Full transcript of Airbus’s annual press conference, Toulouse, February 19, 2026. Speakers: Guillaume Faury (CEO), Thomas Toepfer (CFO), Guillaume Steuer (Head of External Communications). For our analysis, see Thirty-Three Percent.

Video Voiceover: Humankind is made to explore, to share, to dream. Make the impossible possible. Delivering what’s needed, enriching our everyday lives, taking us home. Airbus makes the connection. We reach further to satisfy our curiosity, looking beyond horizons. We innovate to make a better tomorrow, to improve what is and to build what’s next and to progress. Our world must be safe. When it matters most, Airbus is there. To unite, to connect, to protect. This is our purpose: to Pioneer sustainable Aerospace for a safe and United world. Airbus, made to matter.

Guillaume Steuer: Good morning ladies and gentlemen and welcome to our Airbus event center. Thank you for being here with us today for our annual press conference where we will present and discuss our 2025 results. And a big thank you for all of you and all of those who are following us online today.

My name is Guillaume Steuer, I look after external communications and media relations for Airbus. And here with me to present the results are Guillaume Faury, our CEO, and Thomas Toepfer, our CFO.

Guillaume will start today by sharing a few highlights about last year, 2025. And Thomas will provide you then more details about our financials. And finally, Guillaume again will discuss our Outlook and priorities for 2026. And then we’ll move on to our Q&A session which also those of you following online can take part in by submitting questions using the live e-tool.

As always with these things, this entire conference is going to be in English and there will be no simultaneous translations. So now ladies and gentlemen, just as usual please familiarize yourself with our Safe Harbor statement which you can now see on your screens. And please remember that in this conference all forward-looking statements such as in our guidance are based on assumptions. And as conditions may change so may our projections and plans.

So before I hand over to Guillaume for this overview of 2025 we wanted to share with you another short video which we think captures some of the key achievements of team Airbus in 2025. And I hope you enjoy it as much as the teams enjoyed putting it together. So we’ll be back with you in a moment after the video.

Over to you, Guillaume.

CEO Remarks

Guillaume Faury: Thank you, Guillaume. Two Guillaumes on stage. Thank you and hello everyone. Thank you for joining us here in Toulouse and online. You will have seen from the video that last year was a colorful and exciting one.

2025 was indeed a landmark year characterized by very strong demand for our products and services across all businesses, in both civil and defense. We navigated a complex and dynamic global environment. Our primary focus being to manage supply chain constraints that created a disconnect, a desynchronization between production and delivery over the year.

In commercial aircraft we continue to expand our industrial footprint to support our production ramp up. We completed the acquisition of certain Spirit AeroSystems work packages with the closing on the 8th of December. And we opened new final assembly lines in the U.S. and in China for the A320. Going forward the shortage of engines from Pratt & Whitney will require this year our ongoing focus to secure our delivery trajectory. I will get back to this point in a moment.

Our helicopter division delivered a strong performance from programs and growth in services. This is true on the civil side where we are maintaining our leadership position and on the defense side where our market share is growing.

Finally in defence and space we’re reaping the fruits of the transformation of the division and we are capturing the momentum created by increased defence spending in Europe and worldwide.

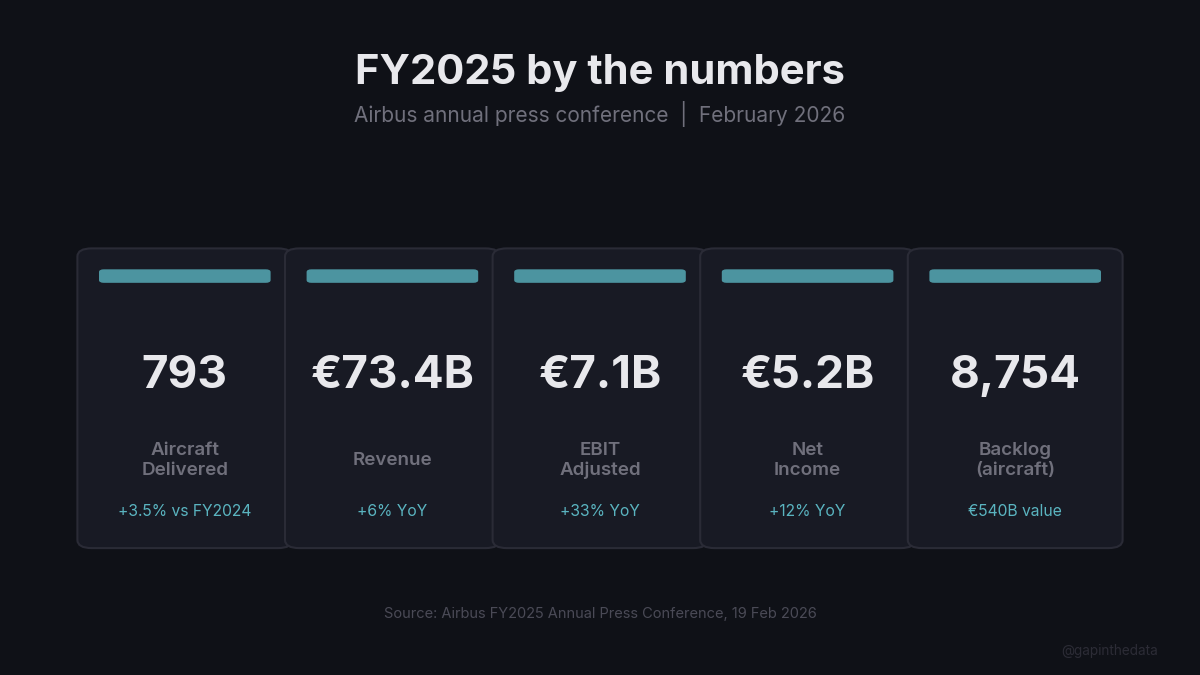

Overall Team Airbus did a great job in 2025. We delivered on our commitments meeting our updated guidance with 793 commercial aircraft deliveries. This demonstrated our collective resilience in the face of persistent and significant headwinds in our supply chain and in the broader global environment. Overall this translated into a strong financial performance for 2025 with a record EBIT Adjusted of 7.1 billion euros and a record net income of 5.2 billion euros supporting our 2025 dividend proposals of 3.2 euros per share. Thomas will give you more details on our 2025 financials in a moment.

Now let’s take a closer look at a commercial aircraft business. We disclosed our 2025 order and deliveries last month already and I will go quickly over the numbers. Overall we delivered as I said 793 to 91 customers representing a year on year increase of 4%. The A320 panel quality issue we faced at the end of 2025 was a significant event that put pressure on our ability to deliver in an already back loaded year. We took immediate steps to address the challenge putting a strong focus on quality and therefore unfortunately impacting our 2025 deliveries.

During the year we won repeat orders and key new customers in both single aisle and wide-body campaigns, booking one thousand gross orders. And we ended 2025 with a record backlog of 8,754 aircraft.

In 2025 we delivered 607 aircraft from the A320 family and we booked 656 gross orders, bringing the backlog of the A320 family up to 7,163 aircraft. The A321 XLR, our latest addition to the family, also continued to attract new customers.

Almost 39 years ago to the day, actually on the 22nd of February in 1987 the A320 made its first flight. Last year it officially became the most delivered commercial aircraft of all times. We saw that on the video. I can’t resist and take a second to honor the Airbus Pioneers who made it possible and to thank the customers who have turned it into such a global success.

And switching to another innovative single aisle aircraft, on the A220 we delivered 93 aircraft in 2025 representing an increase of around 25% year on year and we booked 49 new orders. So 93 A220s, 607 A320s that makes 700 single aisle and then again 93 for the wide bodies makes 793.

On the wide bodies we delivered 36 A330s and 57 A350s. Looking at orders on the A330, sorry, we booked 102 gross orders in another strong year confirming the high demand for this versatile aircraft. On the A350 we received 193 gross orders underpinning the good commercial momentum which was also a successful year for the A350 freighter variant with 28 new gross orders.

Now looking ahead at the specific production ramp up plans for each program. On the A220 family the ramp up is ongoing and paced by the integration of Spirit AeroSystems work packages and the balance between supply and demand. As we continue to make tactical adjustments on this ramp up trajectory we are now targeting a rate of 13 aircraft a month in 2028.

On the A320 family, Pratt & Whitney’s failure to commit to the number of engines ordered by Airbus is negatively impacting this year’s guidance and the ramp up trajectory for this year. As a consequence we now expect to reach the rate of between 70 and 75 aircraft a month by the end of 2027 stabilising at rate 75 thereafter.

On the A330 there’s no change and we continue to target rate 5 in 2029. And there’s also no change on the A350 where we continue to target rate 12 in 2028.

Helicopters. 2025 was an outstanding year for helicopters which delivered 392 units, 31 more than in 2024. We booked 536 net orders compared to 450 in 2024 with a book to bill well above one both in units and value including a strong contribution from the military segments and a good order intake from services. We continue to see positive momentum in particular in military markets. Notable contracts included the order for 100 helicopters from the Spanish Ministry of Defence, the largest helicopter purchase by this customer. The Super Puma family kept performing well on the market with an important contract with the Royal Moroccan Air Force for 10 H225Ms signed in the second half of the year. And we also saw the German armed forces reinforcing their commitment by firming up options for 20 additional H145M military helicopters.

The division’s drone range also recorded notable successes with contracts for the Flexrotor small tactical unmanned air system as well as for the larger VSR 700 system, a 700 kilogram unmanned rotorcraft which we see on the picture, which was ordered by the French Ministry of Defence.

And finally we are actively preparing the future of our helicopter range. The military version of the H160 made its maiden flight last year ahead of force deliveries planned at the end of 2028. And we announced the launch of the H140 which you can also see on the slide, designed to complement our current range of light twin engine helicopters particularly for EMS emergency medical services. And we did that at the Verticon show in Dallas last year.

And now moving to defence and space. 2025 reflected one more year of record order intake which stood at 17.7 billion euros corresponding to a book to bill of around 1.3. The performance of the Division last year was also the result of our transformation efforts which are now paying off.

Looking more closely at our activities 2025 was an excellent year for the Eurofighter program. We recorded an order for 20 aircraft from Germany, 8 for Italy, and we also welcome Turkey to the program with an order for 20 aircraft. To support this growing demand we represent ramping up production of the Eurofighter along with our program partners.

In 2025 we also recorded the first order for the new A330 MRTT Plus, an evolution of the existing MRTT based on the re-engined A330neo, new engine on the 330. It’s an important milestone that ensures the world’s most successful tanker will remain successful for the next decade.

While on air power and given how much has been written on the topic lately let me say a word on FCAS. At Airbus we believe that the European need for an ambitious future combat air system is unchanged. And we also believe an ambition of this scale can only be delivered through cooperation fostering operational interoperability and life cycle synergies for European Air Forces. But the deadlock of a single pillar should not jeopardize the entire future of this high-tech European capability which will bolster our collective defence. If mandated by our customers, we would support the two Fighters solution and are committed to playing a Leading Role in such a reorganized FCAS delivered through European cooperation.

Now, coming back to our 2025 performance and looking at space systems. Airbus was selected by Eutelsat to build a further 341 OneWeb Low Earth orbit satellites complimenting the first 100 recorded in 2024. All these satellites will be produced at our Toulouse site not far from here and will be an important contribution to Europe’s efforts to strengthen its sovereignty in LEO constellations.

In space last year’s agreement with Thales and Leonardo to bring together our satellite and space services activities was obviously an important Milestone. At Airbus we firmly believe that by pulling resources, skill and capabilities we’ll be able to create a new leader rooted in Europe enabled to compete globally. Scale will help increase industrial efficiency, lower cost and ensure that Europe can maintain its autonomy across the strategic space domain. We’ll continue to work closely with our partners to ensure this proposed joint venture can be established as quickly as possible while going through all necessary steps and approvals.

And now this concludes the overview of our 2025 achievements across businesses I wanted to share with you. Handing over to you, Thomas, for a detailed look at our financials.

CFO Remarks

Thomas Toepfer: Well thank you very much Guillaume and Good Morning to everybody in the room and online. I will now talk and take you through our key financial elements for the financial year 2025. And overall I think we can say 2025 we delivered very strong financials across the board in a context of many challenges.

Now starting with the top line you can see our 2025 revenues increased to 73.4 billion euros which is up 4% year on year and it’s mainly reflecting the higher contribution from our divisions, the stronger services volumes across the business and also a higher level of deliveries which was then partially offset by the weakening of the US dollar.

Our 2025 EBIT Adjusted increased to 7.1 billion euros from 5.4 billion in ‘24. And of course let me remind you that in the financial year ‘24 after the completion of the in-depth technical review of our space programs we’ve recorded a total charge of 1.3 billion. Now in 2025 the higher commercial aircraft deliveries together with a more favourable hedge rate and lower R&D expenses were partially offset by the impact of tariffs, of which the vast majority actually occurred in Q4. And it also reflects a stronger performance in both of our divisions.

If you look at the earnings by business the commercial aircraft EBIT Adjusted increased to 5.5 billion from 5.1 billion a year earlier and that was driven by the increase in deliveries with a more favourable hedge rate and lower R&D expenses and as I said it was partially offset by the impact of tariffs which we had to digest.

If you look at helicopters the EBIT Adjusted in that division increased 13% year on year to 925 million euros and that is of course reflecting the higher deliveries as well as very solid growth in the service business.

And finally our EBIT Adjusted at Airbus Defence and Space stood at 798 million euros and that is reflecting the higher volumes and also is supported by the improved profitability in line with the mid-term trajectory that the division has given itself and it is of course also result of the successful transformation plan.

Now turning to the EBIT Consolidated Reported this was 6.1 billion Euros with the adjustments totalling a negative 1 billion. And namely that negative 1 billion includes a negative impact of 622 million from the dollar working capital mismatch and the balance sheet revaluation. And the resulting net income for 2025 is a record 5.2 billion euros with a reported earnings per share of 6.61 euros.

Last but not least you should and you can see it on the right hand side of the page our free cash flow before customer financing totaled 4.6 billion Euros in 2025 and that mainly reflects the level of deliveries, the commercial momentum across all our businesses resulting in very healthy pre delivery payment inflows and it was only partially offset by the planned inventory built up which is associated to the ramp up across all the programs that we have.

So that finally our net cash position for the year stood at 12.2 billion euros at the end of December which is also reflecting the weaker dollar environment and I would just like to emphasize that our total liquidity is still very healthy and stands at around 35 billion. And with that I would like to hand it back to you Guillaume.

Outlook

Guillaume Faury: Thank you Thomas. Our ambition to Pioneer sustainable aviation and our corresponding road maps remain key priorities for Airbus. We took a number of significant steps in 2025 and let me mention a few. During our Airbus Summit last year we presented an updated roadmap for our hydrogen aircraft research effort, a roadmap that takes stock of the slower than expected development of the global hydrogen economy and of our ambition to focus our efforts on solution that would enable a commercially viable and competitive product. In line with this approach we announced in June last year the signature of an agreement with MTU Aero Engines to collaborate on hydrogen fuel cell propulsion, the technology we have identified as the most promising for a future hydrogen aircraft.

In parallel we continue to mature a number of Key technology bricks for our next generation single aisle aircraft which we aim to bring to the market in the second half of the next decade. It will bring a step change in terms of decarbonization and competitiveness and we aim to reduce fuel burn by 25 to 30% compared with current modern generation aircraft.

On SAF, Sustainable Aviation Fuels, Airbus continues to partner with several Airlines to accelerate their development. To overcome the logistical challenges of physically delivering SAF to market, we launched a new book and claim demonstrator allowing customers to buy SAF and claim the corresponding CO2 emissions. And looking at our own operations at Airbus in 2025 we used 21% SAF in our aircraft and helicopter flights. This puts us on track to reach our goal to use at least 30% SAF in our operations by 2030.

And now let’s have a look at our Outlook and priorities this year and beyond. It starts with our guidance which I will read out to you now. As the basis for its 2026 guidance the company assumes no additional disruptions to Global trade or the world economy, air traffic, the supply chain and its internal operations and ability to deliver products and services. The company 2026 guidance is before M&A and includes the impact of currently applicable tariffs. On that basis the company targets to achieve in 2026 around 870 commercial aircraft deliveries, an EBIT Adjusted of around 7.5 billion euros and free cash flow before customer financing of around 4.5 billion euros.

In conclusion what will team Airbus be focusing on in 2026? The key Pillars that underpin everything we do as a company are unchanged. Going forward we will remain focused on safety, quality, integrity, compliance and security. Last year’s events, notably the A320 software recall, the ELAC-B topic and the fuselage panel issues, have only reinforced our resolve to put safety and quality first.

Our primary focus in 2026 will remain ramping up production in commercial aircraft where global demand continues to show that people around the world want and need to fly. And in defence where we intend to play a Leading Role in supporting Europe’s efforts towards sovereignty and security. Across all businesses we will continue to prepare the future in order to deliver profitable growth. Across the group we’ll do so by maturing the Technologies that will help decarbonise Aviation and prevail on tomorrow’s battlefields.

The world around us is changing fast and becoming more unpredictable. In this environment it takes the daily commitment of team Airbus to make a difference by delivering products that help to connect and protect people. Which is why in these volatile times we remain guided by our purpose to Pioneer sustainable Aerospace for a safe and United world. And on that note, inspiring to me, back to you Guillaume.

Q&A

Guillaume Steuer: Thank you very much Guillaume and Thomas for those opening remarks. So we will now start the Q&A session. Again, a few housekeeping remarks. So for those of you who are in the room please raise your hand and wait for one of our colleagues to come to you. And before you ask your question we would ask please to state your name and the name of the publication you’re working for. And for the media colleagues following us online you are and you can use the live e-platform for which you’ve received details and you can submit your questions in writing. Please do so in English. And in case you are experiencing any kind of technical difficulties please feel free to reach out to the communications team, the contact of which you have in the invitation.

So let’s begin the session now we will start by taking questions from the room with our colleagues here. So the floor is yours please raise Your Hands we can start over here. Daniel.

On A350 rates and the A220-500

Jens Flottau (Aviation Week): Thanks good morning. Jens Flottau, Aviation Week. Lars Wagner said in Dublin the other day that he would like to see a lot higher rates of production for widebodies and I was wondering whether Guillaume, what your view on that on this topic is. Related to this, how concretely are you looking at a A350-2000, a stretched A350? And finally what’s the latest on the A220-500?

Guillaume Faury: Thank you Jens. Well I agree with Lars. I’d like to see higher rates on the A350 as well because we have very strong demand. Now we are in a steep ramp up from where we are today to rate 12 in 2028. That keeps us busy. But we’re also looking at what it would mean, what it would require and by when to increase, significantly increase the rates on the A350. So it’s not for today. I agree with Lars we would like to see more but we have to work and do the homework before we take decisions and move forward.

The A350 family relies on a very strong platform. The product is very successful we booked significantly more than we can produce on the short term. And we see demand for a larger plane so that’s also something we are looking at. But again we are in the development phase of the freighter. It’s an important year for the freighter. We have to come to deliveries of the aircraft. So we are timing things one by one but we are seriously looking at what the further potential of the aircraft is and a stretch would be a natural evolution of the product. We are not at the point of decision we are at the point of working, of analysing, of listening to customers. But that’s indeed something possible.

And for the A220, a lot on our plates as well with the integration of the Spirit Aerosystems work packages and what it means for the A220 program so we keep ramping up. But we hear loud and clear from the market that there is a strong potential for what is called a 500. That would make plenty of sense. We had the opportunity to say earlier on that it’s more a question of when than if. We are not yet at the when. And we are not yet there either as you have seen we have plenty of things to do and we want to time things one by one. But this is also something we are seriously considering.

On the Bromo space JV

Jorge Penalba (Avion Revue): My name is Jorge Penalba from Avion Revue. Hello my question is for Guillaume about the new company that you are facing with Leonardo and Thales. Can you explain a little more of the process taken so far to integrate the company? What of the goals that the companies have independently will be merged and if it has already a name decided? Thank you.

Guillaume Faury: Thank you. I’ll start with the with the latter. There was a code name for this project at the very beginning which is Bromo and everybody is speaking about Bromo. So Bromo is not the name of the company but it starts to become more than a code name. So I don’t know there’s no name decided and we will come to it later but we just use now this code name to name this company.

We are not at the point of integration. And actually by Law we cannot do anything that is related to working together as a team or integrating as long as the closing is not done. But we are working hard together to pass the milestones required to then be able to do the closing of this merger at a point in time. And we are obviously responding and presenting our files especially on the antitrust side to the authorities and starting with the European authorities. So that’s the place where we are and as long as we are not together those companies continue to play on the market and compete on the market as they were doing before.

On FCAS and the two-fighter solution

Niklas Zabji (Frankfurter Allgemeine Zeitung): Yes thank you. Niklas Zabji with Frankfurter Allgemeine Zeitung. Guillaume on FCAS, could you please give us some more explanations on the deadlock? So on the one hand there is this dispute with Dassault on governance, on the other hand now the German Chancellor said clearly that there are also just different requirements between France and Germany. So why the deadlock and do you still see chances to overcome this dispute? And then on the two fighter solution, are the three discussed options equally thinkable? So either Airbus develops a new fighter alone or together with Sweden or joins GCAP or do you have any preference for one of those three options discussed? Thank you.

Guillaume Faury: Well I think we would be wrong to be right too early. We’re in a program that is called FCAS. We’ve spent a lot of time and energy to support this program that has a number of pillars. The so-called Next Generation Fighter is one of those pillars and it’s important to say that the other pillars are working well and making good progress namely the so-called combat cloud, the pillar on the remote carriers, the engine pillar also is making progress.

On the Next Generation fighter there is a Deadlock that is linked to expectations on the governance that differ between partners on what leadership means, what cooperation means. That’s one of the reasons of the difficulties. And also under a certain governance on the ability to reach the objective of the program for the different customers and it belongs to the customers to express themselves on that one. I will not comment. So we believe we are at a difficult juncture of the program. At Airbus we continue to believe that the program as a whole makes sense and that we should not jeopardize the progress and the relevance of the other pillars and we need to find a way forward on the NGF pillar expecting decisions from customers. And then we’ll see. We are not at the point of deciding next before this step is passed. We believe in European cooperation. We believe if there’s a way forward with two Fighters, it could be an opportunity to have other partners with us but it belongs to our customers to decide with whom they want to join forces. Would it be the case? Again we are not yet at that point.

On the A400M and European defence consolidation

Robert Wall (Aviation Week): Yeah Hi Robert Wall with Aviation Week. Just a quick follow-up on the FCAS and then A400M question. On FCAS the German Chancellor said as part of the requirements review he does want to ask the question: do they even need a sixth generation fighter? So I guess the question if there is an NGF divorce, how sure are you there’s even going to be a German program for Airbus? And then on A400M, a small housekeeping thing what was the charge for? And then more broadly how confident are you of this year getting top up orders or new customers for the program to keep production stable at eight a year?

Guillaume Faury: You take the A400M, Thomas? I will take the first one. I think the trend from manned to unmanned is very broad and very strong and we see the capabilities of autonomous systems moving forward very fast. So the question of going from manned to unmanned is on the table. The timing is very unclear. And the man-unmanned teaming is also another capability that is being developed. So I think it’s fair to raise the question. I think a lot of us believe that there will be a point in time quite far in the future where the manned capabilities will be to a large extent replaced by unmanned. And the belief at this stage is that there is still a need for a manned fighter besides growing capabilities in unmanned. I think the question is on the table for a number of forces of whether they want to directly go to the next one but then take the risk to be irrelevant for a certain point in time by a lack of modern capabilities of Manned Fighters or invest a lot of money on the Manned Fighters and then moving forward to the next capability. There’s also the understanding that there could be a way to go to a capability that would be manned and/or unmanned either at the same time or in time moving from man to unmanned. So these questions are on the table. Technology is moving very fast on programs that take a lot of time to be developed. And what the Chancellor has expressed is a question that is in industry, that is in defence and for which FCAS had found an answer: we want a sixth generation fighter. But obviously this question will remain. And we see other players having not necessarily the same conclusion. I think that’s what the Chancellor has reflected in his remark that’s my understanding at least. You should raise the question to the Chancellor directly.

Thomas Toepfer: Maybe to answer on the A400M I think the most important thing for us is that in 2025 the cash flow of the A400M was positive and so that I think is a great success relative to what we have seen in the past years. That is what counts for us most. What you’re referring to is a little bit more from the accounting side. You may know the A400M is accounted for as an estimate at completion so we have to take assumptions for the entire remaining lifetime of the aircraft. And what is reflected in the charges is twofold: one, an assessment of the production costs that we have for the A400M, but also to a certain degree certain developments which we still are pursuing in light of the request of the customer. And so those things together if you take them over numerous years and discount them today that gives you the charge but I think nothing really exceptional relative to what the program is delivering.

On transatlantic defence dynamics

Hakan Celik (Posta & CNN Turk): Thank you. Hakan Celik from Posta & CNN Turk. My question for Mr Guillaume Faury. In the context of growing transatlantic friction and visible erosion of strategic trust between the United States and Europe, how do you see this dynamic reshaping the defence and aerospace industry? On the other hand, with rising European defence budget and increasing calls for strategic autonomy, how is Airbus positioning?

Guillaume Faury: Thanks for the question. The way we look at it and we looked at it before the incremental investment of European countries on defence was that Europe was not spending enough money on defence. Data are available I will not dive into the figures but not by a small amount, by a huge amount. Not enough money on defence. Not enough money on defence from European defence manufacturers therefore buying by far too much from outside of Europe. And not buying smartly in the sense of buying too fragmented and not enough jointly for common needs.

The move that is now visible in front of us is going in the right direction. Clear increase of Defence budgets. Intent to rely much more in the future on European players for Europe to increase resilience, sovereignty of the defence system and therefore of the security of Europe. And through the efforts that are made on a number of fronts to co-operate and work jointly. We think we are at the very core of this. We can bring military capabilities to Europe at scale through the duality of our products. We develop technologies with civil and military applications that give scale and speed to our ability to come to the market. We are today the largest EU defence player by order intake and I think as well by turnover and we have capabilities that correspond very well, that are well aligned with the capability needs that have been expressed by Europe looking at the overall picture.

So our strategy is to be there. Is to be a defence player for military aircraft, for cyber, for helicopters, in space to provide the systems, the capabilities that Europe needs but beyond Europe also to serve the allies and the partners of Europe. So therefore having a growing business. And we believe roughly the speed of growth in defence will be similar to the speed of growth in non-defense activities in civil activities. Therefore having on the next five years Horizon a balance between civil and military that would probably remain around 80% for civil 20% for military.

On the A321 and next-generation successor

Sebastian Steinke (Flug Revue): Good morning. Sebastian Steinke from Flug Revue in Germany. I have a commercial aircraft question please concerning the 321. It is a huge success. Do you see a market maybe above it, just above it for maybe a bigger version or a separate program because the growth of the market in Asia seems to indicate there is a need for a slightly bigger one as well. And speaking about the 321 and looking ahead to the next Family doesn’t the 321 success create a sort of pressure for you to stay close to it because it’s now like an almost global standard. Everybody has it everybody has pilots spare parts knows the family. Can the next Family be radical enough or does it have to be close to the success model 321? Thank you.

Guillaume Faury: Thank you. So indeed we see that the demand and the core of the markets for the A320 family has moved from historically A319, A320 to A320, A321 to A321 and its upper versions namely the XLR. We have a lot on our plates to deliver on those programs and deliver in terms of production so we are focusing very much on stabilizing the design to be able to serve production at scale, at speed according to the expectation of our customers. And what I’m suggesting here is as the core of the A320 family market goes to the A321 we will see the percentage of aircraft being A320 family or A321 derivatives increase significantly. We suggested it in the forward but we don’t intend to add a next member to the family. We just move the center of the family towards more A321.

When it comes to the replacement to the successor of the aircraft we do a transition I mean every 20-25 years. In that case it will be more than 40 years. And even if we have increased very significantly the competitiveness of the aircraft, made upgrades, put new engines, new devices on the aircraft, it has to be a significant step. We’re targeting 25 to 30% fuel burn improvement compared to the A320 family and therefore it will be a very significant, it will be a very different aircraft, a very significant step. Still we want to stay in the core of what make the success of the A320 family so we will see a similar philosophies and concepts but new technologies, new performance and new characteristics. It will be very significantly different at the end.

On Pratt & Whitney engine supply

Leen Al-Saady (Bloomberg): Hi, Leen from Bloomberg. On the 870 target you’re obviously still in conversations with Pratt & Whitney. Could they potentially have bigger output? Are you hopeful that you could actually increase that number this year or is this the best it’s going to get? I mean how elastic is that target?

Guillaume Faury: We release a guidance. At the moment we release the guidance and we do it with information we have. Pratt & Whitney has resigned from the orders we had placed and they had accepted for the volumes in 2026. We have to base our guidance on what they tell us now they’re willing to commit and deliver. We’ll continue to work hard to enforce our contractual rights which we believe are not respected in that case. But we also know that Pratt is facing a number of challenges. We are not happy with the outcome but that’s what it is today. As I said earlier this morning if things change over the course of the year we will take benefit of it. If it changes obviously in the right direction which we would expect. We have to adjust the production trajectory to at least at the Beginning maintain opportunities and that creates complexity in the ramp up trajectory, in the level of Inventories we would accept moving forward. We have also to take care of the suppliers, all the other suppliers which have delivered and which continue to deliver on the ramp up trajectory so that creates complexity. And we are also very much focusing on the 2027 volumes of Pratt & Whitney engines to be back on track at least in 2027 if 2026 is not better than what we see today. So we are where we are. We release the guidance at this point of the Year with what we have that is disappointing from Pratt & Whitney and we’ll keep working.

Guillaume Steuer: Thank you Guillaume. We have a question coming up online which I will read out loud for the benefit of those in the room and on the call. It’s a question from Reuters, Tim Hepher. So you mentioned Guillaume on the analyst call that Airbus is ready to enforce its contractual rights in the dispute with Pratt & Whitney. What does this mean in practice? Have you initiated or are you planning any kind of legal action?

Guillaume Faury: We have a contract obviously with our friends from Pratt & Whitney and we see that they are not respecting their contractual obligations so we want to enforce our rights. And indeed we have initiated a process according to contractual requirements of disputes and I will not say more about it because then it becomes a commercial in confidence relationship with them but indeed I confirm we want to enforce our contractual rights.

On the A320 successor engine and SAF

Wolfgang Borgmann (Aero International): Wolfgang Borgmann, Aero International Germany. I have a question about the future A320 successor. You’ve been very public about the RISE concept and engine concept that you’re supporting but what about the Pratt & Whitney switch for example in which you are holding as well shares? So if or any other engine option like maybe Rolls-Royce I don’t know. Are there any further developments you’d like to share and also about the new wing that you’re developing it’s very quiet about that. What you presented last year as a concept idea or other technologies that you would include into the new A320 successor.

And my second question would be about SAF. It’s a more general question and wouldn’t it be about time to tell the public that SAF isn’t there? That’s just an idea. And now the USA are I think pulling out for the next three years at least and the development maybe SAF will remain just a drop on a hot stone so maybe 1% maybe 5% of the fuel needed. But I can’t see where it’s going to be made, where it’s happening, and when the general public will benefit from it.

Guillaume Faury: So two important topics for us. On the A320 successor we had the Airbus summit earlier this year. We’ve been very transparent and open on what we do. Indeed there is a number of technology bricks. Propulsion is one of them. Wings is another one. The Wings is Airbus homework and we’re working hard it’s not just an idea or a project it’s a lot of research Technologies. Now we are at the test phase of production processes to prepare for high rate production of composite wings that will be with a very large wingspan and I mean I don’t want to enter into the complexity of the technology but that’s ongoing.

It’s ongoing also on the propulsion side where there’s an important choice to be made later on whether we go for open rotor, for ducted fan, obviously in both cases with gears, with transmissions to optimise the ratio, the propulsion ratio. And that’s an important strategic choice that will impact the Architecture. And we put these Concepts in competition with each other. The open rotor technology is a more modern one is a recent one and we are working very closely in a very positive way with CFM on what they call the RISE project and we are their partner to develop this technology and to look at the integration where it would mean for the plane. We have important decisions to make later in the decade going to 2030 where we intend to launch the program. We are not at the point of decision but we are at the point of collecting all data that are required to make an educated decision that will be the best one for the program. And indeed we are working with all manufacturers that want to work on open rotor as one mainly CFM and others including CFM on what alternatives could look like and what would the best traditional geared turbofan or traditional would become traditional geared turbofan option for the Next Generation. In both cases you have pros and cons. They are not the same ones but we want to make the decision having de-risked having understood having tested as much as we can. And we are very happy to have this cooperation with CFM to go as far as we can before making a decision on the understanding of what an open rotor technology on a single aisle aircraft of Airbus would mean and how we would deliver something competitive we would certify we would have something reliable in service. And I stop here there’s a lot I would be happy to share but we have to be conscious of time.

Wolfgang Borgmann (Aero International): Yes I’m sorry. I didn’t try to escape the question. No, it’s I mean there isn’t any SAF and it’s it might be a 1% of the fuel needed, kerosene needed. And we are talking since about four years about it we are at the same level. Nothing is really improving. In Europe the energy costs are prohibitive and I can’t see where else it would be produced in huge numbers right now that would build up what the politicians want so and the airlines and manufacturer’s hopefully.

Guillaume Faury: So at Airbus we strongly believe that SAF is a necessary part of the decarbonization road map & strategy. It’s the one that is less in our hands than the others. The planes that is very much something within control. SAF is not the case. On the SAF we are trying to play the role of catalyst we’ve been engaging with a lot of people around the world: regulators, governments, airlines, fuel manufacturers, airports, you name it. The progress is slow, is too slow but it’s not zero. In Europe we have a mandate for 2% and then 6% in 2030 and we see the volumes starting to grow in Europe because of the mandates. There’s a chicken and egg situation with demand and supply and that’s really the conundrum we need to overcome. That’s why we, Airbus want to help by pushing for the book and claim system which we believe has the potential to help because today it’s not very relevant to produce SAF in a place of the world and then to use it on another place. You have to carry the SAF and you waste part of the benefit of having a decarbonised fuel because the production of SAF around the world is indeed not where it has to be to fulfill the trajectory. It’s not hopeless and we see that countries like China like India, the US with the IRA… at a point in time it’s probably not going in the right direction at the moment but still there’s production of biofuels in the US that is growing in certain areas of the US… that there is potential for making this moving forward but the tipping point of acceleration of SAF is indeed more difficult to pass than we were expecting.

There’s a price challenge. An aircraft that burns less fuel is both more competitive and more sustainable. I say economy and ecology are aligned. On SAF it’s the opposite. A fuel that is more sustainable is less competitive and therefore when you compare with your competitors you’re better off from your competitive standpoint with less SAF than the others. We need a global frame. We need a global understanding at least with the main regions of what SAF percentage should look like. Unfortunately with the fragmentation of the world at the moment we are not there and this is slowing down the SAF but we should not give up on SAF.

On Pratt & Whitney constraints and the A220

Ben Katz (Wall Street Journal), via Guillaume Steuer: Can you explain what is keeping Pratt & Whitney from meeting its requirements and is this related to the longer running metallurgy issue? And does the Pratt & Whitney constraints complicate the decision on an A220 stretch? Could Airbus consider an alternative engine provider for a new variant?

Guillaume Faury: I think I will not answer the latter part of it because we’re not at that point and the answer is mostly no it doesn’t impact what we are considering for the A220. I think the first part is the indeed important one. I’d rather have Pratt & Whitney answering that question but I give my understanding of it. They have the combined needs at the moment of serving the production for new aircraft and serving the MRO capabilities for the recall campaign linked to the metal powder and linked to the rather low durability of the engine and that puts stress on a number of bottlenecks: supply of certain parts which are too small in numbers to serve completely both needs and the MRO capability to retrofit all engines in service and reduce the number of AOGs. They’re confronted to those challenges combined at the moment and we are very frustrated that they have decided to reallocate more to the in-service because they miss global capability and to the detriment of Airbus where we think they should do more on increasing capabilities to serve both needs at the same time. We continue to to work with them to make them change the way they manage this and as I have explained earlier today we are in those negotiations. So that’s the combined needs of the ramp up on production of aircraft, on the retrofit of the metal powder issue and the need for material linked to the rather low durability of the current version of engine before the new version of the GTF Advantage comes to the market.

On the open rotor test programme

Tom Boon (Simple Flying): Hi, Tom Boon from Simple Flying. I wanted to go back to the open fan engine concept and I know before you’ve talked about strapping it to the bottom of an A380 to test it I wanted to know is this still the plan? If it is still the plan you know what does the timeline for flying it and testing it look like and finally do you see the A380 as like a longer term test bed for you or do you think once the open fan’s done that will be it?

Guillaume Faury: So yes it’s still the plan to fly the open fan, the open rotor engine. It’s still the plan to fly it on the A380 as it was indicated before and as we have explained. I don’t have the detailed planning in mind and I would be too incorrect so I will not dare giving you a date but we are preparing this so it’s starting to be something now close to us. And the future use of the A380 I’m not sure that we have yet taken a decision. It will be used for the Open Rotor testing, that’s the use we’re happy to do with it. Beyond this work I don’t know. But it’s a convenient test bed because it’s really big and you can test large engines still remaining small compared to the size of the aircraft. So in terms of safety in terms of capabilities of testing that’s really convenient. This being said it’s a very large and expensive aircraft so we’ll see moving forward what we do with with our test beds in general. But short term we do the test for the Open Rotor as planned.

On the 870 guidance as provisional

Charlotte Ryan (Aerospace America), via Guillaume Steuer: Does the failure to reach an engine agreement with Pratt mean that we should look at this year’s delivery target as more of a provisional goal than usual?

Guillaume Faury: Each and every time we give an outlook, we give a guidance that’s based on the best and most reliable information we have and with a certain risk taking and prudence at the same time. At this point of the year and under the current negotiation that we have with Pratt the current guidance reflects what they are telling us they are committed to deliver. And I think I have answered already a lot to the first part of the question. What’s holding Pratt back is some of the challenges they have to face and the fact that they don’t manage to overcome all of them at the same time. I’m not sure we can relate it to the supply chain challenges from the pandemic. It’s really linked to the need to ramp up volumes for new aircraft combined with the huge recall campaign, the retrofit plan that they have to manage and the MRO challenges that it is posing to them both on the availability of material and on the size of the MRO network that needs to be mobilized to do this. We still have too many aircraft on the ground because of missing retrofits and it’s an objective that we support but we think they can do and they should do better serving both needs. That’s why we continue to work on this. If we have better outcomes later in the year we would further adapt but it’s not the case at this very moment and we have tried hard and not obtained what we wanted so I would not take it as something that is very temporary. It’s pacing at least the beginning of the year and what we think is likely to happen.

On the A400M and European consolidation

Murdo Morrison (FlightGlobal): It’s Murdo Morrison from FlightGlobal. I wanted to come back in an earlier question that was asked about A400M and the prospects for that program. And how secure is that program in the medium term do you feel given the lack of export orders compared to the competition? And on the second more broader question on European consolidation in defence, what do you feel needs to be done in Europe in order for Europe to go forward stronger as a region able to source its own defence requirements rather than perhaps having to rely on US manufacturers?

Guillaume Faury: So first on the A400M. We are in a rather classical situation of going from initial contracts for launch customers to the export markets and the second wave I would say of orders. We see a very strong and positive feedback from operators from the air forces that are flying the A400M. A400M used in operation in certain number of places of the world has been seen as very successful and the Air Forces that operate the A400M speak very positively about it. We’re coming not far from the end of the launch contracts so we continue to have aircraft to deliver but we see that this is for the next few years. And we are indeed engaged in a number of campaigns that are promising but take time to materialize especially in this overall environment. And we see that Europe has defined air lift needs as one of the capability gaps so we hear very clearly that there will be a need for additional A400Ms. But the timing becomes a challenge. So that’s really the nexus of when those new campaigns kick in and how low do we need to go and for how long on the assembly of aircraft before we see this second wave of aircraft being manufactured. So we think the product is strong is competitive is I mean from a military standpoint very effective and we are optimistic about the mid-term and the long term but we have to navigate that transition that’s what we’re doing currently.

What would it need to make Europe stronger and what about consolidation when it comes to defence in Europe? I think we are probably the ones with the foot the front foot forward when it comes to European cooperation in defence. That’s what we are that’s what we do. And when we think there’s a larger need for consolidation cooperation for instance in space in satellites we do it and we are happy to find partners that are doing it as well. I think the short answer to your question is we need consolidation of the supply as I call it, industrial consolidation of players across borders that is very often what is difficult. And we need also consolidation of demand meaning governments, customers, military customers coming together for common needs at the same time to trigger scale. And when we work at scale in Europe we are very competitive compared to our American colleagues. But when we are very fragmented and we have a smaller demand not aligned in terms of timing across Europe it’s very difficult to launch and be successful on programs with the right scale. At Airbus we are trying to be positioned where we can make collaboration in defence in Europe happen and that’s what the current programs we’ve been discussing this morning about the A400M, the MRTT and on the helicopter side that’s what they deliver.

On Boeing orders and the United-Rolls-Royce A350 dispute

Leonard Berberi (Corriere della Sera): Hi Leonard Berberi from the Italian newspaper Corriere della Sera. I have a couple of questions. First one: 2025 after seven or eight years Boeing surpassed Airbus on aircraft orders. How much is that a consequence of your own success in these years because you took a lot of orders in these years because of also the Boeing’s missteps and how much is related to the fact that now Boeing has a new head of sales Donald J Trump? And the second question is related to the spat between United Airlines and the engine manufacturer about the A350 if you want to give a comment on that.

Guillaume Faury: I don’t know how to comment smartly on that one so I will use my joker. So when it comes to the order intake it’s quite unique that we had so many years in a row where our level of order intake was higher and in some cases much higher than the main competitor. This has led to a gap a difference in backlog that is very significant. And as we have a backlog that is so big than what it is today we have sort of 10 years plus of order intake and taking I mean book-to-bill of one in that situation means we continue to extend by one year every year. So we are satisfied with it. It is difficult to do more than this. And there is a sort of catch up effect that takes place and that we were to some extent expecting. Now it’s true as well that Boeing, the team Boeing has been well supported in a number of very large and important campaigns on a more political grounds and that’s something we have to live with. But we continue to believe that competitiveness of the product, relevance of our aircraft, satisfaction of customers, aircraft that deliver performance, competitiveness for the airlines will remain a criteria of choice and we remain very focused on having the best aircraft, the best plane. We think that’s what will protect us moving forward. We are not unhappy with the picture that we have created over the last years it puts us in a very strong position.

Guillaume Steuer: Thank you Guillaume and indeed on your other questions I think that’s a question more for United and Rolls in this case.

On A220 production rate and profitability

Olivier Bonassies (Air Finance Global): Olivier Bonassies, Air Finance Global. A question on Commercial and specifically on the A220 program. No question on the 500 don’t worry. I noted the amendment on the production rate to 13 aircraft a month by 2028. I think there was a previous forecast maybe two years ago on 14 aircraft a month by 2026. You mentioned in your remarks that the production rate would be affected by the integration of Spirit. Can you talk to us a little bit more about the performance of the A220 in terms of sales over the past two years because it’s been a bit disappointing? And what is your forecast this year? So again the production rate is it a reflection of Spirit only or also the performance of the sales on the A220 market? Thank you.

Guillaume Faury: Thank you. So indeed we have adjusted in the last two years I think the shape of the trajectory. We were initially targeting 14 now we say 13 for 2028. That’s the result of what we call balance between demand and supply. We think we can stay at rate 13, we can sustain the rate 13 moving forward based on the demand we have. We want also to position the product at the right place when it comes to the price and therefore there is a price-volume discussion that takes place to go to profitability to the program and that’s something that is important to us. So mid-term that’s more balance between demand and supply. Short-term we’re navigating the difficulties of the ramp up on Spirit and on the work packages coming from Spirit namely the Wings so there’s no big change on the short term it’s more tactical changes. And then going to the rate 13 which we believe is a good balance. On your comments or your question on demand, yes we have good campaigns ongoing you saw the news beginning of this year. We think the demand for the 220 is there. The product is making progress in terms of operational reliability in terms of satisfaction of customers and it’s going to be really where it has to be. So we are very comfortable and we trust the power of the A220 to continue to be ordered in the numbers we need to sustain the production rates.

On the Eurodrone and Turkey’s role

Guillaume Steuer: Thank you Guillaume. So we are reaching the end shortly but we’re going to take a quick one from Veronique Guillemard from Le Figaro who’s following us online. Hello Veronique. Do you expect the Eurodrone program to be abandoned?

Guillaume Faury: It’s a bit digital… No I don’t think we are there. There’s an ongoing discussion between customers on the way forward and we have the majority of customers who really want this product continue to back the demand, the program so I think it’s likely to continue.

Hakan Celik (Posta & CNN Turk): Thank you so much for this opportunity. Considering Turkey’s involvement in the Eurofighter program, by the way it will be the first non-US jet for the Turkish Air Force and the long-standing partnership with A400M with Turkey I mean Tusash… and how do you assess Turkey’s deeper integration into the European defence programs in a changing defence global environment as a NATO member and your partner? Thank you so much.

Guillaume Faury: Well first on the A400M the cooperation with Turkey is excellent. And that that’s a very positive experience on the industrial side but I believe as well on the cooperation of Turkey with European partners in the program. Turkey as a country and as a customer. Indeed the steps made on the Eurofighter are important because it means these European partners support, agree, support the fact that Turkey will become a partner for this important military capability. And I think that’s one more step of cooperation between NATO and Turkey as NATO allies. So that’s a step in a broader cooperation with Turkey coming closer to the other European countries. We have to make Eurofighter for Turkey a success like A400M was a success to keep moving forward.

Guillaume Steuer: Thank you Guillaume. And this is going to be the end of the question and answer session. Sorry Stephane we’ll discuss later. Thank you all for the great questions and thank you Thomas and Guillaume for the answer. We’ll bring our press conference to a close now. Once again a big thanks to all of you who joined us either physically or online. And a warm thank you as well to all the great communications colleagues who helped prepare and run the event today. If you have any follow-up questions of course please feel free to reach out to your usual contacts in the media relations team who will be obviously happy to support. So we wish you all a great rest of the day and we thank you again. Thank you very much.