What a carry-on baggage rule reveals about a half-trillion-euro order book.

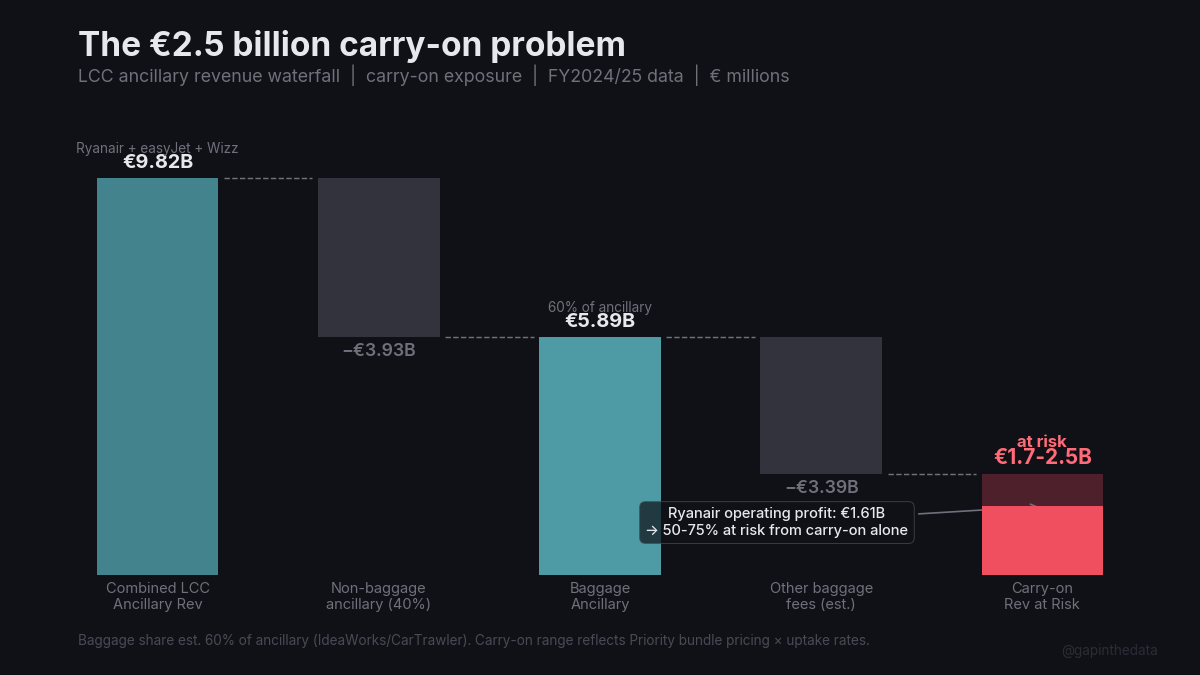

On January 21, 2026, the European Parliament voted 632–15 to mandate a free cabin bag in the base ticket price.1 An estimated €1.7–2.5 billion in annual ancillary revenue is at risk across Ryanair, easyJet, and Wizz Air.2

One week later, Airbus reported record results: a backlog of 8,754 aircraft valued at €540 billion.3 The question is how much of that backlog is exposed to a regulation that threatens the financial capacity of the carriers behind it.

I. Less than 1%

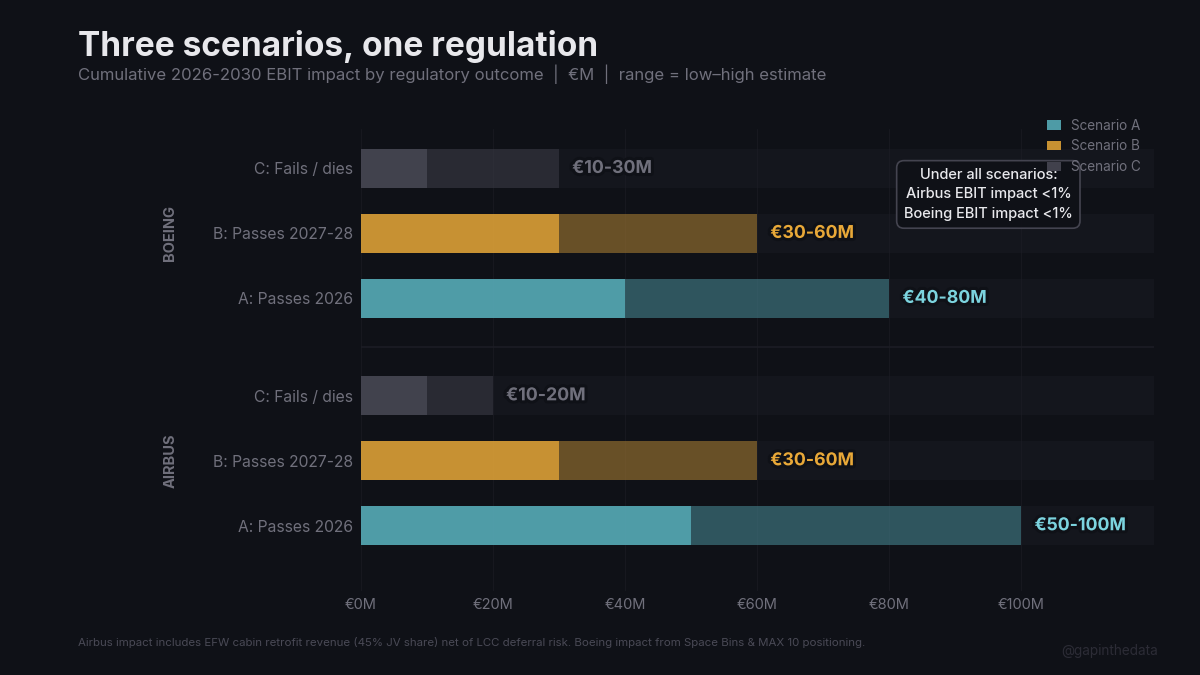

The direct effect on Airbus’s near-term group results appears limited under any scenario. Three legislative outcomes are plausible: full passage with enforcement by 2028–2029, a compromise with enforcement from 2029–2030, or failure. The compromise is likeliest.4

Under every scenario, the near-term group effect stays small relative to Airbus’s current scale. The more acute exposure sits with the airlines carrying the orders and with the timing of future deliveries.4

At less than 1% of EBIT, the regulation barely registers on Airbus’s income statement. It registers acutely on the balance sheets of the customers behind the order book. The industry has a recent case study.

II. The template

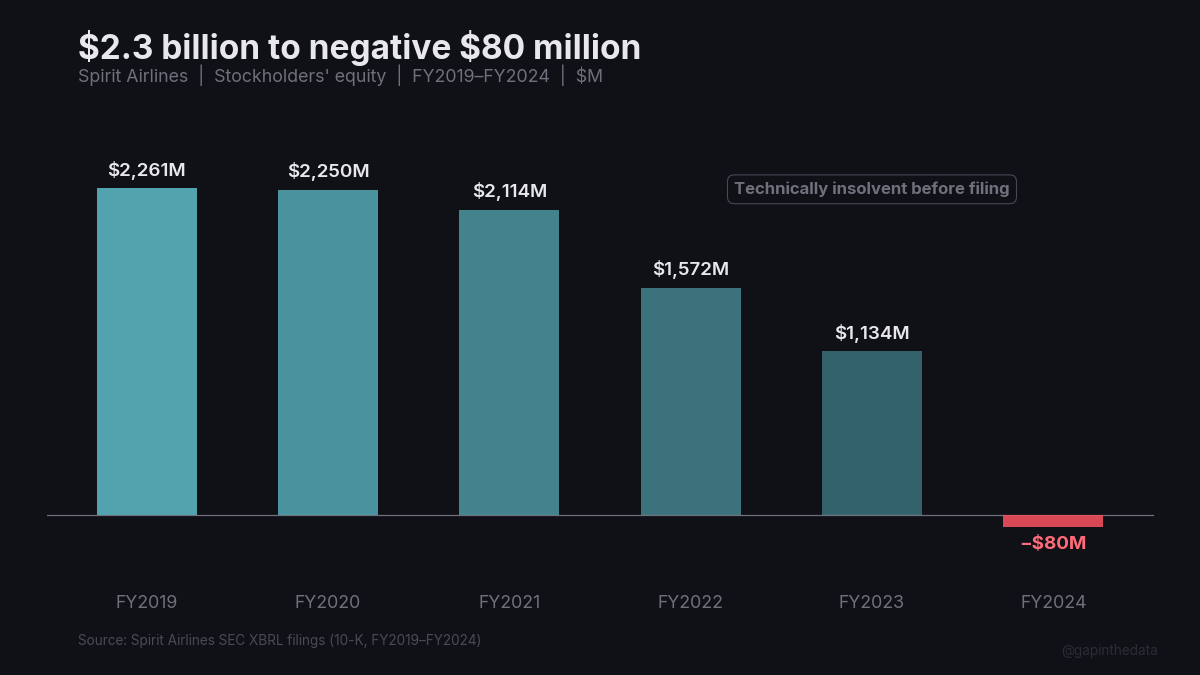

Spirit Airlines was the purest expression of the ultra-low-cost model: all-Airbus fleet, all-GTF engines, ancillary revenue approaching half of total revenue. In FY2019, Spirit reported $501 million in operating income. Five years and $3.1 billion in cumulative net losses later, equity was negative $80 million.5

The all-GTF fleet meant the grounding hit 100% of next-generation aircraft. At peak, roughly 18% of the fleet sat idle while still carrying lease and depreciation costs. The concentration that lowered unit costs in good times became an existential vulnerability in bad ones. The DOJ blocked the $3.8 billion JetBlue acquisition in January 2024, eliminating Spirit’s only strategic exit. Spirit filed for Chapter 11 in November 2024, filed again in August 2025, and downsized from 214 aircraft to 100–120.6

The profile, all-Airbus, all-GTF, high ancillary dependency, high leverage, is a template rather than an anomaly. European carriers benefit from stronger slot protections, government intervention precedent, and consolidation options that US bankruptcy law did not afford Spirit. The structural similarities matter. The specifics do not map directly.

III. One year behind

Wizz Air is exhibiting the same markers on approximately the same timeline.

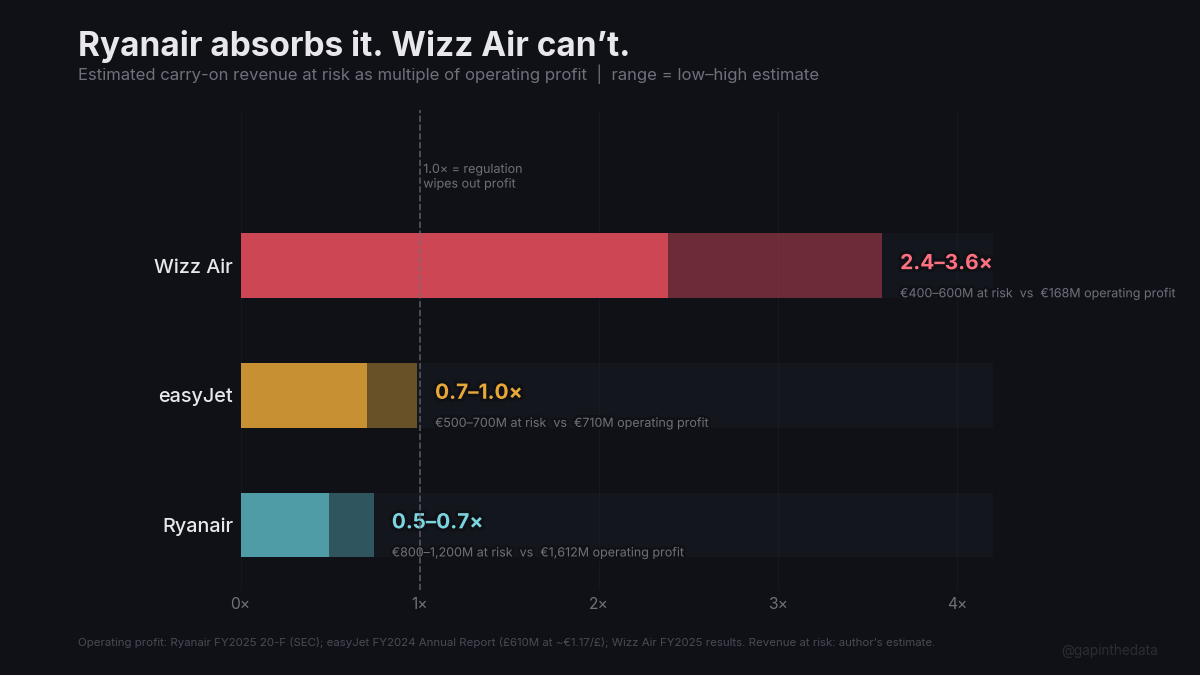

Wizz operates over 200 aircraft, with approximately one-third of its neo fleet grounded by the GTF crisis and full unparking not expected until end of 2027.7 Operating profit fell 61.7%, from €437.9 million to €167.5 million, despite revenue growing 2%.7 Moody’s downgraded Wizz to Ba2 with a negative outlook in June 2025, and Fitch downgraded it to BB in July,8 making it the only major European airline currently rated below investment grade.

The order book is already contracting. Wizz deferred 88 A321neo deliveries and cut A321XLR orders from 47 to 11, a net reduction of 124 aircraft representing approximately €6.8–8 billion in future Airbus revenue.9

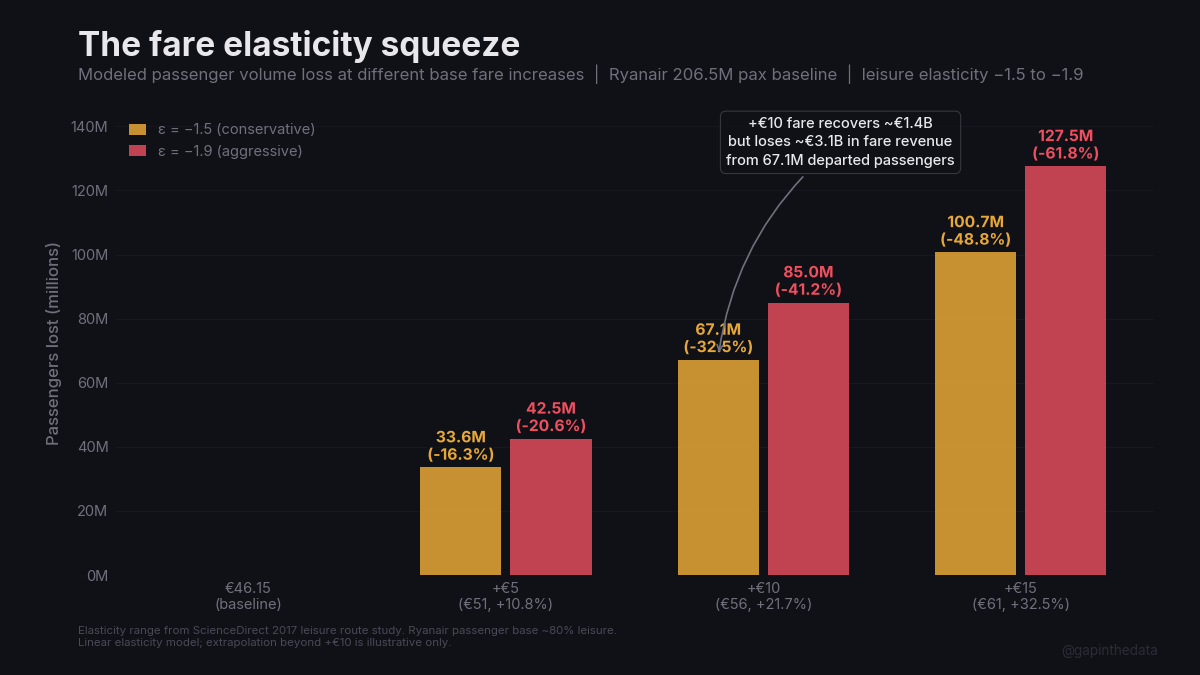

The carry-on regulation compounds all of this. Wizz derives 44.6% of total revenue from ancillary fees, the highest ratio of any major European carrier.2 An estimated €400–600 million in annual carry-on revenue is at risk, against operating profit of €167.5 million.2 7 Raising base fares to compensate destroys volume. Leisure demand is elastic, and even a modest €10 increase on a €46 base fare generates more lost revenue from departed passengers than it recovers in pricing.

easyJet demonstrates that the model is not uniformly fragile. With operating profit of approximately €710 million, lower ancillary dependency at 38.6%, investment-grade credit, and no order deferrals, easyJet is absorbing the same stressors from a considerably stronger position.10 The risk is concentrated in the weakest tail: carriers with junk credit, grounded fleets, and ancillary ratios above 40% create asymmetric downside in an order book that Airbus does not disaggregate by credit quality.

IV. The beneficiary flies Boeing

The regulation’s most obvious beneficiary is not an Airbus customer.

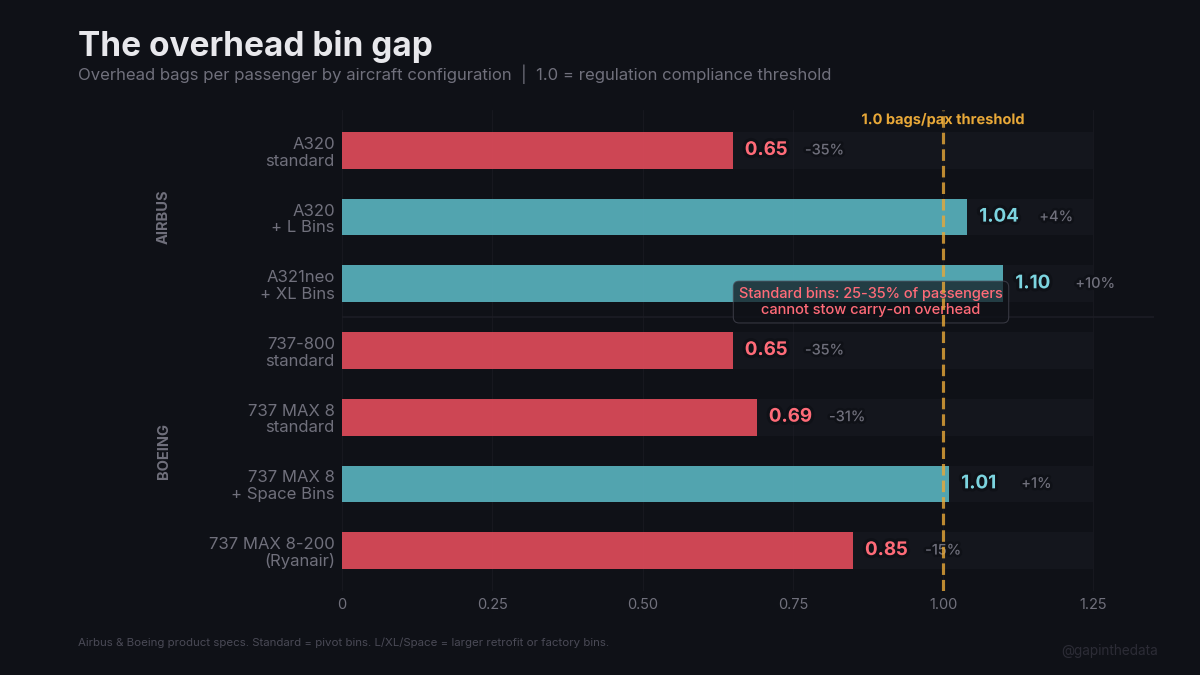

Ryanair reported €1.6 billion in net profit, €1.2 billion in net cash, and €7 billion in equity, making it one of the only major European carriers with net cash on its balance sheet.11 Its fleet is entirely Boeing: 611 aircraft today, with 300 MAX 10s on order.12 The carry-on regulation is fundamentally a bin-capacity question, and Boeing’s bins are larger across every comparable configuration.

A standard A320 achieves 0.65 bags per passenger, 35% below the compliance threshold. The MAX 8 with Space Bins exceeds 1.0.4 If the regulation passes, it imposes disproportionate retrofit costs and revenue pressure on Ryanair’s all-Airbus competitors while Ryanair’s Boeing fleet is already near-compliant.

If weakened competitors contract routes, Ryanair absorbs the capacity. Traffic that shifts from Airbus-heavy LCC operators to Ryanair does not automatically preserve Airbus demand.

V. The backlog

A backlog is a portfolio of promises made by airlines that may or may not have the financial capacity to honour them when delivery slots arrive.

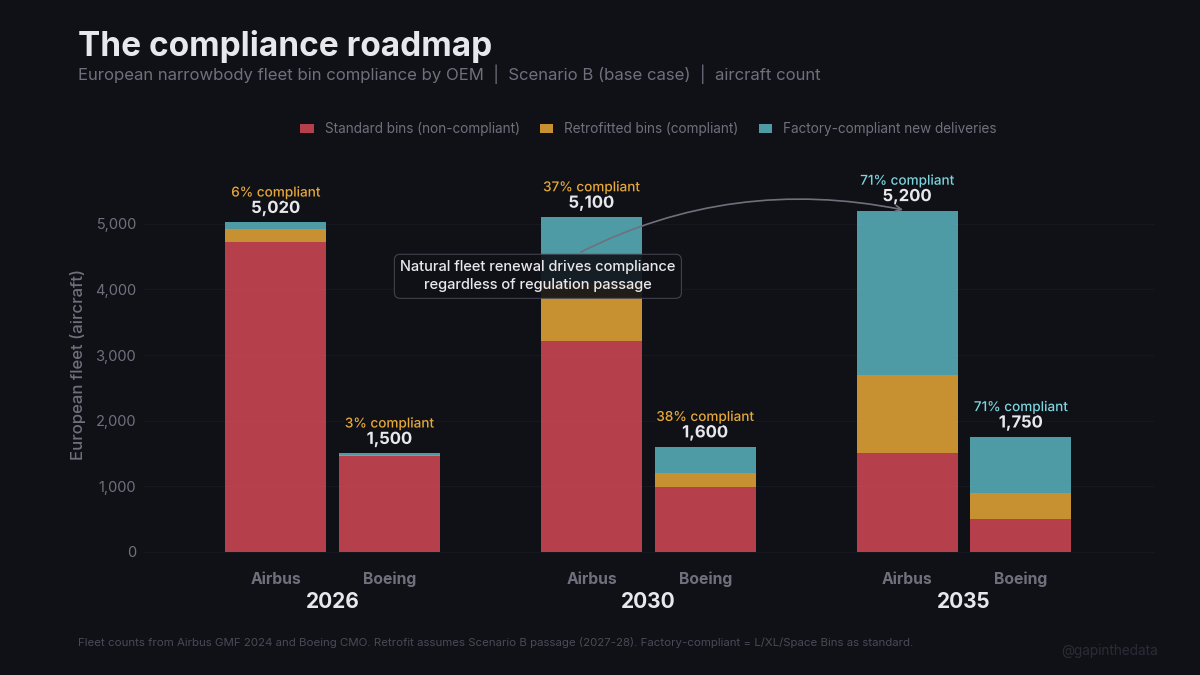

Airbus’s order book stood at 8,754 aircraft at year-end 2025.3 Net orders were 889 after 111 cancellations, more than double the 52 cancellations in FY2024.3 Cancellations are lagging indicators. Airlines defer first, renegotiate second, cancel last. Wizz’s 124-aircraft deferral does not appear in the headline figure.

Roughly 1,000–1,100 European LCC aircraft sit in the order book, approximately 12% of the backlog, concentrated entirely in the A320neo family. The same programme is already constrained by the engine duopoly and three simultaneous loss-making ramps.

Airbus holds €12.2 billion in net cash,3 but the same cash funds three concurrent loss-making production ramps, the A220, the A350 freighter, and the A321XLR, each draining working capital through at least 2028. When a distressed customer defers, Airbus has to rework the delivery slot, timing, and commercial terms. The ramps do not pause while the order book weakens.

Twelve percent of 8,754 aircraft. The credit quality behind those orders is not publicly disaggregated.

Footnotes

1 European Parliament, press release, January 21, 2026. Vote: 632–15 in favour of mandating free carry-on luggage. TRAN Committee prior vote: 36–2 (January 12, 2026). Trilogue negotiations between Parliament, Council, and Commission failed December 2, 2025. The Council remains the primary obstacle, linking carry-on rules to the delay compensation threshold under Regulation 261/2004.

2 Author’s analysis from airline financial disclosures. Ancillary revenue as percentage of total revenue: Wizz Air 44.6% (€2.27B of €5.09B), easyJet 38.6% (€2.83B of €7.33B), Ryanair 33.8% (€4.72B of €13.95B). Estimated carry-on revenue at risk: Ryanair €0.8–1.2B (206.5M passengers at €4–6/pax), easyJet €0.5–0.7B (91.1M at €5–8), Wizz Air €0.4–0.6B (62.7M at €6–10). Combined: €1.7–2.5B. Sources: Ryanair FY2025 20-F (SEC); easyJet FY2024 Annual Report; Wizz Air FY2025 results; IdeaWorks/CarTrawler ancillary revenue yearbook (2024).

3 Airbus, “Airbus Reports Full-Year (FY) 2025 Results,” February 19, 2026. Revenue €73,420M; EBIT Adjusted €7,128M (+33%); 793 deliveries; backlog 8,754 aircraft; commercial aircraft order book €539,693M. Gross orders: 1,000; net orders: 889 (cancellations: 111 vs. 52 in FY2024). A321neo: 64% of A320-family deliveries. Net cash position: €12,171M. 2026 guidance: ~870 deliveries, ~€7.5B EBIT Adjusted.

4 Author’s scenario analysis. Three-scenario framework: Scenario A (passes 2026, enforcement 2028–29); Scenario B (passes 2027–28, enforcement 2029–30); Scenario C (fails). EFW Airspace L Bins: +60% capacity, brings A320 from 0.65 to 1.04 bags/pax. Addressable European retrofit market: ~1,700 A320-family aircraft; total market $1.15–1.6B over 5–8 years. Annual Airbus EBIT contribution at 45% JV share and 15–20% services margin: €10–24M (0.1–0.3% of group EBIT). Bin capacity by config: A320 standard 0.65; A321neo + XL Bins ~1.10; 737 MAX 8-200 (Ryanair) ~0.85; 737 MAX 8 + Space Bins 1.01. Sources: Airbus Airspace cabin product documentation; EFW press releases; Boeing Space Bins specifications.

5 Spirit Airlines SEC XBRL filings (CIK 0001498710), 10-K annual reports, FY2019–FY2024. All figures in USD. Operating income/(loss): $501M (2019), −$508M (2020), −$57M (2021), −$599M (2022), −$496M (2023), −$1,105M (2024). Cumulative net losses FY2020–FY2024: $3,133M. Stockholders’ equity: $2,261M (2019) to −$80M (2024). Source: SEC CompanyFacts API.

6 Spirit Airlines collapse. GTF grounding: all-Airbus A320neo fleet powered exclusively by PW1100G engines; ~39 aircraft grounded at peak (~18% of fleet). More than 800 GTF-powered aircraft globally in storage as of end-October 2025; RTX $3B pre-tax charge (Q3 2023). DOJ blocked $3.8B JetBlue acquisition (January 2024; United States et al. v. JetBlue Airways Corp. and Spirit Airlines, Inc.). Chapter 11: filed November 2024 (SDNY), filed again August 2025; fleet downsized from ~214 to 100–120 aircraft. Sources: Reuters; Flight Global; Spirit Airlines SEC filings.

7 Wizz Air FY2025 results (fiscal year ending March 31, 2025). Fleet: approximately 203 aircraft (41 A320ceo, 41 A321ceo, ~120 A321neo); ceo fleet powered by IAE V2500, neo fleet by PW1100G GTF. 41 neo aircraft grounded at end-June 2025 (down from 46 year prior). Operating profit: €167.5M (FY2024: €437.9M; decline of 61.7%). Revenue: €5,090M (+2%). Full unparking expected by end of 2027. Sources: Aerospace Global News; Wizz Air Holdings plc results and fleet disclosures.

8 Wizz Air credit ratings, 2025. Moody’s: Ba2, negative outlook (June 2025). Fitch: BB, stable outlook (July 2025). Only major European airline rated below investment grade.

9 Wizz Air order adjustments, 2025. 88 A321neo deliveries deferred; A321XLR reduced from 47 to 11. Net reduction: 124 aircraft (~€6.8–8B in future revenue at €55–65M per aircraft). Sources: Wizz Air fleet plan; Flight Global.

10 easyJet plc FY2024 Annual Report (fiscal year ending September 30, 2024). Revenue: £8,255M. Headline profit before tax: £610M (~€710M at average exchange rate). Ancillary revenue: 38.6% of total. Investment-grade credit. Fleet: 356 aircraft; on order: 300+. No order deferrals. Source: easyJet plc Annual Report and Accounts 2024.

11 Ryanair Holdings plc FY2025 SEC XBRL filing (CIK 0001038683), 20-F annual report, fiscal year ending March 31, 2025. Revenue: €13,949M (of which ancillary: €4,719M, 33.8%). Net profit: €1,612M. Cash and cash equivalents: €3,863M. Total borrowings: €2,683M. Net cash position: €1,180M. Stockholders’ equity: €7,037M. Source: SEC CompanyFacts API.

12 Ryanair fleet and growth targets. Current fleet: 611 aircraft (all Boeing 737 variants). On order: 300 737 MAX 10 (delivery 2027–2033). FY2025 passengers: 206.5M. 737 MAX 8-200 “Gamechanger” configuration with Sky Interior achieves ~0.85 bags/pax. Source: Ryanair FY2025 Annual Report and investor presentations.