

10 Author’s calculation. Rate 42 x 12 x 2 = 1,008. Rate 47 x 12 x 2 = 1,128. Rate 52 x 12 x 2 = 1,248. Excludes spare engines, which Safran reports at “still elevated” ratios.

11 LEAP-1A final assembly: Safran Aircraft Engines, Villaroche, France. LEAP-1B final assembly: GE Aerospace, Durham, North Carolina, and Lafayette, Indiana. Shared upstream components include high-pressure turbine blades (LEAP-1A and -1B use common HPT architecture), forgings, castings, and composite fan blades. Upstream suppliers serve both variant lines from the same production base. Per Safran investor presentations, GE Aerospace investor day 2025.

12 Neither Safran nor GE Aerospace publishes the LEAP variant breakdown (1A/1B/1C). The 1,802 total is aggregate across all three platforms. See What Safran Can’t Fix, footnote 1. Without the variant split, the exact magnitude of upstream competition cannot be quantified.

13 Safran FY2025 results, February 13, 2026. LEAP deliveries: 1,802 (+28% YoY). Q4 acceleration: +49%. See What Safran Can’t Fix, footnote 1.

14 Airbus Annual Press Conference, February 19, 2026. Faury on CFM supply: unable to deliver additional engines beyond existing commitments. Per CNBC. Note: Faury’s comments were reported via CNBC’s coverage of the press conference and analyst call; the specific quote on CFM capacity constraints does not appear verbatim in the press conference transcript and may derive from the separate analyst call.

15 Safran FY2025 results, February 13, 2026. Morocco LEAP-1A final assembly line: first engine 2028, capacity approximately 350/year by 2030. See What Safran Can’t Fix, footnote 10.

16 Airbus FY2025 press release. A320 family: “70 to 75 aircraft per month by end of 2027, stabilising at rate 75 thereafter.” Previous targets: rate 75 by 2025, then 2026, then 2027. Per FlightGlobal, Yahoo Finance.

17 Boeing, “Boeing Completes Acquisition of Spirit AeroSystems,” December 2025. Total value $8.3 billion including approximately $4 billion in assumed debt. Spirit fabricates approximately 70% of 737 aerostructure. Per Manufacturing Dive, Forecast International.

18 Airbus acquired Spirit’s Airbus-related operations on December 8, 2025: Belfast, Prestwick, Kinston (North Carolina), Saint-Nazaire, Casablanca, and Saint-Eloi (Toulouse). Over 4,000 employees transferred. See Thirty-Three Percent, footnote 15.

19 Airbus FY2025 financial statements. Spirit impact: €500M A220 impairment, €249M onerous contract provisions, €122M transaction costs, partially offset by €738M IFRS 3 gain. Net: -€188M. CFO Toepfer: turnaround “about three years,” “mid-triple-digit million” negative FCF in 2026 and 2027. See The Margin Trap, footnote 9.

20 Boeing production quality disclosures. Spirit-produced fuselages had issues with incorrectly drilled holes and fastener spacing. Per NPR, CNBC.

21 Spirit AeroSystems, quarterly results through Q3 2025. Going-concern doubt in every filing. Forward losses: $1.1 billion through 9M 2025. “Lack of price increases on Airbus programs” cited as cash flow drag. See The Margin Trap, footnote 13.

22 Forecast International, February 2025. Spirit fuselage panel constraints limit A350 to approximately 6/month; rate 12 “likely not before 2029.” See The Margin Trap, footnote 5.

23 Boeing Q4 2025 results, January 27, 2026. Operating cash flow $1.3 billion. Free cash flow $375 million (non-GAAP). First positive quarter since Q4 2023. Per Sherwood News.

24 Boeing FY2025 free cash flow: negative $1.9 billion. FY2024: negative $14.3 billion. Per Boeing investor relations.

25 Boeing 2026 guidance: more than 700 deliveries, $1 to $3 billion free cash flow. CEO Ortberg, Q4 2025 earnings call, January 27, 2026: “$1 billion and $3 billion” FCF range, with first-half cash usage and second-half acceleration. Capital expenditures projected at $4 billion, including Spirit integration. Per Boeing earnings release, CNBC.

26 Airbus 2026 guidance: approximately 870 deliveries, approximately €7.5 billion EBIT Adjusted, approximately €4.5 billion FCF before customer financing.

27 Ortberg, Q4 2025 earnings call: “We’re marching to this $10 billion free cash flow number and it's going to take us a little bit of time but we've got a methodical plan to get there." Bernstein, February 2026: Boeing price target raised to $298, FCF estimate $9--10 billion annually by 2028. JPMorgan raised Boeing price target to $245. Airbus FCF: €4.7B (FY2022), €4.4B (FY2023), €4.5B (FY2024), €4.6B (FY2025), €4.5B (2026 guidance). Revenue: approximately €65.4B (FY2023) to €73.4B (FY2025), +12%. See Thirty-Three Percent, footnote 27. Note: Boeing’s FCF guidance track record has been poor; sell-side estimates for Boeing have been systematically optimistic over the same period.

28 Airbus net cash position: approximately €12.2B (FY2025). Boeing total debt: $54.1B post-Spirit (including approximately $4B assumed from Spirit); cash and investments $29.4B at end of Q4 2025. Net debt approximately $24.7B. Per Boeing Q4 2025 earnings release, Airbus FY2025 results.

29 Faury, press conference, February 19, 2026: “We are very frustrated that they have decided to reallocate more to the in-service because they miss global capability and to the detriment of Airbus.” The GTF recall requires inspecting all PW1100G engines with affected powder-metal turbine disks, a programme Pratt expects to extend through end of decade. Boeing does not use the PW1100G; the reallocation is recall-driven, not Boeing-driven. See Thirty-Three Percent, footnote 22.

30 Southwest Airlines: MAX 7 certification expected by August 2026, first flights 2027. Southwest holds approximately 90% of MAX 7 orders. Fleet includes 310+ 737-700s requiring replacement. Per Simple Flying.

31 Boeing certification timeline. MAX 7 originally expected 2019; MAX 10 originally expected 2020. Delays driven by MCAS redesign, production cap, engine anti-ice system redesign, and SMYD software exemption process (ALPA opposed). Current estimates: MAX 7 mid-to-late 2026; MAX 10 late 2026 to early 2027. Per AerospaceGlobalNews, FlightGlobal, The Air Current.

32 Boeing has approximately 35 MAX 7 and MAX 10 aircraft stored awaiting certification. Per FlightGlobal.

33 A220-500: stretched variant targeting approximately 180 seats. Airbus running targeted sales campaign. Potential 2027 programme launch. Per AeroTime, Simple Flying. Avolon 2026 “Up Next” report forecasts new programme launch in 2027.

34 Airbus backlog at December 31, 2025: 8,754 aircraft per Airbus FY2025 press release. Forecast International estimated approximately 8,777 units as of January 31, 2026 (the difference from simple net-order arithmetic of 8,784 likely reflects order adjustments and conversions not captured in the headline figures). At projected 2026 deliveries of approximately 902 (Forecast International estimate): 9.7 years. Per Forecast International, February 10, 2026.

35 Author’s calculation. 870 target minus estimated 52 (January and February) = 818 remaining over 10 months = 81.8/month. See What Safran Can’t Fix: “Eleven months remain to deliver 881, or 80.1 per month.” Note: Three Chokepoints, published before the Forecast International February estimate, used a lower February estimate and calculated 83/month; the March 2 data revised this.

36 2019 record: 863 deliveries / 12 months = 71.9/month average. See What Safran Can’t Fix, footnote 28.

37 Engine selection locks airlines in for fleet life: training, tooling, spares, maintenance contracts. See What Safran Can’t Fix.

38 Qatar Airways, May 2025. Deal for 130 787 Dreamliners and 30 777Xs, with options for 50 additional aircraft. Valued at $96 billion. Signed during Trump's Doha visit as part of a $1.2 trillion economic commitment package. Per CNN, France 24.

39 Airbus: approximately 29x 2026E consensus EPS. See What Safran Can’t Fix, footnote 34.

40 Boeing 777X: originally targeted 2020 entry into service; currently targeting 1H 2027 certification, seven years late. Alaska Airlines 737 MAX 9 door plug incident: January 5, 2024. Boeing total debt: $54.1 billion post-Spirit. Cash and investments: $29.4 billion at end of Q4 2025.